The commodities market is closing 2025 with a bang. On December 30, 2025, Phoenix Copper (LSE: PXC) emerged as a top performer on the London Stock Exchange’s AIM market, surging approximately 26% in a single session.

As the "green metal" supercycle intensifies, retail and institutional investors alike are scrambling to understand if this is a short-term spike or the beginning of a massive re-rating for the Idaho-focused producer.

The "Perfect Storm": Key Drivers Behind the Surge

Today's price action wasn't a fluke; it was the culmination of macro tailwinds and micro-milestones hitting the market simultaneously.

Source: Kalkine Group

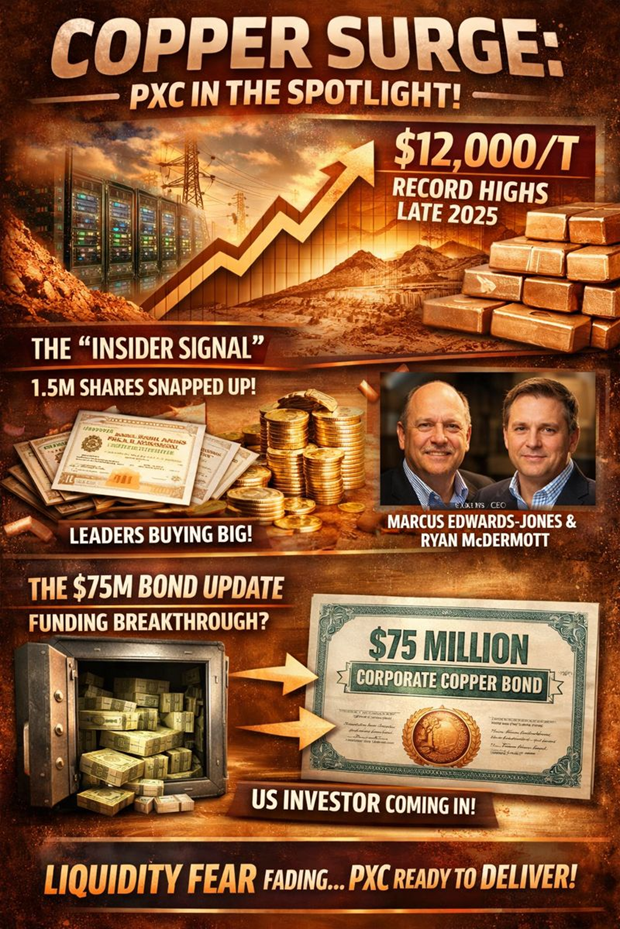

- Global Copper Deficit & Record Highs

Copper prices have shattered records in late 2025, testing the $12,000/tonne mark. With US Federal Reserve rate cuts easing financing costs and a massive surge in demand from AI data centers and electrification, "Doctor Copper" is signaling a supply crunch. PXC, as a US-based developer, is perfectly positioned to fill this gap.

- The "Insider Signal"

Confidence is contagious. Recent filings reveal significant Director and Advisory Board share purchases. Notably, Executive Chairman Marcus Edwards-Jones and CEO Ryan McDermott collectively snapped up over 1.5 million shares in mid-to-late December. When leadership puts their own capital on the line at these levels, the market listens.

- Funding Clarity: The $75M Bond Update

The primary drag on PXC has been the funding gap for the Empire Mine. Speculation today suggests a breakthrough in the $75 million corporate copper bond subscription. News of an accredited US investor moving toward definitive documentation has mitigated "liquidity fear," the #1 killer of AIM stocks.

Business Model & Operational Roadmap 2025/26

Phoenix Copper isn't just a "hope and pray" exploration outfit. Their business model has evolved into a dual-track production and exploration strategy.

The Flagship: Empire Open-Pit Mine

Located in Custer County, Idaho, the Empire Mine is a polymetallic powerhouse.

- Asset: 80% ownership of a skarn-hosted deposit.

- Reserves: 10.1 million tonnes (Proven & Probable) containing 109 million lbs of copper, 104,000 oz of gold, and 4.6 million oz of silver.

- The "Low-CapEx" Edge: PXC is utilizing a "crush-grind-flotation-tank leach" circuit designed to produce two pay streams: a copper/gold/silver concentrate and a cement copper stream.

Exploration Alpha: The "Deep" Potential

While the open pit provides the cash flow, the Empire Sulphide Vein System (located deep below the pit) and the Navarre Creek Gold Exploration project offer the "blue sky" potential that drives 10x returns.

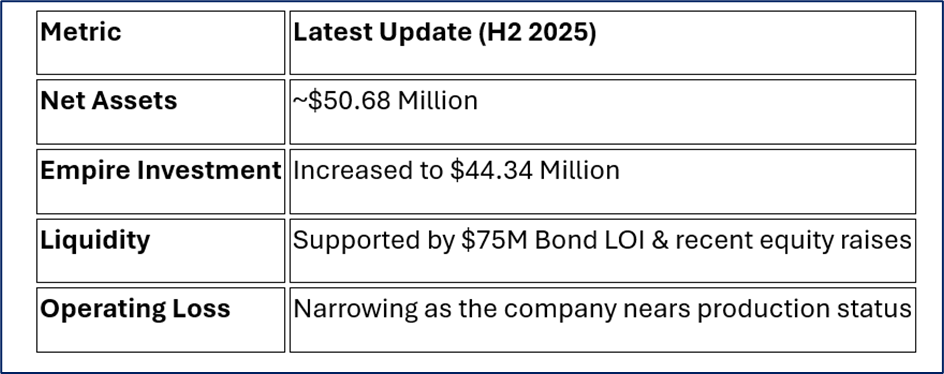

Latest Financial Health Check (As of Dec 2025)

Source: Company Data

Management has been disciplined, restructuring short-term loan facilities and extending maturities to June 2026, giving them the runway needed to reach the "first pour."

SWOT Analysis: The Honest Truth

Source: Kalkine Group

Strengths

- Tier-1 Jurisdiction: Operating in Idaho, USA, reduces geopolitical risk compared to African or South American mines.

- Polymetallic Credits: Gold and silver "by-products" significantly lower the net cash cost of copper production.

- ESG Rating: Holds an 'A' rating for responsible mining, crucial for modern institutional mandates.

Weaknesses

- Funding Dependency: Still reliant on the final drawdown of the $75M bond to reach full-scale construction.

- Micro-Cap Volatility: With a relatively small market cap, the stock is prone to wild swings on low volume.

Opportunities

- US Domestic Policy: 2025 executive orders aimed at slashing red tape for "critical minerals" (like copper) could accelerate permitting.

- AI Demand: The data centre buildout requires massive amounts of copper for power grids.

Threats

- Commodity Price Reversal: A sudden global recession could dampen copper demand.

- Technical Delays: Any metallurgical or engineering hiccups during the construction of the mill.

Critical Risks to Watch

Despite the 26% rally, PXC is not without peril. The company has historically faced a "cash runway" challenge, often resulting in small, dilutive equity raises to keep the lights on. Investors should also monitor the LME vs. COMEX premium, as trade policy arbitrage continues to distort physical metal flows.

The Verdict: Is the Phoenix Rising?

The 26% jump on December 30th reflects a market that is finally pricing in production certainty. By de-risking the $75M bond and riding the wave of record copper prices, Phoenix Copper has transformed from a speculative "penny stock" into a serious US domestic supplier.

With first production targets looming, the next 12 months will be the most transformative in the company’s history. Whether this rally holds depends entirely on one thing: turning Idaho dirt into London dollars.

Please wait processing your request...

Please wait processing your request...