The London market may be winding down for the year, but International Personal Finance (LSE: IPF) just set off some late-year fireworks. On December 29, 2025, the FTSE 250 constituent saw its shares jump approximately 6%, bucking the broader trend of quiet holiday trading.

But this wasn't just a "Santa Rally" fluke. The surge marks the culmination of a dramatic takeover battle that has kept retail and institutional investors on the edge of their seats for months.

The Catalyst: A "Recommended" Takeover Breakthrough

The primary driver behind today's ~6% spike is the official announcement of a Recommended Cash Acquisition.

After months of extensions and "possible offer" teases, the Board of IPF has finally backed a definitive deal with IPF Parent Holdings Limited (backed by BasePoint Capital).

The Key Numbers:

- Offer Price: 235p per share in cash.

- Bonus Sweetener: Shareholders retain a final dividend of up to 9p per share.

- Total Value: Approximately £543 million.

- The Premium: This represents a massive 45.3% premium over the volume-weighted average price before the offer period began in July.

Investors are flocking to the stock today to capture the remaining gap between the previous trading price and the "total exit value" of 244p (offer + dividend).

Financial & Operational Health Check

While the takeover news is the headline, the deal was only possible because of IPF's robust 2025 performance. Their "Next Gen" strategy has yielded impressive results:

Source: Kalkine Group

- Growth: Customer lending momentum is up 12% year-on-year.

- Asset Quality: The annualised impairment rate has dropped to 9%, significantly beating their target range of 14–16%.

- Digital Pivot: Explosive growth in digital credit lines in Mexico and Australia has diversified their traditional home-collected credit model.

- De-risking: The company successfully redeemed its remaining €66.7m Eurobonds in April 2025, leaving a cleaner, more attractive balance sheet for the acquirers.

The Business Model: Evolution to "Next Gen"

IPF has moved far beyond its origins as a traditional door-to-door lender. The latest business model focuses on Financial Inclusion through three distinct pillars:

- European Home Credit: High-margin, relationship-based lending in Poland, Hungary, and Romania.

- IPF Digital: A fast-growing fintech arm offering revolving credit lines and installment loans via mobile apps.

- Mexico Home Credit: A massive market opportunity where banking penetration remains low.

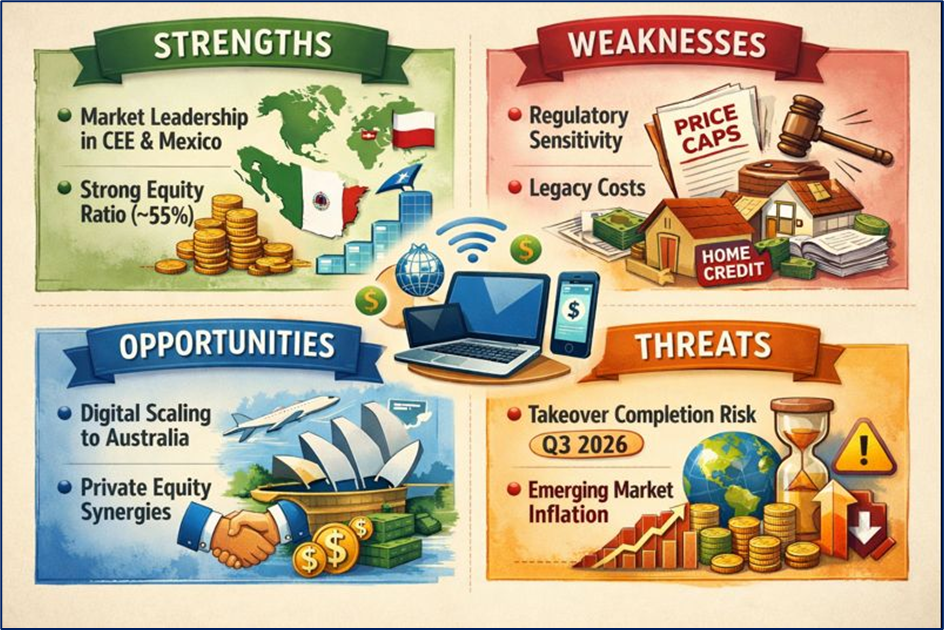

SWOT Analysis (Late 2025 Context)

Source: Kalkine Group

Key Risks to Watch

Even with a recommended offer on the table, the "deal isn't done until it's done."

- Timeline: The acquisition is not expected to close until Q3 2026, meaning shareholders' capital could be tied up for months.

- Regulatory Approval: As a financial services provider, the deal requires "change in control" approvals from multiple international regulators.

- Market Volatility: While the cash offer provides a floor, any "interloper" bid (though unlikely) or a deal collapse could cause sharp volatility.

Conclusion

The 6% jump today is a clear signal that the market views the 235p + 9p offer as "fair value" for a business that has successfully modernized its operations. For IPF, going private under BasePoint Capital represents a chance to escape the "FTSE 250 discount" and fund its next stage of digital growth away from the glare of quarterly public reporting.

Please wait processing your request...

Please wait processing your request...