The London energy scene just got a jolt. On January 6, 2026, Harbour Energy (LSE: HBR) shares climbed approximately 3%, defying broader FTSE volatility. For retail investors and market analysts alike, the move signals a potential "thaw" in investor sentiment toward the UK’s largest independent producer.

But what exactly is fueling this engine? From aggressive share buybacks to a radical shift in their global business model, here is the analytical deep dive into Harbour Energy’s latest updates.

Key Drivers: What Pushed the Stock Up Today?

Source: Kalkine Group

The 3% uptick on January 6 is not a random fluctuation; it is the result of a "perfect storm" of corporate strategy and shifting political winds.

- Aggressive Share Buybacks: On January 5, Harbour confirmed the purchase of 589,626 shares for cancellation as part of its ongoing buyback program. This reduces share supply and signals management’s belief that the stock is currently undervalued.

- The "Exit the UK" Narrative Gains Traction: Investors are increasingly pricing in the company’s reduced exposure to the UK's punitive 78% Energy Profits Levy (EPL). With the massive Wintershall Dea integration now operational and the recent $3.2 billion LLOG Exploration deal in the US Gulf of Mexico, Harbour is no longer just a "North Sea play."

- Sector Momentum & Policy Hope: Industry bodies (OEUK) and unions have intensified pressure on the Labour government to reconsider the ban on new exploration licenses. Any hint of fiscal stability in the UK creates an immediate relief rally for HBR.

Latest Business Model: From North Sea King to Global Major

Harbour Energy has undergone a "silent revolution." Its 2026 business model is built on three distinct pillars that separate it from the Premier Oil/Chrysaor days:

- Geographic Diversification: By acquiring Wintershall Dea and LLOG, Harbour has shifted its production weight. It now holds significant assets in Norway, Germany, Argentina, Mexico, and the USA.

- The 500 kboepd Ambition: The company is now a "mini-major," targeting production levels near 500,000 barrels of oil equivalent per day.

- Low-Tax Jurisdiction Focus: Every dollar invested in the US Gulf of Mexico (taxed at ~23%) or Norway is seen as infinitely more valuable than a dollar trapped in the UK’s high-tax regime.

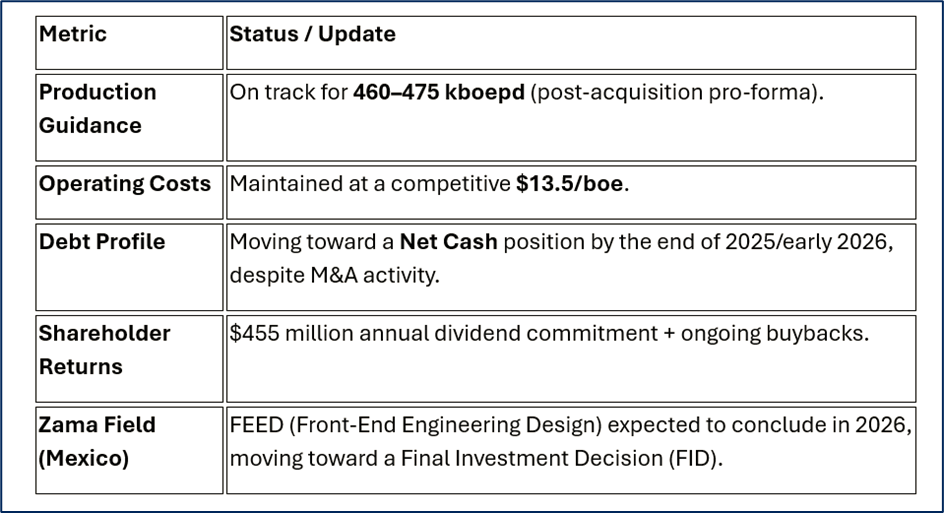

Financial & Operational Updates (Jan 2026)

Source: Company Data

SWOT Analysis: The 2026 Reality Check

Source: Kalkine Group

Strengths

- Scale: Largest UK independent with "Investment Grade" credit potential.

- Cost Efficiency: Unit operating costs are among the lowest in the sector.

- Diversified Portfolio: Less than 50% of production is now tied to UK fiscal risk.

Weaknesses

- Leverage Concerns: The $3.2bn LLOG deal increased near-term debt and caused slight equity dilution.

- Complexity: Managing assets across four continents introduces operational friction.

Opportunities

- US Listing Rumors: Speculation persists about a primary listing move to the US (NYSE), which could re-rate the stock to higher US multiples.

- CCS Leadership: A dominant position in European Carbon Capture and Storage (CCS) projects like Viking and Acorn.

Threats

- Windfall Tax Longevity: If the UK EPL is extended or tightened further, it remains a drag on the remaining North Sea assets.

- Commodity Volatility: While HBR has a lower break-even, a global recession could push Brent below $65/bbl, squeezing margins.

Key Risks to Watch

- Political Risk: The "Labour Factor" in the UK remains the #1 wildcard.

- Integration Risk: Merging the Wintershall Dea and LLOG cultures and systems is a massive undertaking that could see "hiccups" in operational reporting.

- The "Laffer Curve" Effect: As seen in recent reports, the high UK tax is yielding less revenue because companies are slashing investment. If Harbour cuts UK spending further, its legacy production could decline faster than expected.

Conclusion

Harbour Energy’s 3% rise on January 6 reflects a market that is starting to appreciate the "New Harbour." By diversifying away from the UK’s fiscal volatility and focusing on high-margin international assets, the company is attempting to trade more like a global energy giant and less like a regional utility.

With a 2026 trading update scheduled for later this month (Jan 22), all eyes will be on whether the free cash flow from their new US and Norwegian assets can sustain the aggressive buyback pace that fueled today's gain.

Please wait processing your request...

Please wait processing your request...