NVIDIA is entering 2026 as the undisputed heavyweight champion of the "Intelligence Age," with a market valuation that has recently crossed the $5 trillion threshold. Despite a brief period of volatility in late 2025, the consensus among Wall Street’s "smart money"—including Jefferies, Bank of America, and J.P. Morgan—remains overwhelmingly bullish. The narrative has shifted from the initial "AI Gold Rush" (training) to the "AI Utility Era" (inference and agentic AI), where NVIDIA’s software ecosystem and new Rubin architecture are creating a competitive moat that rivals find increasingly difficult to bridge.

Key Drivers and Strategic Catalysts

The primary driver for NVIDIA in 2026 is the transition from "Experimental AI" to "Production-Grade Agentic AI." Leading global fund managers highlight that the industry is no longer just buying chips to train models; they are building "AI Factories."

NVIDIA’s Rubin platform, the successor to Blackwell, is now in full-scale production. It features the Vera CPU and Rubin GPU, integrated with HBM4 memory and 3.6 TB/s networking via NVLink 6. This "extreme co-design" approach allows enterprises to run reasoning-heavy models—which require up to 10x more inference compute than traditional chat models—at a significantly lower cost per token. Furthermore, the Stargate Project and massive cloud capex from Microsoft, Amazon, and Google (estimated to exceed $500 billion collectively in 2026) provide a solid floor for demand.

Source: Kalkine Group

Current Technical Analysis

Source: Trading View

NVIDIA’s stock recently tested major support levels following a pullback from its October 2025 highs of $212. Technicians observe that the stock is currently consolidating in a healthy "bull flag" pattern between $180 and $195. The Relative Strength Index (RSI) has cooled from overbought levels, currently sitting near 52, suggesting the stock has "worked off" its froth. Support remains firm at the 200-day moving average, while a decisive break above the $200 resistance level could trigger a momentum run toward the $250–$275 analyst targets. Volume profiles indicate significant institutional accumulation during dips, a classic sign of "smart money" positioning for the next leg up.

Latest Analyst Upgrades and Target Prices

Source: Kalkine Group

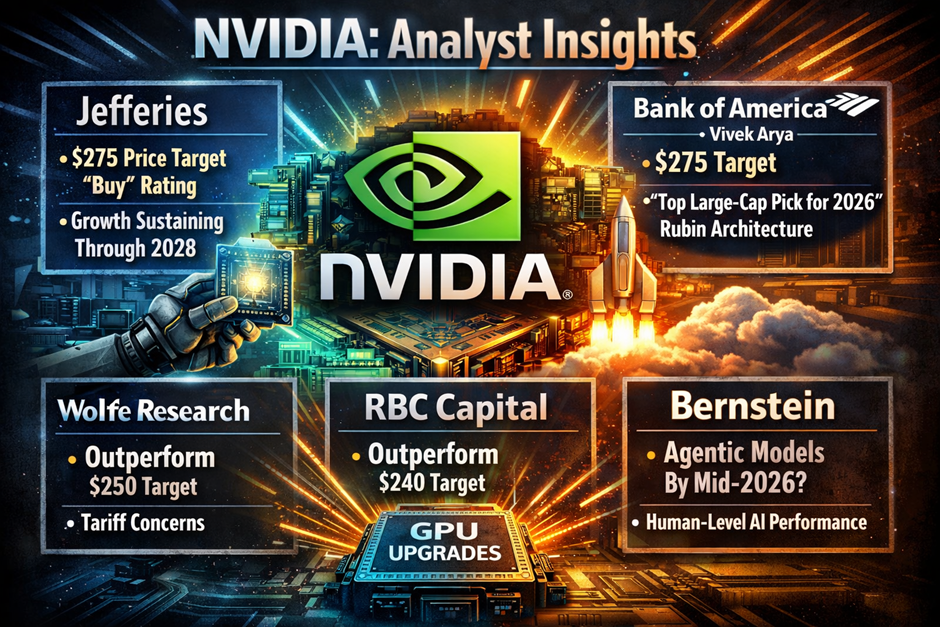

- Jefferies: Recently raised its price target to $275 (from $250), maintaining a "Buy" rating. They cite an updated accelerator build model that sees growth sustaining through 2028.

- Bank of America (Vivek Arya): Reaffirmed a $275 target, calling NVIDIA a "top large-cap pick for 2026" due to its technology moat and the ramp-up of the Rubin architecture.

- Wolfe Research: Reiterated an "Outperform" rating with a $250 price target, despite potential tariff headwinds.

- RBC Capital: Initiated coverage with an "Outperform" rating and a $240 target, highlighting sustained cloud capital expenditure.

- Bernstein: Analysts suggest that agentic models could reach human-level performance by mid-2026, driving another massive wave of GPU upgrades.

Latest Business Model and Operational Updates

NVIDIA has evolved from a hardware vendor into a full-stack "AI Operating System" provider. The latest business model emphasizes recurring revenue through the NVIDIA AI Enterprise software suite and specialized platforms like Omniverse (industrial AI) and DRIVE (autonomous vehicles).

Operational updates show a significant pivot in China; following the loss of approximately $8 billion in H20 chip revenue due to US export controls, NVIDIA is focusing on "Sovereign AI" projects in Japan, Europe, and India. The company also announced a landmark partnership with Siemens to build the world's first fully AI-driven, adaptive manufacturing sites, beginning with a blueprint factory in Germany.

Latest Financials, Valuation, and Dividends

NVIDIA's financial performance continues to defy gravity, though margins have seen a temporary "Blackwell ramp" dip.

- Revenue: Reported a record $57 billion in Q3 (up 62% YoY), with Data Centre revenue accounting for $51.2 billion.

- Gross Margins: Currently sitting at 73.6% (non-GAAP). Management expects a return to the 75% range by late 2026.

- Valuation: Despite the price surge, the forward P/E has compressed to roughly 25x–30x due to explosive earnings growth. The PEG ratio of 0.77 suggests the stock is still "cheap" relative to its growth profile.

- Shareholder Returns: NVIDIA returned $37 billion to shareholders in the first nine months of fiscal 2026. This includes a quarterly dividend of $0.01 per share and massive share buybacks, with over $62 billion still remaining in the current authorization.

Outlook and Risks for 2026

The outlook for 2026 is defined by "The Great Inference Ramp." As AI agents become mainstream in consumer apps and industrial robotics, the demand for real-time token generation is projected to grow tenfold. However, several risks loom on the horizon:

- Competition from Hyperscalers: Amazon (Trainium/Inferentia) and Alphabet (TPU v6) are increasingly using internal silicon to reduce costs, potentially capping NVIDIA's market share in the cloud.

- Supply Chain Concentration: Heavy reliance on TSMC and Samsung for HBM4 and advanced packaging remains a single point of failure.

- Geopolitical Friction: Ongoing trade wars and 25% tariffs on advanced semiconductors could squeeze hardware margins or disrupt global shipping.

- Execution Risk: Moving from Blackwell to Rubin in record time leaves little room for manufacturing errors or firmware bugs.

Conclusion

NVIDIA enters 2026 as the primary beneficiary of a structural shift in global computing. While competition from custom silicon (ASICs) and geopolitical hurdles are real, the company’s "extreme co-design" of chips, networking, and software provides a moat that many analysts believe is widening rather than shrinking. With a valuation that remains grounded by massive earnings growth and a product roadmap that is accelerating, NVIDIA remains the "North Star" for institutional and retail investors alike in the AI economy.

Please wait processing your request...

Please wait processing your request...