The first week of 2026 has kicked off with a golden bang. On January 5, 2026, Endeavour Mining (LSE: EDV) shares surged by roughly 6%, bucking the trend of New Year profit-taking and outperforming a broad market rally that saw the FTSE 100 cross the historic 10,000-point threshold.

As retail investors and institutional funds alike rebalance their portfolios for the year ahead, Endeavour has emerged as a high-conviction "Alpha" play in the precious metals sector. Here is the analytical breakdown of why the stock is moving and what the 2026 roadmap looks like.

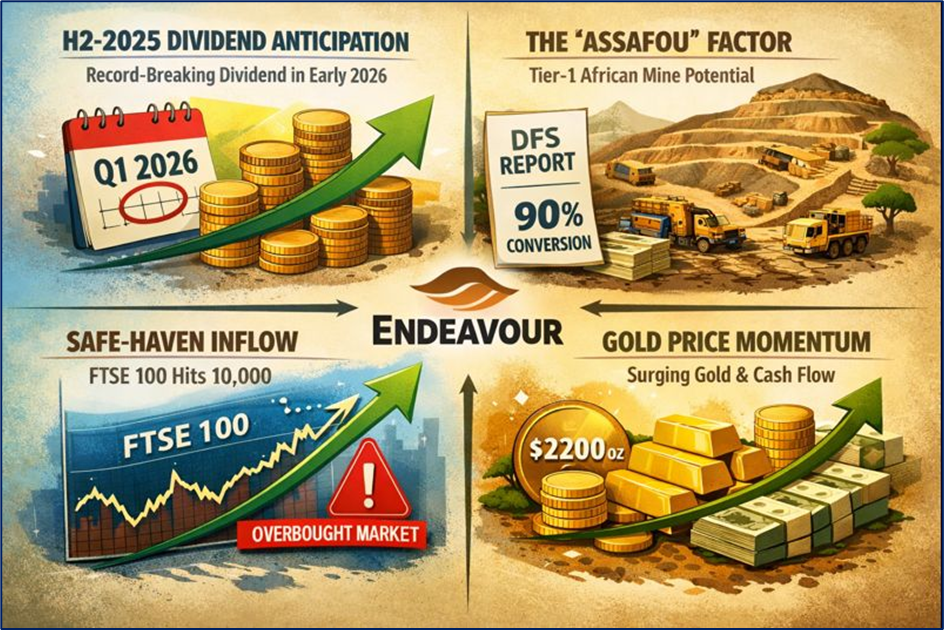

Key Drivers: Why the 6% Jump?

Source: Kalkine Group

The surge on January 5th wasn't just a "rising tide" effect. It was fueled by a confluence of specific operational and macroeconomic catalysts:

- H2-2025 Dividend Anticipation: The company confirmed in late 2025 that its H2-2025 dividend declaration—expected to be a "record breaker"—would be announced in early Q1 2026. Investors are front-running this announcement to lock in yields that are projected to be sector-leading.

- The "Assafou" Factor: The market is pricing in the upcoming Definitive Feasibility Study (DFS) for the Tanda-Iguela (Assafou) project, slated for release this quarter. Early indicators suggest a 90% resource-to-reserve conversion, potentially making it one of Africa’s most efficient tier-1 mines.

- Safe-Haven Inflow: With the FTSE 100 hitting 10,000, some analysts are warning of an "overbought" broader market. Investors are rotating capital into Endeavour as a hedge against potential equity volatility.

- Gold Price Momentum: As gold prices sustain levels near 2025 records, Endeavour’s high-margin profile means every $100/oz increase in gold contributes disproportionately to their free cash flow (FCF).

The 2026 Business Model: "The Organic Machine"

Endeavour has pivoted from being an M&A-hungry consolidator to a disciplined Organic Growth Machine. Its 2026 business model rests on four pillars:

- Self-Funded Growth: Unlike peers that dilute shareholders, Endeavour uses its $680M+ annual FCF to fund development (like Lafigué and Assafou) without heavy debt.

- Operational Cluster Model: By concentrating mines in Cote d’Ivoire, Senegal, and Burkina Faso, they share supply chains and technical expertise, keeping AISC (All-In Sustaining Costs) lower than the industry average.

- Aggressive Discovery: The "2026–2030 Strategy" aims to discover 12–15 million ounces of gold at a cost of <$40/oz, utilizing AI-driven satellite mapping and autonomous drilling.

- Aggressive Shareholder Returns: A policy of returning at least 75% of FCF above a certain threshold via buybacks and dividends.

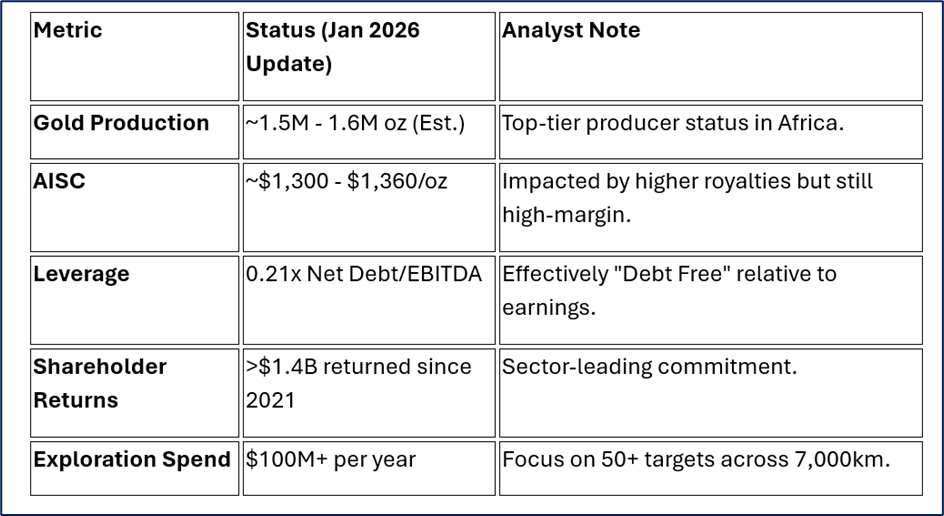

Financial & Operational Pulse (Latest Updates)

Source: Company Data

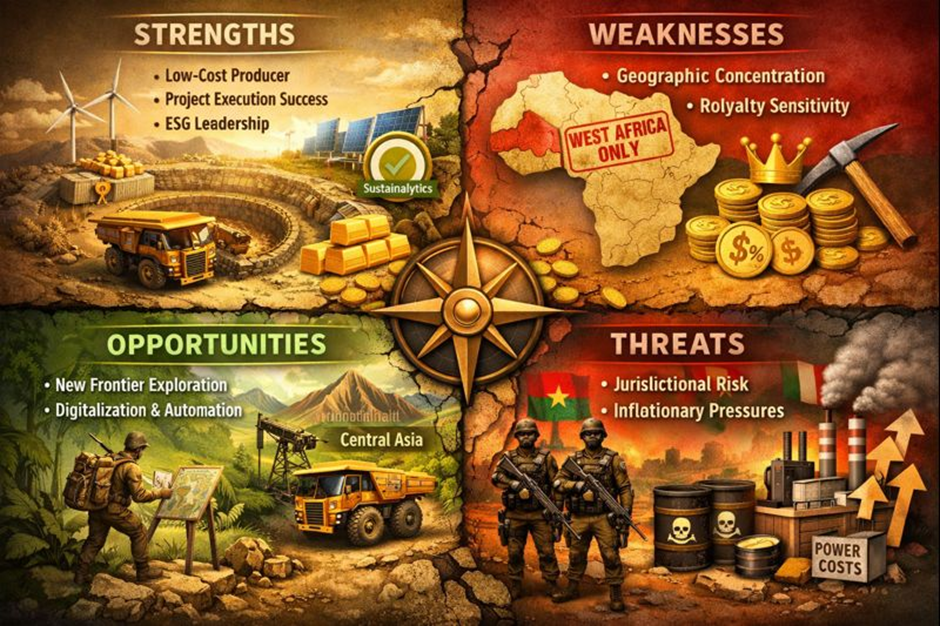

SWOT Analysis: The 2026 Reality Check

Source: Kalkine Group

Strengths

- Low-Cost Producer: AISC remains significantly below current spot gold prices.

- Project Execution: Completed five mines on time and on budget over the last decade.

- ESG Leadership: Top Sustainalytics ratings attract "green" institutional capital.

Weaknesses

- Geographic Concentration: Operations are exclusively in West Africa, creating a lack of global diversification.

- Royalty Sensitivity: Higher gold prices trigger higher government royalties, eating into some of the upside.

Opportunities

- Greenfield Frontiers: New exploration in the Guiana Shield and Central Asian Orogenic Belt could diversify the portfolio beyond Africa.

- Digitalization: Implementation of autonomous hauling could shave another 5% off operational costs.

Threats

- Jurisdictional Risk: Political shifts in Burkina Faso or Mali can lead to sudden operational pauses.

- Inflationary Pressures: Rising costs for power and cyanide (key for processing) could squeeze margins if gold prices soften.

Key Risks to Watch

Investors shouldn't ignore the "West Africa Discount." While Endeavour is a master of operating in these regions, security risks and tax regime changes remain the primary threats to the share price. Furthermore, as the company enters a high-spend exploration phase ($540M over 5 years), any failure to "hit the vein" at new sites could dampen the current valuation premium.

Conclusion

Endeavour Mining’s 6% jump on January 5 is a reflection of a company that has successfully transitioned from a builder to a harvester. With a rock-solid balance sheet, a clear 5-year exploration roadmap, and a massive dividend announcement looming, it remains the "quality pick" for those looking to play the gold sector in 2026.

Please wait processing your request...

Please wait processing your request...