Discover whether DCC plc’s diversified energy, healthcare, and technology distribution operations can deliver sustainable dividend growth, resilient free cash flow, and long-term total shareholder returns for FTSE 100 investors in 2026 and beyond.

Key Takeaways – February 2026 Update

- Why is DCC stock up ~3.8% on 12 February 2026? Positive Q3 trading sentiment, strong dividend appeal, and FTSE 100 momentum amid currency tailwinds are likely drivers.

- What is the 2026–27 dividend outlook? 29 consecutive years of dividend growth and an attractive ~4.5% yield support income investors.

- How is GBP impacting FTSE 100 stocks like DCC? A softer pound boosts overseas earnings translation and enhances competitiveness.

- Is DCC bullish or bearish right now? Fundamentally constructive long term, with short-term volatility tied to macro data and execution risks.

- What should investors consider now? Short-term momentum, medium-term dividend compounding, and long-term strategic energy growth positioning.

Source: Kalkine Group

Why Is DCC PLC (FTSE 100: DCC) Stock Up ~3.8% on 12 February 2026?

Shares of DCC plc advanced approximately 3.8% intraday on 12 February 2026, outperforming sections of the broader FTSE 100. The rally appears supported by:

- Improved investor sentiment following trading updates

- Continued demand for high-yield defensive dividend stocks

- Relative GBP weakness enhancing overseas revenue translation

- Broader index momentum amid global macro recalibration

As a globally diversified distributor with significant exposure to energy markets, DCC often benefits when investors rotate toward cash-generative, internationally diversified FTSE blue chips.

What Global & UK Macro Forces Are Supporting FTSE 100 Stocks?

In February 2026, global equity markets are reacting to:

- Inflation moderation trends

- Interest rate trajectory expectations

- Commodity price resilience

- Currency fluctuations

The FTSE 100, with its multinational revenue base, tends to benefit from:

- A softer British pound

- Energy and commodity-linked earnings strength

- Defensive income-seeking capital flows

For DCC, which generates substantial international revenues, currency dynamics and energy demand trends can materially influence earnings translation and margin stability.

What Is DCC’s Dividend Outlook for 2026 and Beyond?

DCC remains one of the more consistent dividend performers in the FTSE 100, with:

- 29 consecutive years of dividend growth

- A forward yield of approximately 4.5%

- Strong free cash flow generation supporting distributions

Dividend sustainability appears underpinned by:

- Recurring energy distribution revenues

- Capital discipline

- Portfolio optimisation initiatives

While payout ratios warrant monitoring, long-term income investors often prioritise DCC’s track record of incremental annual increases.

How Does DCC Compare With FTSE 100 & FTSE 250 Peers?

Relative to both the FTSE 100 and the FTSE 250:

- DCC offers a higher-than-average dividend yield

- Free cash flow yield remains competitive

- Earnings volatility is typically lower than cyclical industrials

Unlike more cyclical UK industrial names, DCC operates in essential distribution markets, providing a degree of structural resilience.

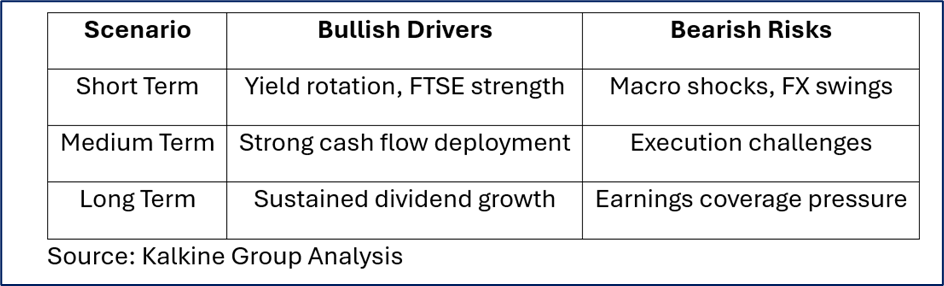

Is DCC Stock Bullish, Bearish, or Neutral in 2026?

Bullish Catalysts

- Long-term dividend growth credibility

- Strong free cash flow conversion

- Strategic focus increasingly weighted toward energy

- FTSE 100 macro tailwinds

Bearish or Neutral Risks

- Dividend payout coverage must remain sustainable

- Portfolio restructuring execution risk

- Currency volatility impacting earnings translation

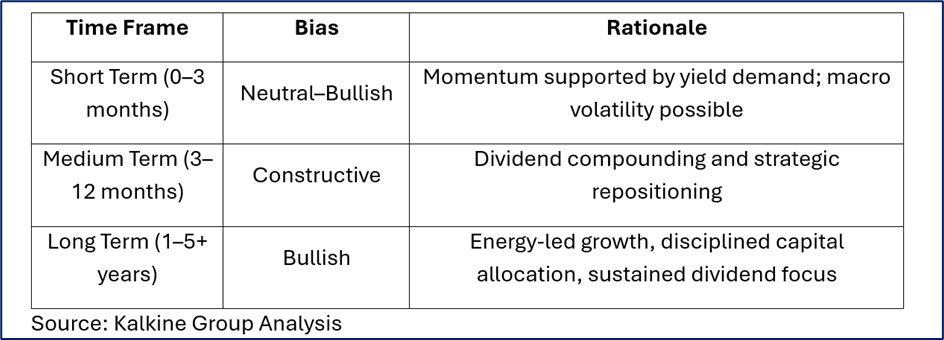

Outlook by Time Horizon

What Strategies Could Investors Consider?

Short Term (3–6 Months)

- Track GBP movements and UK macro releases

- Monitor quarterly earnings momentum

- Consider hedging strategies in volatile conditions

Medium Term (6–12 Months)

- Focus on dividend reinvestment strategies

- Evaluate capital allocation from divestments

- Assess margin trends in energy operations

Long Term (1–5+ Years)

- Prioritise dividend compounding and cash flow durability

- Benchmark against global energy distribution peers

- Monitor structural demand in energy transition markets

Bull vs Bear Scenario Matrix

What Do Analysts Indicate About Future Valuation?

Consensus sentiment typically views DCC as:

- A stable dividend compounder

- Moderately valued relative to free cash flow generation

- Positioned for steady, rather than aggressive, capital appreciation

Analyst commentary often highlights reliability over high-beta growth characteristics.

What Are the Key Risks for Investors?

- Dividend sustainability relative to earnings coverage

- Integration and divestment execution risks

- Energy demand cyclicality

- Currency exposure across operating geographies

FAQ – DCC PLC Stock & Dividend Outlook 2026

Why did DCC stock rise 3.8% on 12 February 2026?

Positive trading sentiment, FTSE 100 momentum, and favourable currency dynamics likely contributed.

Is DCC a strong long-term dividend stock?

Its 29-year dividend growth streak and strong free cash flow profile make it attractive for income-focused portfolios.

Is DCC suitable for 2026 investors?

For those prioritising dividend stability and moderate growth within the FTSE 100, DCC offers a balanced risk-return profile.

Final Investment Perspective – Is DCC a Hidden FTSE 100 Compounder?

DCC plc combines defensive dividend consistency, international earnings diversification, and energy-sector positioning, making it a compelling candidate for investors seeking steady total returns in 2026.

The February rally reflects broader FTSE 100 dynamics rather than purely speculative movement. While short-term volatility remains possible, DCC’s foundation—rooted in disciplined capital allocation and long-term dividend growth—supports its profile as a potential FTSE 100 compounder for income-focused portfolios.

As always, investment decisions should align with individual risk tolerance, time horizon, and portfolio diversification objectives.

Please wait processing your request...

Please wait processing your request...