As the curtain closes on 2025, Hochschild Mining PLC (LSE: HOC) is providing retail investors with a year-end masterclass in momentum. Trading up approximately 6% today, the precious metals producer has hit a new 12-month high, outperforming the broader FTSE 250 and cementing its status as one of the year’s most dramatic turnaround stories.

But what is fueling this late-December rally? From skyrocketing gold prices to operational breakthroughs in Brazil, here is the deep-dive analysis of why Hochschild is the name on every trader's lips today.

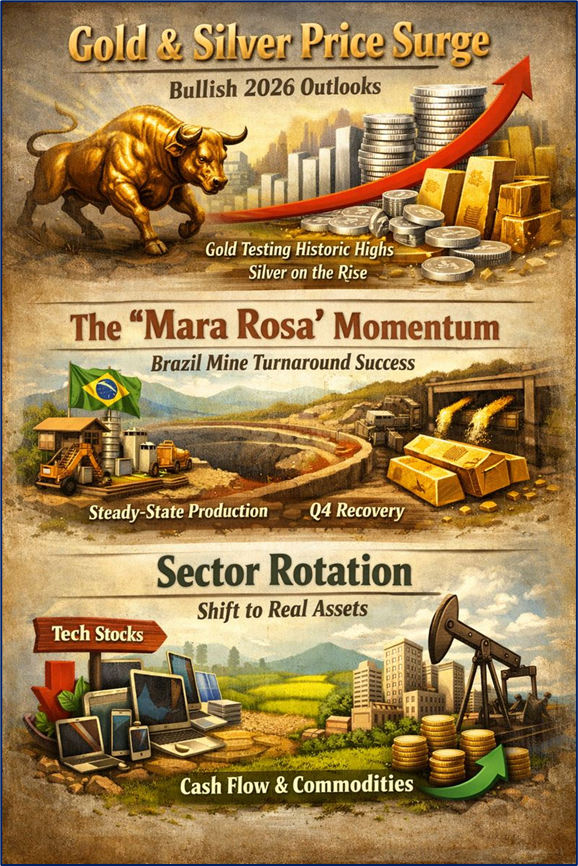

The Catalyst: Why the 6% Jump Today?

While a 6% move for a mid-cap miner is significant, it isn’t accidental. Several macro and micro factors converged on December 30:

Source: Kalkine Group

- Gold & Silver Price Surge: Gold is currently testing historic resistance levels as 2026 outlooks turn increasingly bullish. Silver has followed suit, benefiting from both its safe-haven status and rising industrial demand.

- The "Mara Rosa" Momentum: After a rocky start to the year, the market is finally pricing in the successful turnaround of the Mara Rosa mine in Brazil. Recent Q4 updates suggest the operation is finally hitting its "steady-state" stride.

- Sector Rotation: As investors rebalance portfolios for 2026, there is a clear shift away from high-valuation tech and into "real assets" with strong cash flow yields.

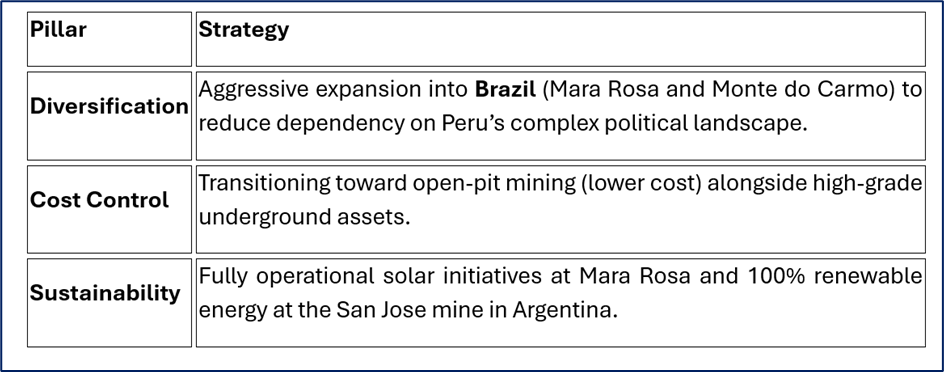

Latest Business Model: The 2025 Pivot

Hochschild has evolved from a traditional Peruvian underground miner into a diversified, multi-jurisdictional growth engine.

Source: Company Data

Financial & Operational Health Check

The Numbers (H2 2025 Snapshot)

- Revenue: Up 33% year-over-year, driven by a 28% increase in realized gold prices.

- Net Debt: Currently sitting at approximately $246 million, but with a healthy Net Debt/EBITDA ratio of 0.5x, showcasing strong deleveraging capacity.

- Dividends: The board restored the dividend in 2025, signaling a return to "financial discipline" that has been warmly received by institutional funds.

Operational Updates

The company is on track to hit its revised 2025 production guidance of 291k – 319k gold equivalent ounces. While Mara Rosa faced mechanical filter issues earlier in the year, the Q4 ramp-up has seen mining rates surge to over 70,000 tonnes per day, setting a record for the site.

SWOT Analysis: The Bull vs. Bear Case

Source: Kalkine Group

Strengths

- High Operational Leverage: Profits expand exponentially as gold prices rise due to a fixed-cost base.

- Tier-1 Assets: The Inmaculada mine remains a cash cow with a long reserve life.

- Strong ESG: Recent inclusion in the UN Global Compact boosts appeal for ESG-mandated funds.

Weaknesses

- Cost Inflation: All-In Sustaining Costs (AISC) have crept up to $1,980–$2,080/oz, leaving less margin if gold prices retreat.

- Jurisdictional Risk: Exposure to Argentina and Peru remains high, despite the Brazil expansion.

Opportunities

- Monte Do Carmo: This "low-hanging fruit" project in Brazil is expected to deliver significant growth by 2027/2028.

- Brownfield Exploration: Recent drilling at Inmaculada suggests the potential for high-grade resource extensions.

Threats

- Political Volatility: Mid-term elections in South American jurisdictions can trigger currency fluctuations and tax changes.

- Geological Risk: Operational setbacks (like the Mara Rosa filter failures) remind investors that mining is never "guaranteed."

Key Risks for 2026

While the current rally is impressive, retail investors must keep a sharp eye on two primary risks:

- Gold Price Mean Reversion: If central banks' hawkishness returns, gold could cool rapidly, hitting HOC’s share price harder than the underlying metal.

- Execution at Royropata: The next major growth leg depends on permitting and developing the Royropata zone in Peru; any delays here could stall the 2026-2027 growth narrative.

Conclusion

Hochschild Mining’s 6% jump today is the market's "vote of confidence" in a management team that has successfully navigated a crisis year. By diversifying into Brazil and maintaining its dividend, the company has transformed from a risky bet into a legitimate FTSE 250 "Value & Growth" play. As we head into 2026, the question is no longer whether Hochschild can survive—it’s how high it can fly in a record-breaking gold environment.

Please wait processing your request...

Please wait processing your request...