-Copy_01_30_2026_17_00_02_241315.jpg)

Key Takeaways – Lloyds Banking Group Share Update (January 2026)

- Earnings Beat: Lloyds delivered a 12% year-on-year rise in statutory profit before tax, reaching £6.7bn for FY2025, comfortably ahead of consensus forecasts of £6.4bn.

- Shareholder Windfall: Management launched a £1.75bn share buyback from 30 January 2026 and raised the ordinary dividend by 15% to 3.65p per share.

- Best-in-Class Efficiency: The bank is targeting a sub-50% cost-to-income ratio by 2026, placing Lloyds among the most efficient retail banks in Europe.

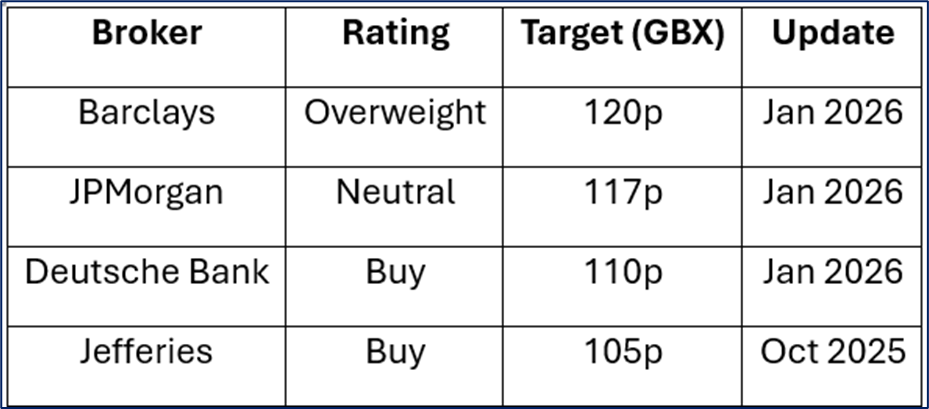

- Analyst Upgrades: Major brokers have lifted price targets, with bullish scenarios pointing toward 120p upside.

Will Lloyds Shares Rally Further in 2026? UK Economy & Market Outlook

The FTSE 100 crossing 10,000 in January 2026 marks a historic breakout for UK equities. Despite global macro uncertainty, the UK economy is proving resilient, with GDP growth projected at 1.2% for 2026.

The Bank of England’s gradual rate-cutting cycle has created a near-perfect environment for UK lenders—supporting borrowers while preserving net interest margins (NIMs).

For Lloyds, the UK’s largest mortgage lender, this backdrop is highly favourable. A weaker pound near $1.37–$1.38 has also made UK bank valuations increasingly attractive to global institutional investors. As inflation cools toward target, Lloyds’ operational leverage is starting to shine.

Peer Comparison: Lloyds vs Barclays, HSBC, and NatWest

Within the UK banking sector, Lloyds stands out as a pure-play domestic retail leader, avoiding the volatility tied to global investment banking exposure.

Key competitive advantages:

- Return on Tangible Equity (RoTE):

- FY2025: 12.9%

- 2026 guidance upgraded to above 16%, outperforming peers

- Capital Generation: Over 200bps superior capital creation versus NatWest, according to recent broker commentary

- Income Strength: Dividend yield trending toward 4%, offering dependable income in volatile markets

- Valuation Re-rating: Trading near 18x earnings, Lloyds is increasingly viewed as a digitally enabled growth bank, not a legacy lender

Lloyds Share Price Outlook: Short, Medium & Long Term

Short Term (0–6 Months): Bullish

The £1.75bn buyback now underway provides a powerful technical tailwind by reducing share count and supporting valuation. Momentum from the January earnings surprise is likely to carry into Q1 2026.

Medium Term (6–18 Months): Neutral to Bullish

Investor focus will shift to net interest margins, guided at 3.06%, supported by Lloyds’ structural hedge.

The main overhang remains the FCA motor finance investigation, though the bank has already provisioned £800m, limiting downside risk.

Long Term (2+ Years): Bullish

Lloyds is rapidly evolving into a digital-first financial ecosystem. With 21.5 million active digital users, the bank is expanding into capital-light revenue streams such as insurance, wealth, and embedded finance.

Management is targeting £2bn in incremental annual revenue by end-2026, a potential catalyst for a material valuation re-rating.

Latest Lloyds Broker Ratings & Price Targets (January 2026)

Source: Market Data

Consensus: Moderate Buy

Average Target: ~104p

Current Price: ~108p (late January 2026)

How Should Investors Position for Lloyds in 2026?

- Short Term: Capitalise on buyback-driven momentum and earnings strength

- Medium Term: Reinvest dividends to compound total returns

- Long Term: Track progress toward Lloyds becoming a “super-app” for UK financial services

Final Verdict: Is Lloyds a Buy, Hold, or Sell?

Investment Rating: BUY (Income, Stability & Re-rating Potential)

Lloyds Banking Group has decisively moved beyond its post-financial-crisis reputation. With record profits, rising dividends, aggressive buybacks, and a clear path to 16%+ RoTE, the bank is emerging as a core FTSE 100 income and recovery play.

While regulatory risks remain, Lloyds’ 13.2% CET1 capital ratio provides ample protection—making the risk-reward profile compelling at current levels.

Lloyds Investor FAQs – January 2026

When is the next Lloyds dividend paid?

The final dividend of 2.43p is expected in May 2026, subject to shareholder approval.

Why is Lloyds share price rising?

A combination of a 12% profit beat, dividend upgrade, and the launch of a £1.75bn buyback.

What are the key risks?

The FCA motor finance review and any sharp deterioration in the UK housing market.

Please wait processing your request...

Please wait processing your request...