As of January 21, 2026, Barclays PLC (LSE: BARC) continues to demonstrate the resilience and strategic evolution that has made it a focal point of the FTSE 100’s recent performance. Following a 0.20% surge on January 20, the banking giant is navigating a complex macroeconomic landscape characterized by shifting interest rate expectations and a robust domestic recovery.

By balancing a high-conviction share buyback program with an aggressive pivot toward investment banking and AI-driven operational efficiency, Barclays has managed to capture investor optimism even as the broader market grapples with geopolitical fragmentation. This momentum reflects a "re-rating" of the UK banking sector, where historically depressed valuations are finally being challenged by consistent capital returns and diversified revenue streams.

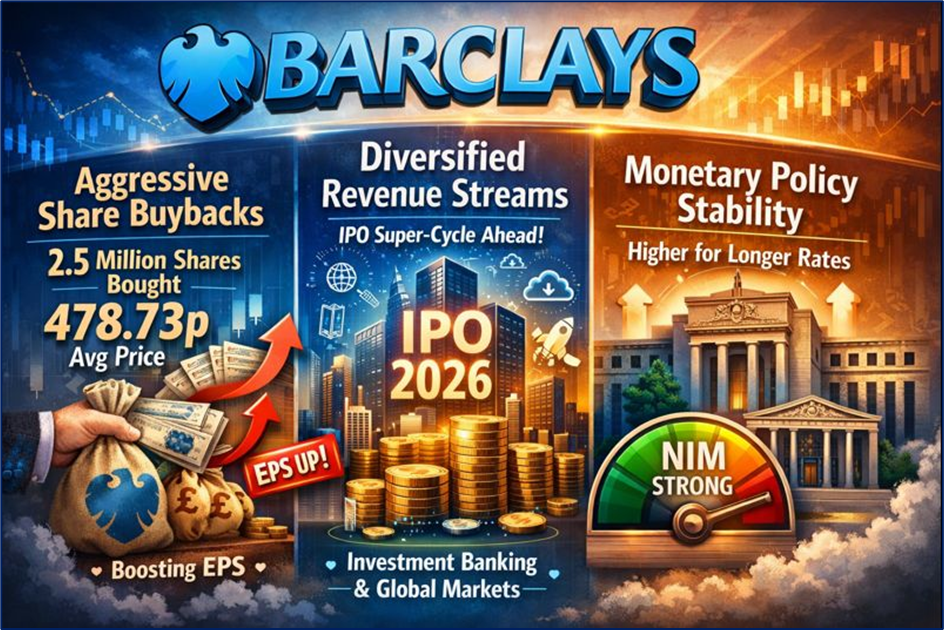

Latest Drivers of the Stock Surge

Source: Kalkine Group

The recent uptick in Barclays' share price is underpinned by a combination of aggressive capital management and favorable sector tailwinds:

- Aggressive Share Buybacks: A primary catalyst for the January 20 surge was the execution of the ongoing buyback program. On that day alone, Barclays purchased approximately 2.5 million shares for cancellation at an average price of 478.73p. This reduces the total share count, effectively increasing earnings per share (EPS) and tightening the equity base.

- Diversified Revenue Streams: Unlike pure-play retail banks, Barclays’ strength in investment banking and global markets is proving vital. Anticipation of a "super-cycle" in IPO activity for 2026—led by major tech entries—has positioned Barclays as a key beneficiary of rising corporate deal-making.

- Monetary Policy Stability: As the Bank of England and the Federal Reserve signal a "higher-for-longer" approach to terminal rates compared to previous cycles, the Net Interest Margin (NIM) for Barclays remains structurally supported, despite modest rate cuts expected later in the year.

Technical Analysis and Current Price Positioning

Source: Trading View

Based on market data as of January 21, 2026, Barclays is trading in a defined bullish corridor:

- Price Level: The stock is currently hovering around the 488p – 490p range, having successfully breached previous resistance levels near 475p.

- Trend Indicators: The stock remains well above its 50-day and 200-day Moving Averages, signaling sustained medium-term momentum.

- Volume and Volatility: Trading volume remains high, with over 108 million shares changing hands in recent sessions, indicating deep liquidity and institutional support for the current price levels.

Latest Analyst Coverages and Source Updates

Major financial institutions have recently refreshed their outlooks on Barclays, reflecting a generally optimistic consensus:

- TipRanks/Spark AI: Maintains an "Outperform" rating with a price target of £5.35, citing strong capital return metrics and strategic buybacks.

- HSBC/Standard Chartered Comparisons: In cross-sector notes, analysts at Barclays' own investment arm have recently upgraded peers like HSBC to "Overweight," which has historically signaled a rising tide for the entire UK banking "Big Four" cohort.

Current Business Model

Barclays operates a "Universal Banking" model, designed to capture value across the entire financial lifecycle:

- Barclays UK: Focuses on personal banking, mortgages, and wealth management within the British domestic market.

- Barclays International: Comprises the Corporate and Investment Bank (CIB) and Consumer, Cards, and Payments (CC&P). This segment provides a hedge against UK-specific downturns by tapping into US credit card markets and global capital markets.

- Strategic Transformation: The 2024–2026 strategy focuses on "Right-sizing" the investment bank to ensure it delivers a Return on Tangible Equity (RoTE) above 12% while reducing the group's overall cost-to-income ratio.

Dividend Analysis and Capital Returns

Barclays remains one of the FTSE 100’s most committed income stocks, with a clear roadmap for 2026:

- Capital Return Target: The bank is on track to return at least £10 billion to shareholders between 2024 and 2026 through a combination of dividends and buybacks.

- Dividend Strategy: The policy is to maintain the total dividend at stable absolute levels while growing the Dividend Per Share (DPS). This growth is achieved by reducing the total number of shares in issue via buybacks.

- Recent Payments: Following a 3.0p interim dividend in late 2025, the market is anticipating a final dividend announcement in early 2026, typically paid in April (Source: Barclays Investor Relations).

Barclays Financial and Operational Business Updates

- Share Capital Reduction: As of January 20, 2026, the issued share capital has been reduced to approximately 13.8 billion ordinary shares.

- AI Integration: Management has highlighted that over 53% of business leaders in their corporate ecosystem are now seeking investment specifically for AI, a trend Barclays is mirroring internally to automate back-office functions and enhance risk modeling.

- CET1 Ratio: The bank continues to operate within its target Common Equity Tier 1 (CET1) range of 13–14%, providing a significant buffer against market volatility.

Outlook and Risks

Outlook: For the remainder of 2026, Barclays guidance suggests a focus on "productivity." The bank expects to benefit from a recovery in the UK economy and a stabilization of global trade relationships.

Risks:

- Geopolitical Fragmentation: Continued tensions in global trade could impact the Investment Bank’s advisory and trading revenues.

- Inflationary Pressure: Stubbornly high inflation in the UK could lead to higher impairment charges if consumers struggle with debt servicing.

- Regulatory Changes: Potential shifts in UK capital requirements or windfall taxes remain a "headline risk" for the sector.

Conclusion

Barclays' performance on January 20, 2026, is a microcosm of its broader strategic success. By aggressively reducing its share count and positioning itself at the intersection of a recovering UK economy and a burgeoning global AI investment cycle, the bank has transitioned from a defensive play to a dynamic growth-and-income story. While risks regarding global debt and geopolitical stability persist, the bank’s disciplined capital return framework provides a clear floor for investor sentiment as it moves deeper into the 2026 fiscal year.

Please wait processing your request...

Please wait processing your request...