Hollywood Bowl Group PLC (LSE: BOWL) saw its shares jump by around 5% following the announcement of its full-year results for FY2025 (year ended September 30, 2025), which highlighted a fourth consecutive year of record revenue and profit. The market reacted positively to the company's strong performance, particularly its resilience in a challenging economic climate and its aggressive growth strategy.

Key Reasons & Drivers for the 5% Surge

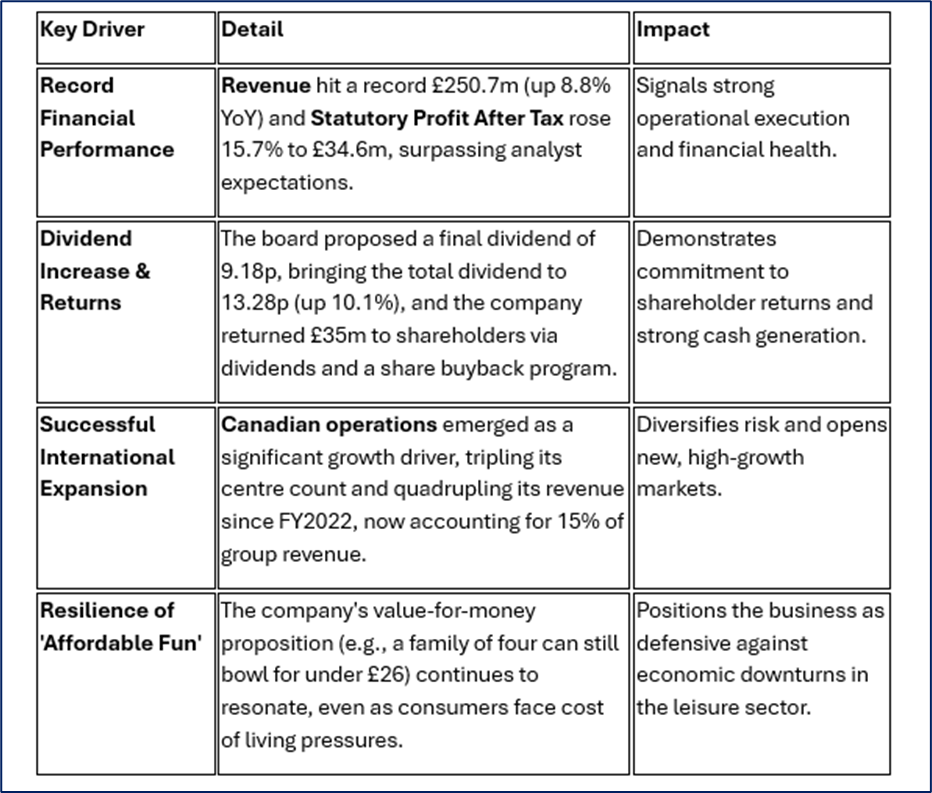

The stock price increase is primarily driven by the exceptional financial results and confidence in the company's strategic execution:

Source: Company Data

Latest Business Updates (FY2025)

- Estate Expansion: A record seven new centres were opened (five in the UK, two in Canada), alongside 12 refurbishments across the group. This accelerates progress toward the target of 130 centres by 2035.

- Spend Per Game Uplift: Despite a decline in game volumes (likely due to challenging weather/economic headwinds in the UK), spend per game surged 9.2% in the UK and 14.8% in Canada. This reflects successful pricing and the positive impact of ancillary sales (food, drink, amusements).

- Operational Efficiency: The rollout of the Compass bespoke booking system and the use of Pins on Strings technology (reducing lane downtime) have improved operational costs and customer experience.

- Cost Management: Energy costs in the UK are hedged through FY2027, mitigating a major inflationary risk.

Source: Kalkine Group

Business Model: The Competitive Socialising Powerhouse

Hollywood Bowl Group's business model is a high-margin, cash-generative model centered on providing a complete, affordable leisure experience.

- Core Offering: High-quality, modern Ten-Pin Bowling (under Hollywood Bowl/Splitsville brands).

- Ancillary Revenue (High-Margin): Significant income comes from Amusements, Food, and Beverage (F&B) sales, which increases customer 'dwell time' and average spend.

- Real Estate Strategy: Centers are predominantly located in prime out-of-town, multi-use leisure/retail parks with good visibility and foot traffic (often alongside cinemas/casual dining).

- Value Proposition: Focusing on affordable, multi-generational fun (families, friends, corporate events) makes it resilient during economic squeeze.

Principal Risks

- Economic Environment: While currently resilient, a severe and prolonged cost of living crisis could eventually lead to consumers cutting back even on affordable leisure.

- Operational Risks: Dependence on core IT systems (e.g., booking platform, digital engagement) and the efficient management of a growing, diverse estate (UK and Canada).

- Inflationary Pressures: Increased costs for staffing (e.g., minimum wage hikes) and food/beverage supply, which must be balanced against maintaining the 'affordable' price point.

- Competition: The growing trend of "competitive socialising" means new competitors entering the market (mini-golf, darts, axe-throwing venues).

Conclusion: A Defensive Growth Stock

Hollywood Bowl Group has demonstrated its ability to thrive in a tough environment by executing its strategic playbook: investing in its estate, expanding aggressively in the UK and Canada, and successfully driving high-margin ancillary spend through a superior, value-focused customer experience. The 5% stock surge is a clear vote of confidence from the market that the company's differentiated business model is delivering sustainable, profitable growth, positioning it as a leading "affordable leisure" stock.

Source: Trading View, 16 December 2025, 9:00 AM GMT

Please wait processing your request...

Please wait processing your request...