FTSE 250 Growth Pulse: IP Group and Metro Bank Lead Mid-Cap Resurgence

The London market is witnessing a tactical shift as investors pivot toward undervalued specialists, with IP Group (IPO) and Metro Bank (MTRO) emerging as standout performers on January 27, 2026. While the broader FTSE 250 navigates global macroeconomic shifts, these two entities are carving out gains through aggressive portfolio realisations and a successful pivot toward high-margin specialist lending.

IP Group is currently benefiting from a flurry of monetization events in its deep-tech and life sciences holdings, while Metro Bank continues its "turnaround story" of the year, bolstered by a lean cost structure and a robust capital buffer that has silenced previous liquidity concerns.

IP Group PLC (IPO): The Science of Monetization

Source: Kalkine Group

Latest Drivers of the Surge

- The primary catalyst for today's upward movement is the reiteration of the company’s ambitious exit target, aiming for over £250 million in realisations by the end of FY27 (London Stock Exchange, Jan 2026).

- Recent positive momentum in the obesity drug sector has cast a halo effect on IP Group’s holdings, particularly following updates regarding Metsera, where potential income streams are becoming more visible to the market (AJ Bell).

- Continued execution of the £75 million share buyback programme has provided a structural floor for the share price, signaling management's confidence in the underlying Net Asset Value (NAV).

Business Model & Operational Update

- Model: IP Group acts as a bridge between world-class university research and the public markets. It provides "patient capital" to spin-outs in Life Sciences, Deeptech, and Cleantech, typically taking significant minority stakes.

- Financials: In the latest company release, the group highlighted a strengthened liquidity position following the sale of Featurespace to Visa, which marked one of its largest cash realisations to date (IP Group Annual Report).

- Dividends: The group maintains a flexible capital return policy, prioritizing share buybacks when the stock trades at a significant discount to NAV, though it has previously returned capital via special dividends following major exits.

SWOT Analysis

- Strengths: Unrivaled access to UK and US university IP; diversified portfolio across non-correlated sectors; permanent capital structure.

- Weaknesses: Vulnerability to "fair value" write-downs in volatile markets; high dependence on the IPO window for portfolio exits.

- Opportunities: Growing global demand for AI and Cleantech solutions (estimated $2.5 trillion market by 2025); increased M&A interest from Big Pharma for biotech assets.

- Threats: Higher-for-longer interest rates devaluing long-duration tech assets; intense competition from private equity for early-stage deals.

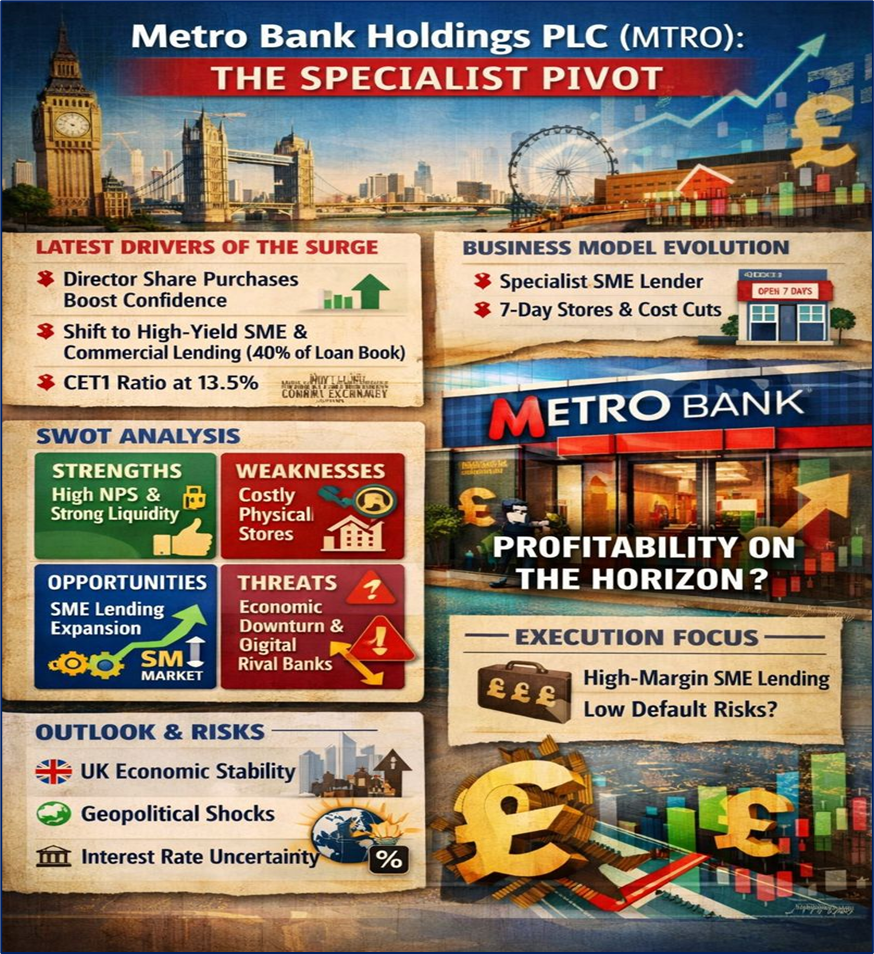

Metro Bank Holdings PLC (MTRO): The Specialist Pivot

Source: Kalkine Group

Latest Drivers of the Surge

- Metro Bank is trending higher following a series of Director/PDMR shareholdings updates in January 2026, which often signals internal confidence in the bank’s recovery trajectory (London Stock Exchange).

- The market is reacting positively to the bank’s successful rotation away from low-margin residential mortgages toward high-yield specialist SME and commercial lending, which now constitutes roughly 40% of the loan book (DCFmodeling Analysis).

- A "risk-on" sentiment for UK domestic banks is being supported by Metro’s stabilised CET1 ratio of 13.5%, significantly above regulatory requirements.

Business Model & Operational Update

- Model: Originally a "disruptor" high-street bank, Metro has transitioned into a specialist lender. It maintains a "stores" (not branches) model focused on 7-day-a-week service while aggressively cutting back-office costs.

- Financials: Operational updates indicate a sharp reduction in the cost-of-risk to 0.06%, down from 0.26% in the previous year, as the bank sheds underperforming assets (Metro Bank FY Trading Update).

- Dividends: While the bank has focused on capital preservation and meeting MREL requirements through 2025, the recent return to profitability has led to analyst speculation regarding a timeline for future capital returns (Simply Wall St).

SWOT Analysis

- Strengths: Industry-leading Net Promoter Score (NPS > 80); unique physical service proposition; robust liquidity coverage ratio of 180%.

- Weaknesses: High operational costs associated with physical stores; historically volatile reputation during the 2023-2024 recapitalization phase.

- Opportunities: Expansion into the specialist SME lending market where traditional "Big Four" banks are retreating; digital upgrades to improve customer "stickiness."

- Threats: Potential for increased arrears in the SME sector if the UK economy cools; intense competition from digital-only challenger banks.

Outlook & Risks

The outlook for both IP Group and Metro Bank remains tied to the stability of the UK’s macroeconomic environment. For IP Group, the key will be the successful listing or sale of late-stage assets like Hinge Health. If the IPO market remains open, the discount between its share price and NAV could narrow. For Metro Bank, the focus is on execution; management must prove that the shift to commercial lending can maintain high margins without a spike in defaults.

Risks include geopolitical shocks that could freeze capital markets (impacting IPO's exits) and sudden shifts in the Bank of England's interest rate path that could compress Metro’s net interest margins.

Conclusion

The ascent of IP Group and Metro Bank on January 27, 2026, reflects a broader market appetite for "self-help" stories. IP Group is proving its ability to extract cash from complex science, while Metro Bank is successfully rebranding itself from a struggling retail player to a disciplined specialist lender. Both stocks represent the high-alpha potential within the FTSE 250 for those monitoring corporate turnarounds and asset monetization cycles.

Please wait processing your request...

Please wait processing your request...