Forget the S&P 500: The "Yellow Metal" Titans Dominating the FTSE Today

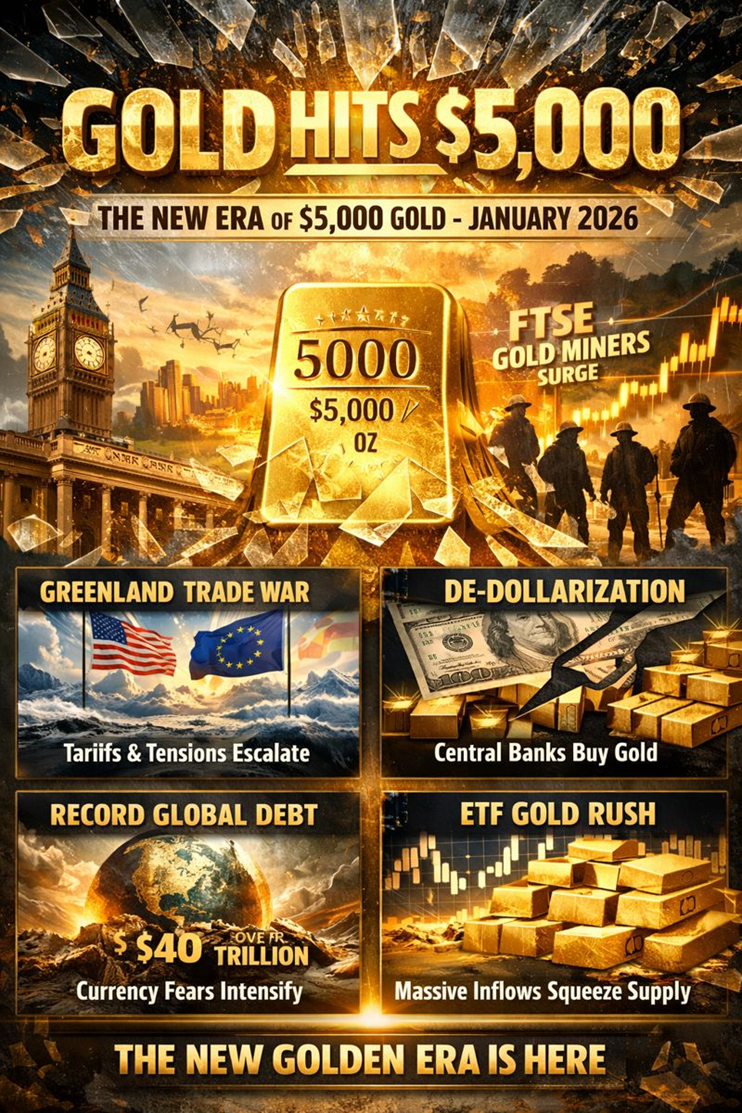

The psychological "glass ceiling" of the commodities world has shattered as gold officially breached the $5,000 per ounce mark in early 2026, marking a historic paradigm shift in global finance. This monumental surge, fueled by an explosive cocktail of aggressive trade tariffs, the "Greenland dispute" between the US and Europe, and a structural flight from the US dollar, has fundamentally rebased the valuation of safe-haven assets.

For the London Stock Exchange, this "Golden Dawn" has thrust the FTSE gold mining sector into the spotlight. As production margins widen to unprecedented levels, these five miners are operating in a reality where bullion is no longer just a hedge, but a dominant driver of corporate cash flow and capital return.

Latest Key Reasons & Drivers for the $5,000 Surge

Source: Kalkine Group

- The "Greenland Friction" and Trade Wars: A primary catalyst for the January 2026 surge has been the escalation of trade tensions. Following US threats of 25% tariffs on European allies linked to geopolitical disputes over Greenland, investors have aggressively pivoted from the dollar to gold.

- Central Bank De-Dollarization: Emerging market central banks have accelerated their diversification away from USD-denominated assets. With the US dollar’s share of global reserves hitting two-decade lows, gold has become the de facto reserve asset of choice.

- Sovereign Debt Anxiety: Record global debt levels—approaching $340 trillion—have revived fears of currency debasement. As fiscal deficits in the US and Europe remain unchecked, gold at $5,000 acts as a hedge against long-term duration risk.

- ETF Re-stocking: After years of outflows, gold-backed ETFs have seen a massive reversal. Inflows in early 2026 have tightened physical supplies, creating a "squeeze" effect that pushed prices through the $5,000 resistance.

- Endeavour Mining PLC (LSE: EDV)

- Current Business Model: West Africa’s largest gold producer, focusing on high-margin, low-AISC (All-In Sustaining Cost) assets across Senegal, Cote d'Ivoire, and Burkina Faso.

- Latest Financial/Operational Update: Reported a forward dividend yield of 4.57% as of late January 2026. The company remains on track for its 2026 exploration strategy, with new production streams expected to go live in the first half of the year (Source: Endeavour Mining Q4 2025/Jan 2026 Update).

- SWOT Analysis:

- Strengths: Massive operational leverage in West Africa; industry-leading dividend growth (30% 3-year CAGR).

- Weaknesses: Geographic concentration in politically volatile regions.

- Opportunities: High gold prices allow for accelerated debt reduction and increased share buybacks.

- Threats: Regional security risks and inflationary pressure on mining consumables.

- Fresnillo PLC (LSE: FRES)

- Current Business Model: The world’s largest silver producer with significant gold output, operating primarily in Mexico. It follows a vertically integrated model from exploration to refining.

- Latest Financial/Operational Update: For the most recent full-year cycle, adjusted revenue grew 26.9% to $3.64 billion, while EBITDA more than doubled to $1.55 billion. A one-off special dividend of 41.8 cents per share was recently highlighted as part of a record total distribution (Source: Fresnillo PLC Final Results / LSE Announcement).

- SWOT Analysis:

- Strengths: Dual exposure to silver and gold; strong liquidity with over $1.2 billion in cash.

- Weaknesses: High sensitivity to Mexican Peso volatility and local regulatory changes.

- Opportunities: $5,000 gold significantly offsets any historical silver price stagnation.

- Threats: Rising "resource nationalism" in Latin America.

- Hochschild Mining PLC (LSE: HOC)

- Current Business Model: A leading underground precious metals company focused on high-grade silver and gold deposits in the Americas (Peru, Argentina, and Brazil).

- Latest Financial/Operational Update: Paid an interim dividend of $1.0 cent per share in late 2025, with the next dividend declaration expected in April 2026. The company is benefiting from its Mara Rosa project in Brazil reaching full production capacity (Source: DividendMax / Hochschild 2026 Calendar).

- SWOT Analysis:

- Strengths: Successful diversification into Brazil; low-cost underground mining expertise.

- Weaknesses: Historical reliance on aging Peruvian mines.

- Opportunities: Exploration success at the Volcan project could significantly re-rate the stock at current prices.

- Threats: Social unrest and permitting delays in Peru.

- Pan African Resources PLC (LSE: PAF)

- Current Business Model: A mid-tier South African gold producer specializing in both high-grade underground mining and low-cost surface tailing re-treatment.

- Latest Financial/Operational Update: Declared an annual dividend of 1.64 GBp for the 2025 period, with the next payment cycle estimated for December 2026. Market cap has surged to over £2.5 billion as of January 2026 (Source: Fidelity / Stock Events 2026).

- SWOT Analysis:

- Strengths: Tailings re-treatment provides a stable, low-cost production base; high transparency in reporting.

- Weaknesses: Operational risks related to South Africa’s energy grid (Eskom).

- Opportunities: Higher gold prices make previously "marginal" underground reserves highly profitable.

- Threats: Labor disputes and rising electricity costs.

- Centamin PLC (LSE: CEY) / AngloGold Ashanti

- Current Business Model: Centamin’s flagship is the Tier 1 Sukari Gold Mine in Egypt. Note: The company is currently transitioning under the acquisition terms by AngloGold Ashanti.

- Latest Financial/Operational Update: AngloGold Ashanti reported a 109% increase in Adjusted EBITDA to $1.6 billion in their latest quarterly release. Centamin shareholders are transitioning into the new entity which paid an interim dividend of 91 US cents per share in late 2025 (Source: AngloGold Ashanti Q3-Q4 2025/2026 Release).

- SWOT Analysis:

- Strengths: Possession of Sukari, one of the world's largest producing gold mines; strengthened balance sheet under the AngloGold merger.

- Weaknesses: Complex integration process during a high-volatility market.

- Opportunities: Accelerated exploration in the Arabian-Nubian Shield.

- Threats: Geopolitical instability in the Middle East affecting logistics.

2026 Outlook and Risks

- The Bull Case: Analysts at Bank of America have already looked past the $5,000 mark, suggesting gold could reach $6,000 by Spring 2026 if the "doom loop" of global trade fragmentation continues. FTSE miners are currently generating record free cash flow, which is expected to trigger a wave of special dividends and M&A activity.

- The Bear Case: The World Gold Council warns of a "reflation return" scenario. If US fiscal policies spark a surprise growth surge, the Fed may be forced to hike rates, leading to a potential 5% to 20% correction in gold prices as investors rotate back into risk-on assets like tech stocks.

- Operational Risks: Despite $5,000 gold, miners face "margin creep" from energy costs, labor demands, and potential windfall taxes from governments looking to capture a slice of the "golden windfall."

Compelling Conclusion

The breach of $5,000 gold represents more than just a price tick; it is a signal of a fractured global order where hard assets have regained their throne. For the FTSE gold miners, this is a transformative moment. The transition from "survival mode" in the previous decade to "record profitability" in 2026 has provided these companies with the strongest balance sheets in a generation. While geopolitical volatility remains the primary driver of this rally, the operational discipline of the London-listed miners will determine which stocks capitalize on this golden era and which remain tethered to the risks of the earth they toil.

Please wait processing your request...

Please wait processing your request...