Endeavour Mining continues to trade below its long-term valuation range even as gold prices remain elevated and free cash flow momentum accelerates. With investors rotating back into defensive, income-generating assets in early 2026, the key question is whether the market is underestimating the earnings power and dividend resilience of this FTSE 100-listed gold producer.

Key Takeaways (Updated: February 2026)

- Strong near-term momentum: Endeavour Mining shares climbed roughly +5.9% on 9 February 2026, outperforming the FTSE 100 and most global gold peers.

- Gold leverage back in focus: Elevated bullion prices, robust margins, and consistent execution are restoring confidence in high-quality gold miners.

- Dividend strength reaffirmed: A progressive dividend policy, backed by free cash flow, supports Endeavour’s appeal to income-oriented investors.

- Macro tailwinds remain supportive: Sticky inflation, softer real yields, GBP volatility, and renewed safe-haven demand are lifting gold equities.

- Balance-sheet discipline: Conservative leverage and a clear shareholder-returns framework remain central to the 2026 investment case.

Source: Kalkine Group

Why Did Endeavour Mining Shares Rise Nearly 6% in February 2026?

The sharp move higher in Endeavour Mining shares reflects a convergence of favourable drivers: strong gold prices, disciplined operational performance, and improving sentiment toward defensive assets. As inflation uncertainty and geopolitical risks persist, investors are reallocating capital toward cash-generative, dividend-paying miners—an area where Endeavour stands out.

Investor search activity in February 2026 reinforces this trend. High-intent terms such as UK gold stocks, FTSE 100 mining shares, inflation hedge equities, safe-haven investments, dividend gold miners, and West Africa gold production increasingly align with Endeavour Mining’s equity story.

In parallel, renewed inflows into the FTSE 100—driven by global diversification and defensive positioning—have provided additional support for Endeavour’s share price momentum.

How Are Global Markets and the UK Economy Shaping Gold Stocks in 2026?

The macro backdrop in early 2026 is defined by uneven global growth, persistent geopolitical risk premiums, and shifting interest-rate expectations. Against this backdrop, gold has reasserted its role as a store of value and portfolio hedge—directly benefiting established producers.

For UK investors, the FTSE 100’s international revenue exposure is a key advantage. Endeavour Mining’s US dollar-linked revenues and West African operations reduce reliance on UK domestic demand, offering insulation from local economic softness.

At the same time, heightened GBP volatility enhances the appeal of globally diversified miners. Currency fluctuations can boost translated earnings, reinforcing the defensive characteristics of FTSE 100-listed gold equities.

What Is Happening in the Gold Mining Sector—and Why Does Endeavour Mining Stand Out?

In 2026, investors are no longer rewarding gold miners for aggressive production growth alone. Instead, the market is prioritising:

- Free cash flow generation

- Cost discipline and margin protection

- Balance-sheet strength

- Sustainable shareholder returns

Endeavour Mining distinguishes itself through:

- Large-scale, diversified operations across West Africa

- Competitive all-in sustaining costs, supporting margins through gold price cycles

- Disciplined capital allocation, balancing reinvestment with dividends

This approach places Endeavour alongside global leaders such as Barrick Gold, Newmont, and AngloGold Ashanti, while offering a distinctive FTSE 100-listed income profile.

What Does Endeavour Mining’s Business Model Signal in February 2026?

Endeavour Mining operates a focused, pure-play gold production model built around efficiency, margin protection, and disciplined growth. Recent updates continue to highlight:

- Stable production guidance supported by long-life reserves

- Strong free cash flow conversion at current gold prices

- Ongoing commitment to progressive dividends

Management’s preference for asset optimisation over large-scale acquisitions aligns closely with prevailing institutional investor preferences.

How Attractive Is Endeavour Mining’s Dividend Outlook for 2026?

Gold equities are regaining favour among income investors in 2026, and Endeavour Mining’s progressive dividend framework positions it as a hybrid growth-and-income opportunity. While dividends remain linked to gold prices and cash generation, the policy is explicitly designed to reward shareholders across the cycle.

For UK income portfolios seeking diversification beyond banks, energy, and consumer staples, Endeavour offers inflation-resilient income with additional upside from gold price strength.

Bullish or Bearish? Endeavour Mining Across Investment Horizons

Short term (3–6 months):

- Bias: Bullish to Neutral

- Rationale: Gold momentum, supportive technicals, and FTSE 100 inflows underpin upside, though volatility may follow sharp gains.

Medium term (6–18 months):

- Bias: Constructively Bullish

- Rationale: Sustained cash flows, dividends, and disciplined execution align with late-cycle macro conditions.

Long term (3+ years):

- Bias: Neutral to Bullish

- Rationale: Structural gold demand and reserve quality are supportive, while geopolitical and regulatory risks require monitoring.

What Investment Strategies Make Sense in 2026?

Short-term traders:

- Tactical exposure to gold-driven momentum

- Tight risk management due to commodity volatility

Medium-term investors:

- Accumulate on pullbacks to capture dividends and cash-flow yield

- Use gold miners as macro hedges

Long-term holders:

- Maintain exposure within a diversified real-assets allocation

- Focus on dividend reinvestment and balance-sheet quality

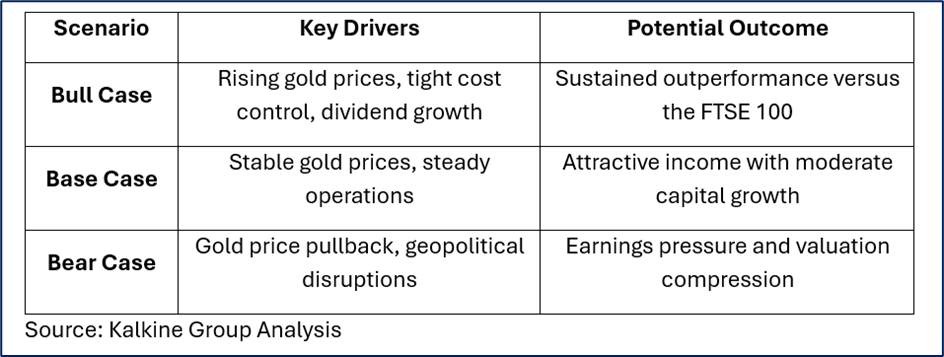

Bull, Base, and Bear Scenarios for Endeavour Mining in 2026

What Is the Analyst Consensus in February 2026?

Broker sentiment remains broadly constructive, with analysts highlighting:

- Strong leverage to gold prices

- Competitive cost structure

- Consistent shareholder returns

Most coverage positions Endeavour Mining as a core large-cap gold holding, rather than a speculative mining play.

Key Risks Investors Should Watch

- Gold price volatility and real-rate movements

- Political and regulatory developments in operating regions

- Operational disruptions or cost inflation

- Currency fluctuations impacting reported earnings

Final Verdict: Is Endeavour Mining Still Undervalued After Its 5.9% Rally?

Endeavour Mining’s February 2026 surge reinforces its position as a cash-generative, dividend-paying FTSE 100 gold miner well aligned with today’s macro environment. While sector risks remain unavoidable, its operational discipline, balance-sheet strength, and direct leverage to gold prices suggest the market may still be undervaluing its medium- to long-term potential.

For investors seeking income diversification, defensive growth, and inflation protection, Endeavour Mining remains firmly on the 2026 watchlist.

Please wait processing your request...

Please wait processing your request...