The FTSE 100 is witnessing a decisive rotation back into energy heavyweights today, with BP PLC (LSE: BP.) leading the charge as renewed geopolitical friction injects a premium back into crude markets. After weeks of listless trading driven by oversupply fears, the narrative has shifted overnight following fresh comments from the US administration regarding Iran, sparking fears of supply choke-points in the Strait of Hormuz.

For BP, a company that has aggressively streamlined its operations to lower its breakeven price, this sudden uptick in Brent crude acts as an immediate multiplier to free cash flow. Investors are bidding up the stock not just on today's oil price action, but on the realization that the "energy transition" trade was oversold, and the world’s reliance on secure, traditional hydrocarbons remains the dominant economic reality of 2026.

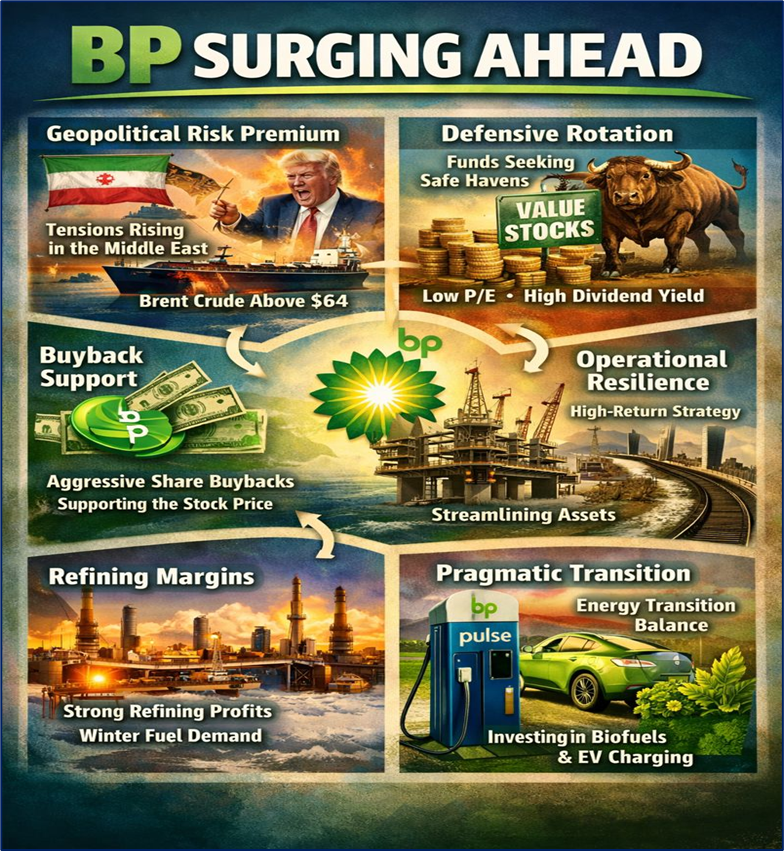

Latest Key Reasons for Surge

Source: Kalkine Group

- Geopolitical Risk Premium: The primary catalyst for today's surge is the sudden escalation in Middle East rhetoric. With President Trump's administration signaling a tougher stance on Iranian exports and potentially tightening sanctions, the market is pricing in a supply deficit. Brent Crude has rebounded firmly above the $64 support level, directly boosting sentiment for upstream producers like BP.

- Defensive Rotation: As broader markets face volatility from tech valuations and rate uncertainty, institutional capital is flowing into "value" sectors. BP, with its low P/E ratio and robust dividend yield, is attracting defensive inflows from fund managers seeking shelter in tangible assets.

- Buyback Support: BP's relentless share buyback program provides a constant floor under the stock price. The market reacts positively to the company's commitment to returning excess cash to shareholders, viewing dips as buying opportunities for the company itself.

- Operational Resilience: Despite a lower production environment globally, BP's recent trading update indicates that its "high-grading" strategy—selling expensive, low-margin assets and focusing on high-return barrels—is preserving margins.

- Refining Margins: While upstream oil gets the headlines, BP's downstream (refining and marketing) division is benefiting from resilient crack spreads, particularly as winter demand peaks in the Northern Hemisphere.

- Pragmatic Transition: The market continues to reward BP's nuanced approach to the energy transition. By slowing the decline of its oil and gas output while maintaining disciplined investment in bio-energy and EV charging (bp pulse), the company has aligned itself better with shareholder demands for near-term returns over long-term speculative growth.

Current Business Model: The "And" Strategy

BP operates as an Integrated Energy Company (IEC), a shift from the traditional International Oil Company (IOC) model.

- Hydrocarbons (The Cash Engine): This remains the core profit driver. It involves the exploration, development, and production of oil and natural gas. This segment funds the dividend and the transition.

- Convenience & Mobility: A massive retail network (gas stations, M&S Food partnerships, EV charging) that generates high Return on Capital Employed (ROCE) and provides stable cash flow less correlated to oil prices.

- Low Carbon Energy: Focused investments in offshore wind, hydrogen, and biofuels (specifically Sustainable Aviation Fuel - SAF). The model aims to transition revenue streams gradually without sacrificing current profitability.

Latest Company Financial & Operational Updates

(Source: BP plc Fourth Quarter 2025 Trading Statement, released 14 Jan 2026)

- Upstream Production: BP confirmed that upstream production for Q4 2025 was "broadly flat" compared to Q3, a solid result given maintenance schedules.

- Gas Trading: The company flagged that its gas marketing and trading result—often a "black box" of massive profits—is expected to be "average" for the quarter, tempering some exuberance but aligning with normalized markets.

- Divestments: A key highlight was the confirmation of divestment proceeds exceeding $4 billion for the year, significantly ahead of the $2-3 billion guidance. This directly aids in net debt reduction.

- Net Debt: Management reiterated its target to maintain a strong investment-grade credit rating, with net debt reduction remaining a priority before any additional increases in shareholder distributions.

- Upcoming Catalyst: The full Q4 and Full Year 2025 results are scheduled for release on 10 February 2026.

Dividend & Shareholder Return Status

(Source: BP Investor Relations, Jan 2026)

- Dividend Yield: Currently hovering around 5.6% - 5.8%, one of the most attractive in the FTSE 100.

- Payment Schedule: The next quarterly dividend is expected to be declared with the Q4 results in February, with payment likely in late March 2026.

- Buybacks: BP continues to execute its stated $1.75bn quarterly share buyback, systematically reducing the share count and artificially boosting Earnings Per Share (EPS).

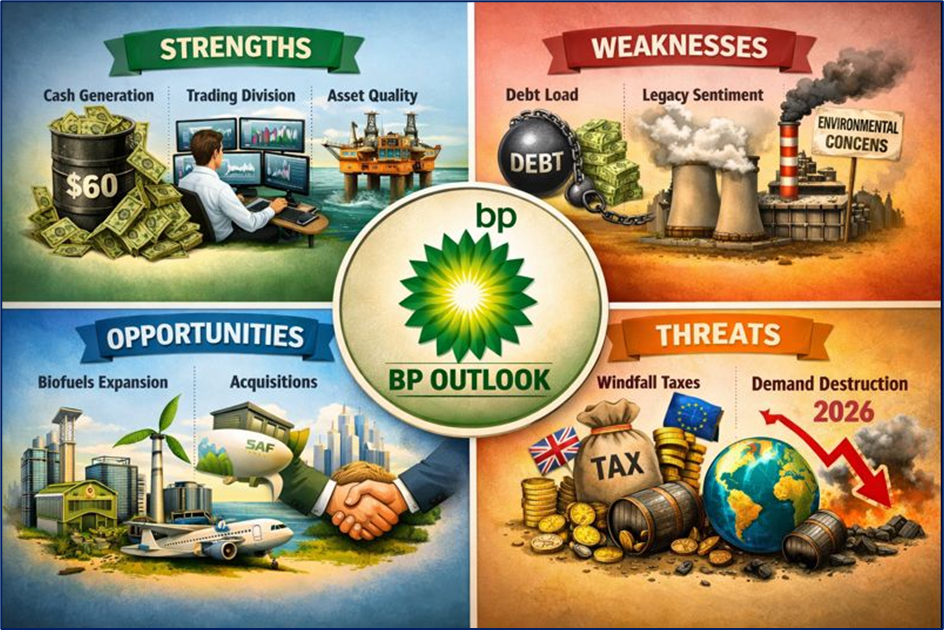

SWOT Analysis (January 2026)

Source: Kalkine Group

- Strengths:

- Cash Generation: Massive free cash flow capability even at $60/barrel oil.

- Trading Division: A world-class trading arm that can profit from market volatility, regardless of price direction.

- Asset Quality: A streamlined portfolio focused on high-margin regions like the Gulf of Mexico and the North Sea.

- Weaknesses:

- Debt Load: Net debt remains higher than peers like Shell or Chevron, limiting flexibility if oil crashes below $50.

- Legacy Sentiment: Still battles public perception issues regarding environmental impact, which can limit ESG fund ownership.

- Opportunities:

- Biofuels: Expansion into high-margin biofuels and SAF offers a growth runway that complements existing refining infrastructure.

- Acquisitions: With a stronger balance sheet, BP could look to acquire smaller, pure-play renewable or gas assets at distressed valuations.

- Threats:

- Windfall Taxes: The continued risk of UK or EU governments imposing higher levies on "excess" profits to fund fiscal deficits.

- Demand Destruction: A severe global recession in 2026 could crater oil demand, pushing prices below BP's breakeven targets.

Outlook & Risks

Outlook: The outlook for BP in Q1 2026 is cautiously bullish. The company has successfully navigated the "valuation trough" of 2025 and is now priced for resilience. Analysts expect the upcoming February earnings to show that while headline profits may have dipped year-on-year due to lower gas prices, the underlying cash flow remains robust enough to cover the dividend and buybacks comfortably. The focus remains on "value over volume."

Risks:

- Commodity Price Crash: If the geopolitical tension fades and OPEC+ floods the market, a drop to $50 Brent would severely squeeze BP’s buyback capacity.

- Regulatory Shock: New environmental mandates or carbon taxes could force higher capex spending, eating into free cash flow.

- Execution Risk: The transition to renewables is capital intensive and historically lower margin; failure to execute this pivot profitably is the long-term existential risk.

Compelling Conclusion

BP represents a classic "contrarian value" play in a market obsessed with growth. While it may lack the explosive potential of the tech sector, it offers something arguably more valuable in the current climate: tangible cash flow backed by real assets. Today's surge is a reminder that in a world of geopolitical uncertainty, energy security is paramount, and BP is one of the few global players capable of delivering it at scale. For the investor seeking a blend of high income (5.6% yield) and defensive insulation against market volatility, BP's current setup offers a compelling risk-reward proposition heading into the rest of 2026.

Please wait processing your request...

Please wait processing your request...