If you are tracking the FTSE 250 today, you likely spotted IntegraFin Holdings (IHP) - making a decisive move, jumping approximately 5-6% in early trading. For retail investors who might overlook the "plumbing" of the financial world, IntegraFin is the parent company of Transact, one of the UK’s premier investment platforms for financial advisers. While it’s not as consumer-facing as a Robinhood or Hargreaves Lansdown, it is a B2B powerhouse.

Today's surge isn't speculation; it is driven by hard data released in their Full Year Results for the year ended 30 September 2025.

1. Key Drivers: Why the Stock is Popping Today

The primary catalyst is the release of stellar FY2025 Annual Results this morning (December 17, 2025). The company beat expectations on critical growth metrics that matter most to platform businesses: Net Inflows and Profitability.

The "Wow" Metrics (FY25 vs FY24)

- Net Inflows Skyrocketed: Net inflows hit £4.4 billion, a massive 76% increase year-on-year. In a year where many asset managers struggled to attract new cash, Transact acted as a magnet for adviser assets.

- Funds Under Direction (FUD): Total assets on the platform grew 16% to £74.2 billion. This is the critical number because IntegraFin’s revenue is a percentage of this pot.

- Profit Growth: Underlying Profit Before Tax (PBT) rose 7% to £75.4 million.

- Dividend Boost: Management signaled confidence by raising the total dividend by 9% to GBX 11.3per share.

The Analyst Take: The market loves "operating leverage." IntegraFin showed it can grow assets (inflows) significantly faster than its costs, which drives pure profit margin expansion. The 76% jump in inflows suggests that while competitors were distracted, Transact was winning market share from UK financial advisers.

2. The Business Model: How IntegraFin Prints Money

To understand the sustainability of this rally, you must understand the "Transact" model. It is a classic Platform-as-a-Service (PaaS) for wealth management.

The "Toll Road" Model

IntegraFin does not pick stocks or manage funds. It provides the infrastructure (software and administration) that lets financial advisers hold their clients' ISAs, pensions, and investment portfolios in one place.

- Revenue Source: They charge an annual fee based on the percentage of assets held on the platform (Funds Under Direction).

- Example: If markets go up 10%, IntegraFin’s revenue goes up ~10% without them lifting a finger (beta exposure).

- Example: If advisers bring new clients to the platform, revenue goes up (alpha growth).

- Moat: "Stickiness." Once a financial adviser moves their clients' assets to Transact, it is incredibly painful and time-consuming to leave. Retention rates are typically over 95%, creating a recurring, annuity-like revenue stream.

3. Latest Business Updates (Dec 2025)

Beyond the raw numbers, today's report highlighted two strategic shifts that are fueling the bullish sentiment:

- Cost Efficiency Program: The company completed a Group-wide cost review. They have identified "enhanced business efficiency and productivity opportunities." In plain English: they are cutting fat to ensure that future revenue growth drops straight to the bottom line.

- Digitalization Push: Continued investment in the Time4Advice software (their adviser back-office system) is starting to pay off, creating an ecosystem where advisers are "locked in" not just for custody, but for their own practice management.

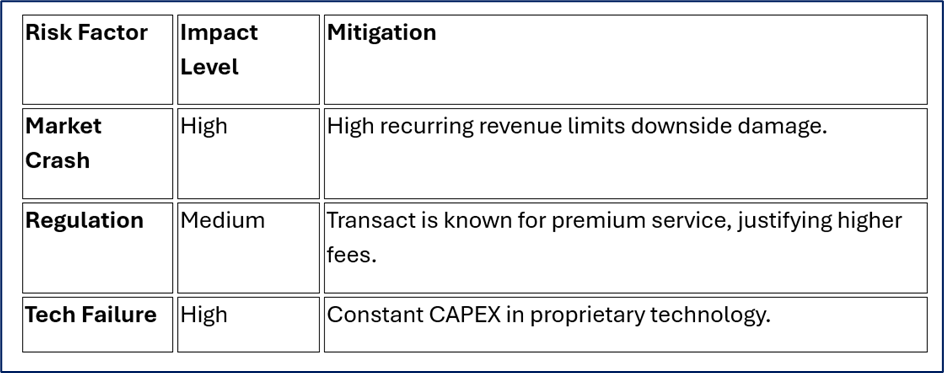

4. Risks: What Could Kill the Momentum?

No stock is without risk, and IntegraFin trades at a premium valuation because of its quality. Here is the "Bear Case" you must consider:

- Market Correlation (Beta Risk): Since revenue is tied to the value of assets on the platform, a stock market crash directly hurts IntegraFin’s top line. If the FTSE or S&P 500 tanks 20%, IntegraFin's revenue base shrinks by 20% overnight.

- Fee Pressure: The UK regulator (FCA) is obsessed with "Consumer Duty" and lowering costs for retail investors. There is constant pressure on platforms to lower their fees. If IntegraFin has to cut prices to compete with cheaper rivals (like AJ Bell or Vanguard), margins will compress.

- Adviser Consolidation: As small financial advice firms get bought up by giant consolidators, those giants might force a switch to their own proprietary platforms, cutting Transact out of the loop.

Source: Kalkine Group

5. Conclusion:

IntegraFin is a high-quality "picks and shovels" play on the UK wealth market. Today's 5% jump is a rational re-pricing based on them proving they can accelerate growth (that massive 76% inflow jump) even in a mature market. If you believe the UK stock market will recover and financial advice will remain a growing industry, IHP is one of the safest ways to play that trend. If you think a global recession is imminent or that AI will replace financial advisers, IHP is vulnerable.

Bottom Line: The "Integrain" (IntegraFin) surge is real, supported by cash flow and double-digit asset growth. It remains a premium stock for a reason.

Source: Trading View, 17 December 2025, 10:30 AM GMT

Please wait processing your request...

Please wait processing your request...