In a strong vote of confidence from the market, Endeavour Mining (LSE: EDV), the FTSE 100’s largest West African-focused gold producer, recently saw its stock jump by approximately 3% following a series of powerhouse operational and financial updates. This surge is not merely a short-term blip, but the culmination of a dual tailwind: soaring gold prices and a strategically flawless execution of its business model.

For both seasoned financial analysts and curious retail investors, the key question remains: are these gains sustainable, and what forces are truly driving the momentum?

The Midas Touch: Two Core Drivers Behind the Surge

The recent stock performance is fuelled by two primary, interwoven factors—one external, driving revenue, and one internal, driving margins.

- The Macro-Economic Tailwind: Gold’s Safety Rally

The single greatest external driver is the historic bull cycle in gold prices. As global economic uncertainty persists and major central banks (like the Bank of England and the U.S. Federal Reserve) signal potential rate cuts, investor demand for safe-haven assets has skyrocketed. With gold prices realized by Endeavour reaching high levels (cited at over $3,200 per ounce in Q3 2025), every ounce produced translates directly into significantly higher revenue and margin expansion. This environment creates a massive "windfall" for low-cost producers like EDV.

- The Financial Powerhouse: Record-Shattering Free Cash Flow (FCF)

Internally, Endeavour's Q3 2025 results delivered a massive confidence boost. The company is expertly managing its operational output while capitalizing on the high gold price:

- Free Cash Flow Explosion: Year-to-date FCF reached an astronomical $680 million, representing a stunning over 1,400% increase compared to the prior year. This staggering cash generation is the market’s primary focus.

- Balance Sheet Fortification: The huge FCF allowed Endeavour to fully repay its revolving credit facility, reducing gross debt by $425 million and leaving its net debt to Adjusted EBITDA ratio at a remarkably low 0.21x—comfortably below its through-the-cycle target of 0.50x.

- Production Excellence: Endeavour is firmly on track to achieve the top half of its 2025 production guidance (1.11–1.26 million ounces), reinforcing its reputation for reliability.

Source: Kalkine Group

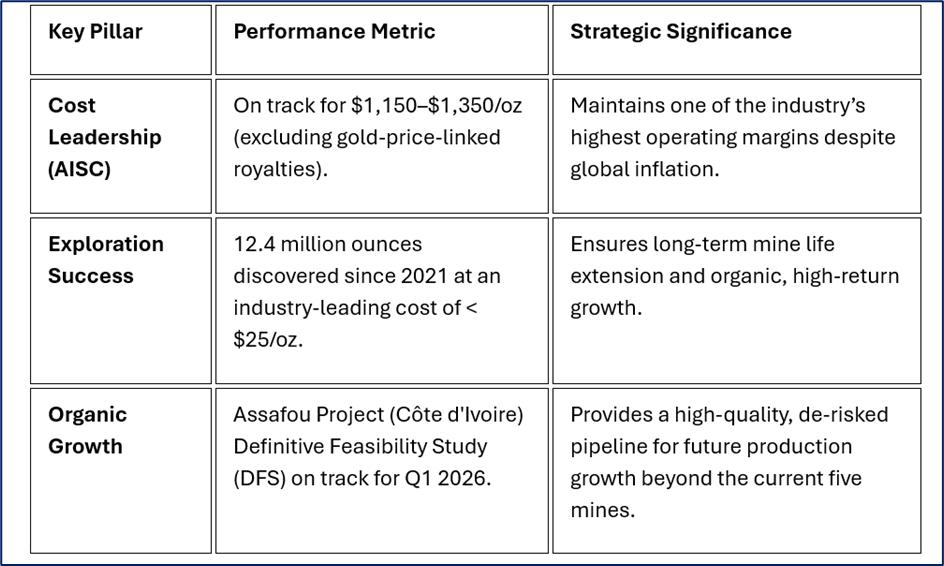

The Endeavour Model: Low-Cost Production, High-Growth Exploration

Endeavour’s competitive edge lies in its disciplined business model centered on high-quality West African assets, particularly in Senegal, Côte d'Ivoire, and Burkina Faso.

Source: Company Data

The ability to consistently replenish its reserves at such a low cost is arguably the "secret weapon" that separates Endeavour from many of its peers, securing its production outlook well into the next decade.

Investor Payback: The Shareholder Returns Machine

Crucially for investors, Endeavour has maintained a disciplined capital allocation framework designed to maximize shareholder returns. The company has already returned over $1.4 billion to shareholders since 2021—an 83% surplus above its minimum commitment.

With a record-setting $150 million dividend paid in Q4, and year-to-date returns already exceeding the full-year minimum of $225 million, Endeavour is positioned as a high-yield gold equity that rewards patience and performance. The strong balance sheet ensures that these returns are robust and sustainable, regardless of short-term gold price fluctuations.

The Geopolitical Check: Managing West African Risk

The principal risk remains the concentration of its operations entirely within West Africa, particularly in jurisdictions like Burkina Faso.

- Jurisdictional Headwinds: Political instability in some operating regions poses a risk to asset safety and continuity.

- Regulatory Royalty Pressure: Governments are increasingly seeking higher returns from their natural resources. While Endeavour benefits from stabilization clauses in older conventions (like Ity), discussions in countries like Côte d'Ivoire are ongoing, leading to potential upward pressure on future royalty rates. This is a cost headwind that investors must track carefully.

However, management has shown adeptness by proactively engaging with governments and strategically shifting focus. The growing importance of Côte d'Ivoire—a consistently highly-rated mining jurisdiction—is a strategic de-risking move.

Conclusion: The Verdict on EDV’s Run

Endeavour Mining’s ~3% surge is a clear indicator that the market is rewarding exceptional execution in a favourable environment. The combination of supercharged free cash flow, an ultra-low-cost exploration model, and a robust shareholder return program makes it a compelling choice among FTSE 100 materials stocks.

The core sustainability of the stock's run will depend on two factors: the continued strength of global gold demand and the company’s ability to successfully navigate the evolving geopolitical landscape in West Africa while bringing its Assafou project online. For now, Endeavour Mining is delivering on its promise, making it a golden opportunity for those seeking exposure to the current precious metals rally.

Source: Trading View, 16 December 2025

Please wait processing your request...

Please wait processing your request...