Is Centrica PLC shaping up as one of the FTSE 100’s most compelling income-and-value plays—or is the stock still hostage to energy-market cycles? As of February 2026, Centrica is back in focus as investors rotate toward defensive, cash-generative businesses with visible dividends, buybacks, and infrastructure optionality.

Key Takeaways — February 2026 Snapshot

Source: Kalkine Group

- Centrica shares (LSE: CNA) advanced roughly +1.4% on 6 February 2026, extending positive momentum ahead of earnings and reflecting renewed confidence in UK utilities.

- Dividends and buybacks remain central to the investment case, with consensus forecasts pointing to ~20–22% dividend growth in the next fiscal year.

- FTSE 100 resilience, led by energy and “old-economy” stocks, is cushioning portfolios amid global tech volatility.

- UK macro conditions are stabilising, with easing inflation, expected rate cuts, and manufacturing PMI back in expansion territory.

- Sell-side sentiment skews constructive, dominated by Buy/Hold ratings and fair-value estimates above current prices.

- Clear bull, base, and bear scenarios highlight the trade-off between income visibility and energy-price risk.

- Actionable strategies outlined for short-term traders, medium-term value investors, and long-term income holders.

How Is Centrica Stock Performing in the FTSE 100 Right Now?

- Centrica is trading near multi-month highs, reflecting a renewed bid for defensive, income-generating equities.

- The +1.4% daily move on 6 Feb 2026 highlights strong technical support and positioning ahead of results.

- Year-to-date and 52-week trends show a meaningful recovery from last year’s lows, reinforcing improving sentiment.

Market backdrop: The FTSE 100 has held firm as investors respond to dovish signals from the Bank of England, favouring energy, utilities, and consumer defensives over high-beta tech.

Dividend Outlook: Is Centrica Still an Income Stock?

- Current dividend yield sits in the ~2.5%–3.8% range, competitive within UK utilities.

- Analysts expect ~22% dividend growth over the next fiscal periods, supported by:

- Robust free cash flow

- Conservative payout ratios

- Ongoing share buyback programmes

- Total shareholder returns are enhanced by capital discipline, not just headline yield.

For UK income investors, Centrica screens well versus peers on yield sustainability rather than yield alone.

UK & Global Macro Landscape — February 2026

UK Economy

- Policy rates held at 3.75%, with guidance pointing toward future cuts.

- Inflation is easing, though still above target.

- Manufacturing PMI has moved back into expansion, signalling selective economic resilience.

Sterling & Markets

- GBP has softened modestly on dovish expectations, supporting internationally exposed earnings.

- FTSE 100 benefits from global revenue exposure, while the FTSE 250 is leveraged to a domestic recovery and lower borrowing costs.

Centrica Business Model & Strategic Drivers

Centrica operates across integrated energy supply and services, anchored by British Gas and complemented by trading, optimisation, and infrastructure exposure.

Key growth and support factors:

- Improved operational efficiency and customer retention

- Participation in Sizewell C nuclear development

- Early-stage positioning in hydrogen and energy transition assets

- Consistent capital returns via dividends and buybacks

Key risks to watch: earnings sensitivity to gas prices, regulatory shifts, and periodic infrastructure write-downs underscore that energy cyclicality still matters.

Analyst Consensus & Forecast Trends

- Most analysts maintain Buy or Hold ratings.

- Average 12-month fair-value estimates sit above current trading levels.

- Dividend per share forecasts show double-digit growth expectations into upcoming fiscal years.

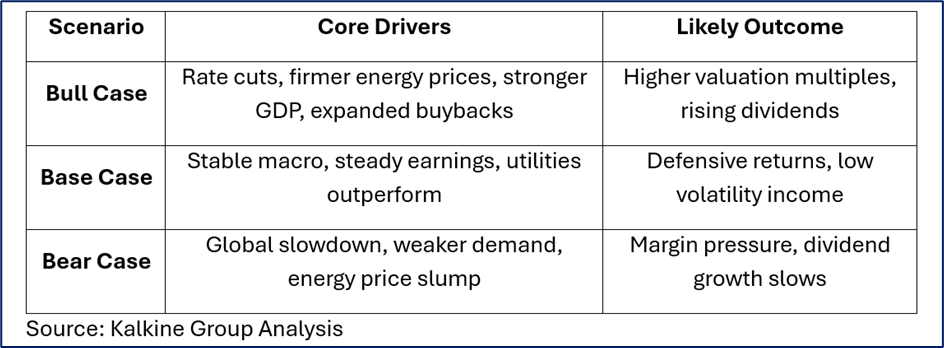

Scenario Framework (Risk-Balanced View)

Investor Playbook by Time Horizon

Short Term (0–6 months)

- Trade around earnings, CPI prints, and BoE policy updates

- Monitor GBP and energy-price volatility

Medium Term (6–18 months)

- Accumulate on valuation-driven pullbacks

- Track infrastructure milestones and capital-return announcements

Long Term (18+ months)

- Focus on dividend compounding

- Evaluate nuclear and hydrogen exposure as structural growth options

Balanced View: Bullish vs Bearish

Why bulls like Centrica

- Defensive cash flows in uncertain markets

- Growing dividends plus buybacks

- Strategic exposure to UK energy infrastructure

Why bears stay cautious

- Commodity-linked earnings volatility

- Regulatory and political risk

- Dependence on UK economic momentum

High-Intent FAQs (Search-Optimised)

Why is Centrica up today in the FTSE 100?

Utility rotation and defensive demand amid global volatility.

Is Centrica good for dividend investors in 2026?

Consensus supports dividend growth, but risk tolerance matters.

How does the UK macro outlook affect Centrica shares?

Rates, inflation, and sterling directly influence valuations and sentiment.

Final Take — Informational, Not Predictive

As of February 2026, Centrica presents a credible income-and-value proposition within the FTSE 100. Supportive macro trends, disciplined capital returns, and strategic infrastructure exposure strengthen its defensive appeal. However, investors should balance dividend optimism against the realities of energy-market cyclicality and UK economic sensitivity. For diversified portfolios, Centrica offers multiple ways to participate—across trading, value, and long-term income strategies—without relying on a single macro outcome.

Please wait processing your request...

Please wait processing your request...