Halma has built a reputation as a high-quality FTSE 100 compounder. With strong margins and disciplined acquisitions, can it keep delivering long-term growth?

Key Takeaways – February 2026 (Latest Market Update)

- Halma share price jumped around 3% on 13 February 2026, outperforming sections of the FTSE 100

• Defensive growth rotation across UK equities is accelerating amid global macro volatility

• Strong recurring revenue, high margins, and disciplined acquisitions continue to attract institutional flows

• Long-standing dividend growth track record reinforces its status as a premium UK compounder

• Analysts remain broadly constructive despite elevated valuation multiples

Source: Kalkine Group

Why Is Halma Stock Rising 3% Today and Dominating UK Stock Market Headlines in February 2026?

Halma share price is trending sharply higher today as investors aggressively rotate into defensive FTSE 100 dividend growth stocks, high-quality UK compounders, recession-resilient technology shares, and safety-focused global leaders amid global economic uncertainty, shifting interest rate expectations, and currency volatility in February 2026.

As the UK economy navigates moderate GDP growth, cooling inflation pressures, evolving Bank of England policy guidance, and relative GBP stability, investors are prioritising predictable earnings visibility, recurring revenue models, high return on capital employed (ROCE), strong free cash flow generation, and global revenue diversification — all of which define Halma’s investment profile.

With global equity markets experiencing mixed momentum and capital rotating away from cyclical sectors toward quality defensive growth names, Halma is emerging as a prime beneficiary of this capital reallocation theme across the UK stock market.

What Are the Core Catalysts Driving Halma’s February 2026 Share Price Surge?

The latest momentum appears supported by multiple structural and tactical drivers:

- Defensive sector rotation within the FTSE 100

• Continued demand for environmental monitoring, safety compliance, and healthcare technology solutions

• Strong balance sheet flexibility enabling bolt-on acquisitions

• Resilient organic revenue growth across international markets

• Sustained dividend growth confidence

Halma’s decentralised acquisition-led growth model — focused on niche, mission-critical safety and environmental technologies — provides stability even during broader economic slowdowns (Company interim and annual trading updates).

How Are the UK Economy, GBP Trends and Broader FTSE Indices Influencing Halma’s Performance?

Is the UK Economic Backdrop Favouring Defensive Global Leaders?

The UK macro environment in February 2026 remains cautiously stable:

- Inflation moderating but not fully at target

• Interest rate outlook gradually shifting toward stability

• Consumer activity mixed but resilient

• GBP relatively stable against major currencies

This backdrop typically benefits internationally diversified FTSE 100 constituents like Halma, whose revenue exposure extends far beyond domestic UK demand.

Is the FTSE 100 Outperforming the FTSE 250 in the Current Market Cycle?

Yes, large-cap defensive exporters within the FTSE 100 are showing stronger relative performance compared to the more UK-centric FTSE 250. As capital flows favour quality and earnings resilience, Halma’s positioning within the blue-chip index enhances its defensive appeal.

What Makes Halma’s Business Model So Structurally Resilient in 2026?

Halma operates across three strategic growth segments:

- Safety technologies

• Environmental & analysis solutions

• Healthcare diagnostics and medical devices

Its competitive strengths include:

- Asset-light, high-margin operations

• Recurring revenue streams from regulatory compliance needs

• Strong cash conversion

• Proven acquisition integration track record

• Decentralised entrepreneurial management structure

The company’s focus on mission-critical applications — where safety, regulation, and compliance are non-negotiable — creates durable demand regardless of macro cycles.

What Do the Latest Financial and Dividend Signals Reveal?

Recent company-released financial updates highlight:

- Organic revenue growth supported by pricing power and innovation

• Healthy adjusted operating margins

• Robust return on invested capital

• Continued progressive dividend increases

Halma’s multi-decade record of annual dividend growth reinforces its reputation as a premium UK dividend growth stock suitable for long-term compounding portfolios.

How Does Halma Compare to Global Industrial and Technology Peers?

Peer benchmarking indicates:

- Higher valuation multiple due to earnings visibility and consistency

• Lower earnings volatility versus heavy industrial peers

• Stronger margin resilience

• Superior capital allocation discipline

While valuation remains elevated relative to cyclical industrial stocks, investors often justify the premium for predictability and structural growth exposure.

What Is the Short-Term, Medium-Term and Long-Term Investment Outlook?

Is Halma Bullish in the Short Term?

Short-term outlook (3–6 months): Neutral to moderately bullish

Drivers:

- Defensive capital rotation

• Stable earnings expectations

• Reduced macro volatility

Risks:

- Premium multiple sensitivity to interest rate surprises

• Currency fluctuations impacting reported earnings

Is Halma Attractive in the Medium Term?

Medium-term outlook: Constructively bullish

Drivers:

- Continued bolt-on acquisitions

• Environmental regulation tailwinds

• Healthcare diagnostics demand

• Infrastructure and compliance spending

Is Halma a Long-Term Structural Compounder?

Long-term outlook: Strongly bullish structural thesis

Drivers:

- Secular global safety standards tightening

• Climate and environmental monitoring demand growth

• Expanding healthcare technology needs

• Disciplined capital allocation and dividend reinvestment potential

What Forward-Looking Strategies Can Investors Consider?

Short-Term Strategy

- Consider gradual accumulation during volatility

• Monitor macro policy commentary

• Track organic growth trends

Medium-Term Strategy

- Maintain core holding

• Reinvest dividends

• Evaluate acquisition pipeline execution

Long-Term Strategy

- Hold as defensive growth allocation

• Apply pound-cost averaging

• Focus on total shareholder return compounding

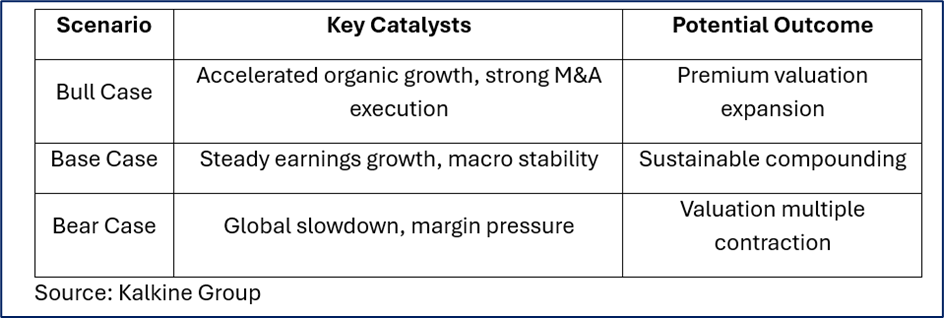

What Does Scenario Analysis Suggest?

What Are Leading Analysts Indicating in February 2026?

Broker consensus sentiment (latest publicly available summaries):

- Barclays – Overweight

• JPMorgan – Neutral

• UBS – Buy

• Morgan Stanley – Equal Weight

While price targets vary, consensus reflects confidence in Halma’s long-term quality profile, balanced by valuation awareness.

What Key Risks Should Investors Monitor?

- Elevated valuation compression risk

• Acquisition integration challenges

• FX volatility

• Regulatory shifts

• Global economic deceleration

Is Halma Stock Bullish, Bearish or Neutral Right Now?

Short term: Neutral-to-bullish bias driven by defensive flows

Long term: Bullish structural outlook supported by recurring revenue, global diversification, and dividend growth momentum

This remains analytical commentary for informational purposes only.

Frequently Asked Questions About Halma Stock in February 2026

Why is Halma share price rising today?

Defensive capital flows and resilient earnings outlook.

Is Halma a strong dividend growth stock?

Yes, supported by consistent cash flow and progressive dividend increases.

Is the stock expensive?

It trades at a premium reflecting quality and earnings stability.

Which sectors does Halma operate in?

Safety technology, environmental monitoring, and healthcare diagnostics.

What Is the Final Investment Conclusion for February 2026?

Halma continues to stand out as a high-quality FTSE 100 defensive growth stock, global safety technology leader, dividend growth compounder, and ESG-aligned environmental solutions provider. While short-term upside may be moderated by valuation considerations, the company’s structural resilience, regulatory-driven demand, acquisition discipline, and global revenue diversification support a compelling long-term investment thesis.

For investors seeking stable UK dividend stocks, recession-resilient global equities, long-term compounding returns, and defensive growth exposure in 2026, Halma remains analytically attractive.

Please wait processing your request...

Please wait processing your request...