With UK mortgage rates finally easing and housing demand showing early signs of stabilisation, investors are rotating back into cyclical recovery plays. Among UK housebuilder stocks, Bellway is emerging as a front-runner in early 2026. But is BWY genuinely one of the biggest beneficiaries of falling rates — or is optimism running ahead of fundamentals?

Key Takeaways – Latest Month & Year (February 2026)

- Bellway shares surged ~4–5% on 10 February 2026, driven by a strong trading update and improving buyer sentiment.

- Early spring selling momentum has replaced a weak autumn, lifting reservations and enquiry volumes.

- Analyst price targets remain above current levels, signalling further upside potential.

- Dividend growth of ~9–11% is forecast, backed by a robust balance sheet and share buybacks.

- Risks persist from affordability pressures, macro uncertainty, and UK housing market volatility.

What Is Bellway Stock Doing Today, Up Around 4–5% on 10 February 2026?

In February 2026, Bellway has become one of the most closely watched names among UK housebuilders. The stock jumped approximately 4–5% following a confident trading update that highlighted improving reservation rates and renewed buyer engagement.

This move reflects growing optimism that the housing cycle is turning. As a FTSE 250 constituent, Bellway is highly sensitive to UK mortgage trends, making it a direct beneficiary of easing interest rates and improving affordability expectations.

Why Is Bellway Stock Rising Today and What Is the Current Trading Range?

BWY shares are currently trading in the 2,600p–2,700p range, hovering near recent 52-week highs. Trading volumes have increased, indicating renewed institutional and retail participation.

From a technical perspective:

- Momentum indicators suggest neutral-to-moderately bullish conditions

- Price action reflects confidence in near-term order growth and completions

- The stock is consolidating above key support levels, reinforcing positive sentiment

How Are the UK Economy and GBP Influencing Bellway’s Performance?

The UK macro environment in early 2026 remains finely balanced. Inflation has eased from prior peaks, wage growth has moderated, and the Bank of England is gradually shifting toward a more accommodative stance — all critical variables for housing demand.

Sterling volatility adds another layer:

- A weaker GBP can attract overseas property interest

- Domestic affordability, however, remains sensitive to real wage growth

Globally, equity markets are near record levels, supported by cyclical recovery optimism. Yet consumer confidence and interest-rate expectations remain key swing factors for UK housing stocks like Bellway.

What Are Analysts Saying About Bellway’s Dividend and Price Targets?

Consensus broker forecasts remain constructive:

- Median 12-month price target: ~3,150p

- Bull case: ~3,740p

- Bear case: ~2,600p

Dividend expectations are equally supportive. Forecasts point to a dividend of ~£0.77–£0.78 per share, representing 9–11% year-on-year growth. Strong cash generation, disciplined capital allocation, and ongoing buybacks underpin this outlook.

Is Bellway Stock Bullish, Bearish, or Neutral in 2026?

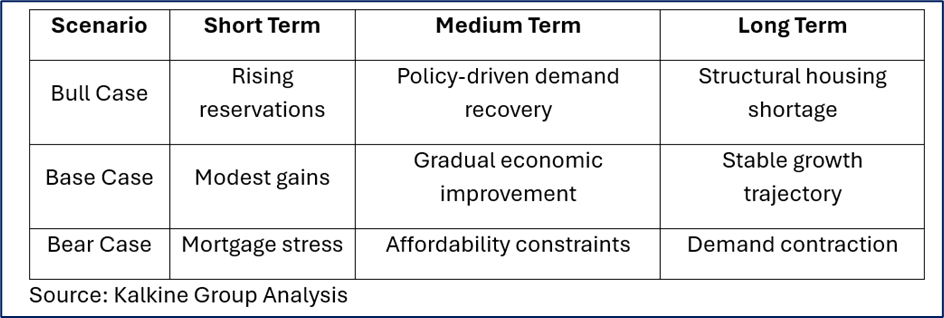

Short Term (0–6 months):

Bullish catalysts include seasonal sales acceleration and improving mortgage sentiment. Risks remain tied to affordability and consumer confidence.

Medium Term (6–24 months):

Performance depends on the pace of UK economic stabilisation and further rate cuts. Policy clarity and planning reforms could unlock stronger demand.

Long Term (2+ years):

Structural housing undersupply in the UK, demographic trends, and urbanisation support sustained long-term demand.

Overall stance:

- Bullish with supportive macro and policy tailwinds

- Neutral if mortgage costs plateau

- Bearish only under renewed economic stress or policy reversal

What Is Bellway’s Business Model and Latest Strategic Focus?

Bellway is a long-established UK residential developer with over seven decades of operating history. The company focuses on disciplined land acquisition, efficient build cycles, and shareholder returns.

Recent updates highlight:

- Growing housing completions

- Selective land buying at attractive valuations

- A £150m share buyback programme

- Dividend growth supported by earnings resilience

How Does Bellway Compare With Other UK Housebuilder Stocks?

Relative to peers:

- Vistry Group has struggled with operational setbacks and profit warnings

- Barratt Redrow offers scale advantages but carries different risk dynamics

Bellway’s conservative land strategy, capital discipline, and shareholder-friendly policies provide a more balanced risk-reward profile within the sector.

Bellway Stock Outlook: Short, Medium, and Long Term

Short-Term Drivers

- Early spring selling season momentum

- Improving consumer sentiment

- Planning policy clarity

Medium-Term Drivers

- Mortgage affordability improvements

- Order book growth and delivery execution

Long-Term Drivers

- Chronic UK housing undersupply

- Population and demographic trends

- Urban development demand

Bellway Scenario Analysis Matrix

What Are the Key Risks for Bellway Investors?

- Mortgage affordability and interest-rate uncertainty

- UK inflation affecting build costs

- Policy shifts in stamp duty or housing regulation

- Consumer confidence volatility

- Competitive pressures within UK housing

FAQ – Bellway Stock (SEO Optimised)

Is Bellway stock up today on the FTSE 250?

Yes. Bellway shares are up approximately 4–5% on 10 February 2026.

Is Bellway a good dividend stock?

Analysts expect rising dividends supported by strong cash flows and buybacks.

What is Bellway’s forecast price target?

The median 12-month target is around 3,150p.

How does the UK economy affect Bellway?

Mortgage rates, affordability, consumer confidence, and housing policy directly influence demand.

What is Bellway’s long-term outlook?

Long-term fundamentals remain supportive despite cyclical risks.

Final Investment View

Bellway’s February 2026 rally reflects improving confidence in the UK housing recovery narrative. With easing interest rates, rising dividends, disciplined capital management, and supportive analyst forecasts, BWY stands out as a compelling UK housebuilder stock for income-focused and cyclical investors alike. While macro risks remain, Bellway offers a well-balanced blend of recovery upside and shareholder returns as the housing cycle turns.

Please wait processing your request...

Please wait processing your request...