The Spark: First Gas at Galactica (USA) & Validated Production Model

The ~17.50% surge isn't just retail hype—it’s a fundamental rerating. After a volatile year, Helium One has transitioned from a "pure explorer" to a revenue-generating entity.

Source: Kalkine Group

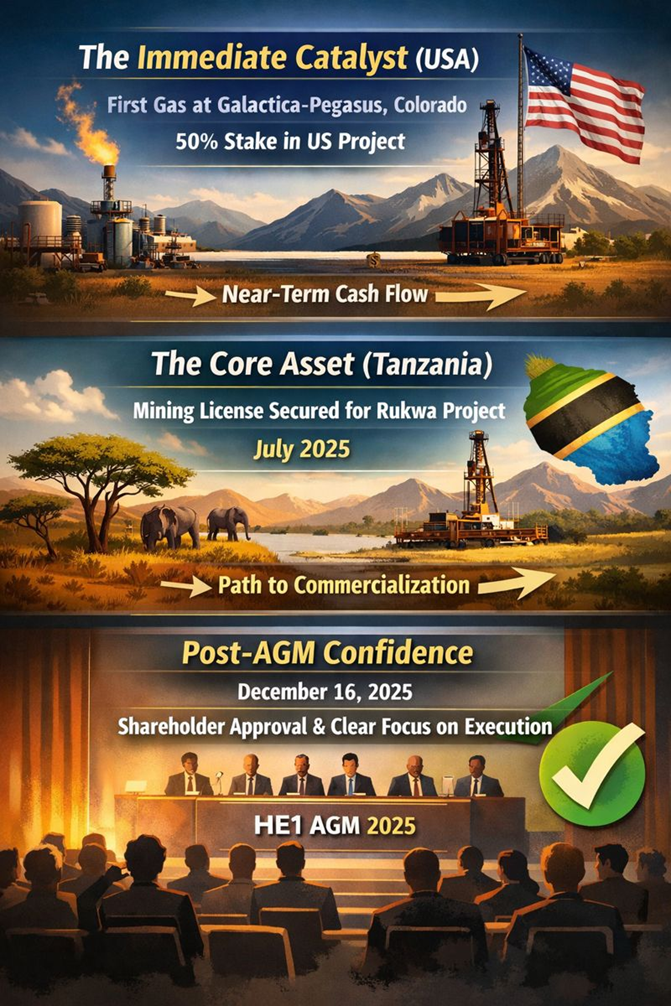

- The Immediate Catalyst (USA): The primary driver is the confirmation of First Gas at the Galactica-Pegasus project in Colorado (in which HE1 holds a 50% interest). This validates the decision to diversify into the US market, providing near-term cash flow while the massive Tanzanian asset is developed.

- The Core Asset (Tanzania): Investors are also pricing in the Mining License (ML) secured for the Rukwa Project earlier this year (July 2025). The market is waking up to the reality that the regulatory hurdles are cleared, and the path to commercialization in Tanzania is open.

- Post-AGM Confidence: Following the AGM on Dec 16, 2025, shareholder approval of key resolutions has removed governance uncertainty, allowing management to focus purely on execution.

The New Business Model: "Two-Pronged Attack"

Helium One has evolved beyond a single-asset gamble. Their 2025 strategy focuses on a Hybrid Model:

- US Cash Cow (Galactica-Pegasus): Role: Short-cycle, low-capex helium production.

- Goal: Generate immediate revenue to offset corporate overheads and fund Tanzanian operations, reducing the need for dilutive equity raises.

- Status: PRODUCING. (First Gas confirmed Dec 2025).

- Tanzanian Giant (Rukwa - Itumbula West-1):

- Role: The "Company Maker." High-grade helium (up to 5.5-7.9%) with significant scale.

- Goal: Large-scale commercial export of liquid helium.

- Status: DEVELOPMENT. Mining License granted; moving toward plant construction and full-field development.

SWOT Analysis

Source: Kalkine Group

Financial & Operational Health Check (Dec 2025 Update)

- Cash Position: Improved following the mid-2025 equity raise (~£11m) and the move toward revenue generation in the US.

- Burn Rate: The company has been managing a tight ship, but the transition to development (building plants) is expensive. The US revenue is critical here to plug the gap.

- Operations: * Rukwa: Focus is now on the Feasibility Study and FEED (Front End Engineering Design) for the processing plant.

- Galactica: Ramping up well count to maximize daily production volume.

The Risks: What Could Go Wrong?

- The "Sustained Flow" Trap: Achieving a high flow rate for a week (EWT) is different from 10 years of production. Reservoir pressure depletion is a real geological risk.

- Infrastructure Delay: Getting the necessary processing units (LHe plants) to rural Tanzania can face massive lead-time delays (often 12-18 months).

- Dilution Loop: If the US revenue doesn't ramp up fast enough, they may need one more large fundraise to build the Tanzanian plant, hurting the share price temporarily.

Conclusion: The Verdict

Helium One is no longer just a "punt." The 16% rise reflects the market acknowledging two massive de-risking events: US Production and the Tanzanian Mining License.

For the retail investor, the narrative has shifted from "Will they find helium?" to "How fast can they sell it?". The massive grades in Tanzania offer 10x potential, while the US assets put a "floor" under the valuation. The dream is alive, and for the first time, it's generating cash.

Source: Trading View, 23 December 2025

Please wait processing your request...

Please wait processing your request...