The London Stock Exchange witnessed a pre-Christmas firework display today as Gulf Marine Services (LSE: GMS) saw its share price ignite, climbing roughly 11.71% to reach intra-day highs near GBX 18.12. For retail investors and offshore energy watchers, this isn't just a seasonal drift; it’s a fundamental breakout driven by a massive contract win and a rapidly deleveraging balance sheet.

The Catalyst: Why Dec 23rd Saw an 11.71% Spike

The primary driver behind today's rally is the announcement of a major new contract award in the European market.

Source: Kalkine Group

- Asset Utilization: The contract covers two of GMS’s Large-Class vessels (E-Class), ensuring high-margin work for a staggering 985 days.

- Backlog Boost: This single win has propelled the company’s contracted backlog to a robust $540 million, providing clear revenue visibility well into 2027 and 2028.

- Market Confidence: Coming just before the holidays, this "Santa Rally" for GMS signals that the demand for self-propelled self-elevating support vessels (SESVs) remains white-hot, even as other parts of the energy sector face volatility.

The 2025 Business Model: Not Your Father’s Oil Rig

GMS has undergone a strategic metamorphosis. Its latest business model is built on high-tech versatility and cost-efficiency:

- Niche Dominance: They operate the world's youngest fleet of SESVs. Unlike traditional jack-ups that require expensive tugs, GMS vessels are self-propelled, allowing them to move between offshore sites independently, saving clients millions in logistics.

- Opex-Led Revenue: 50-70% of revenue now comes from National Oil Company (NOC) Opex budgets (maintenance/refurbishment) rather than cyclical Capex (new exploration). This makes GMS far more resilient to oil price swings.

- Dual-Sector Play: While rooted in oil and gas, the fleet is increasingly pivoting to Offshore Wind. Their Large-Class vessels are ideal for wind turbine maintenance and installation, giving GMS a green-energy growth "kicker."

Latest Financial & Operational Updates

The 2025 performance data paints a picture of a company "right-sizing" its destiny:

- H1 2025 Performance: Revenue hit $87.1 million (up 8% YoY), with Adjusted EBITDA climbing to $50.8 million.

- Deleveraging Machine: Net debt has been slashed by 22% year-on-year to approximately $172.2 million. The net leverage ratio has dropped from a dangerous 4.4x a few years ago to a healthy 1.6x.

- Guidance: Management is "highly confident" in achieving 2025 Adjusted EBITDA of $101m–$109m, with 2026 targets already eyeing the $115m mark.

- Shareholder Returns: With debt falling, GMS has signaled that dividends and share buybacks are on the horizon for 2026, a massive magnet for value investors.

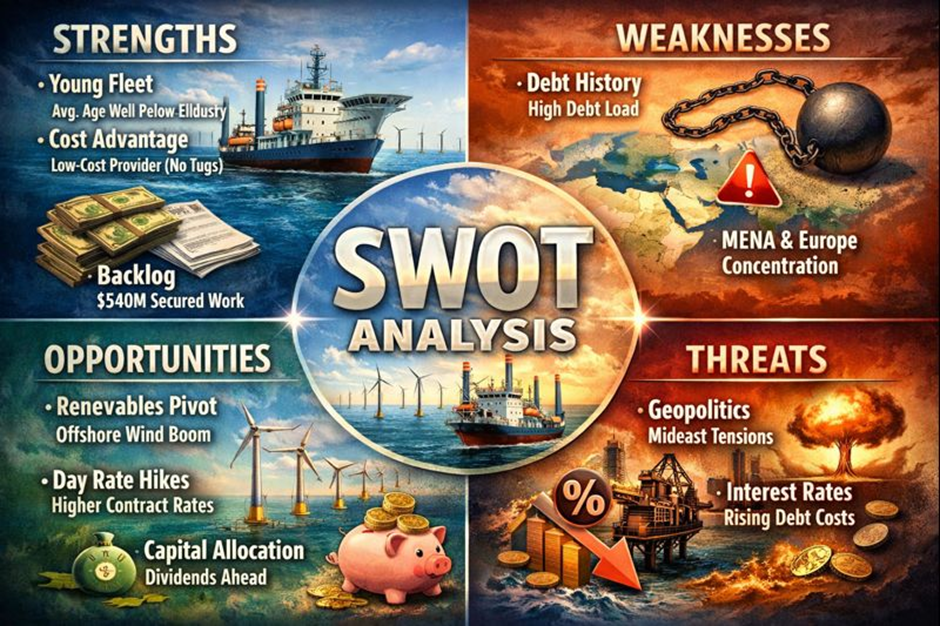

SWOT Analysis: The GMS Deep Dive

Source: Kalkine Group

Strengths

- Young Fleet: Average age is significantly below industry average, reducing maintenance downtime.

- Cost Advantage: Self-propulsion eliminates tug costs, making them the "low-cost provider" in their niche.

- Backlog: $540 million in secured work provides a massive "moat" against short-term market dips.

Weaknesses

- Debt History: While improving, the company still carries a historical debt load that requires disciplined servicing.

- Concentration: Significant exposure to the Middle East (MENA) and Europe; a downturn in either could sting.

Opportunities

- Renewables Pivot: Accelerated offshore wind build-outs in the North Sea and Asia.

- Day Rate Hikes: As global vessel supply remains tight, GMS can re-contract at significantly higher rates.

- Capital Allocation: Transitioning from "debt-repayment mode" to "dividend-paying mode."

Threats

- Geopolitics: Middle Eastern tensions can impact vessel mobilization and insurance costs.

- Interest Rates: While falling, high rates still impact the cost of remaining debt.

Key Risks to Watch

Despite the 8% jump, savvy investors should monitor:

- Contract Delays: Offshore work is subject to weather and client scheduling.

- Inflation: Rising labor and technical part costs could eat into those healthy 58-60% EBITDA margins.

- Liquidity: While the stock is surging, its current ratio remains tight (0.16), meaning the company relies heavily on its operational cash flow to meet immediate obligations.

Conclusion

Gulf Marine Services is no longer a "distressed debt" story; it is a cash-flow story. Today’s 11.71% jump reflects a market realizing that GMS has successfully filled its dance card for the next three years. With a $540M backlog, falling debt, and a foot in both the "Old Energy" and "New Energy" camps, GMS is ending 2025 as one of the FTSE’s most compelling turnaround plays.

Source: Trading View, 23 December 2025

Please wait processing your request...

Please wait processing your request...