Proteome Sciences (LSE: PRM) capped off 2025 with a definitive exclamation point, climbing approximately 10.8% on December 31, 2025.

For retail investors and biotech analysts, this wasn't just "end-of-year window dressing." It was the culmination of a pivotal year where the company successfully pivoted from a reagent-dependent model to a high-growth Contract Research Organization (CRO) powerhouse.

Key Drivers: What Ignited the Dec 31 Rally?

Source: Kalkine Group

The double-digit surge on the final trading day of the year was driven by three primary catalysts:

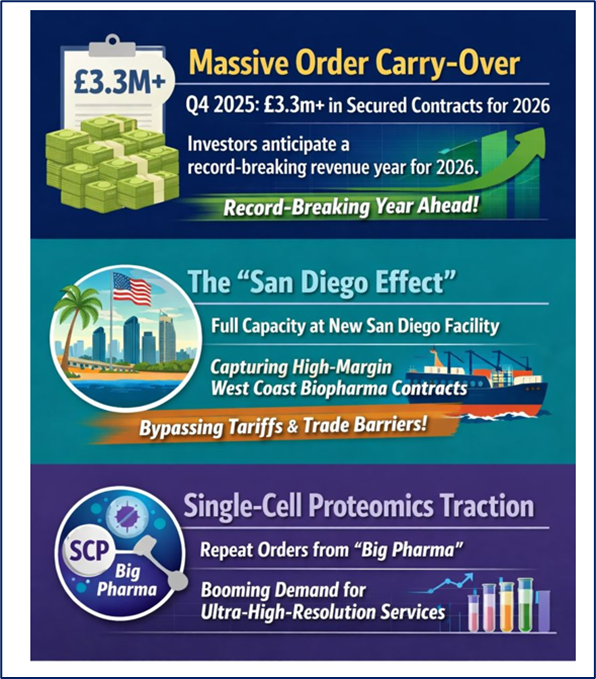

- Massive Order Carry-Over: Throughout Q4 2025, management signaled that the order book for 2026 was already exceeding £3.3m in secured contracts. Investors reacted to the realization that 2026 is mathematically positioned to be a record-breaking year for revenue.

- The "San Diego Effect": The newly operational San Diego facility reached full capacity in late 2025. This localized US presence bypassed international trade friction and tariffs, capturing high-margin "West Coast Biopharma" contracts that were previously out of reach.

- Single-Cell Proteomics (SCP) Traction: After securing its first commercial SCP contracts in late 2024 and early 2025, the market received confirmation of repeat orders from "Big Pharma" for these ultra-high-resolution services.

Latest Business Model: The "Hybrid High-Margin" Strategy

Proteome Sciences has evolved its business model to balance stability with explosive upside:

- Services-First (The Growth Engine): Moving away from just selling kits, PRM now operates as a specialized CRO. They provide end-to-end mass spectrometry services, including SysQuant® and TMT MS3, which are essential for clinical trial biomarker discovery.

- The Reagent Royalty Tail: While TMT (Tandem Mass Tags) reagent sales (distributed by Thermo Fisher) faced R&D budget headwinds in early 2025, the model now relies on the 35plex TMTpro™ tags, which offer the highest multiplexing capacity in the industry, ensuring long-term royalty streams.

- IP Licensing: The company is actively out-licensing its proprietary biomarker panels for stroke and oncology, moving toward a "discovery-as-a-service" model.

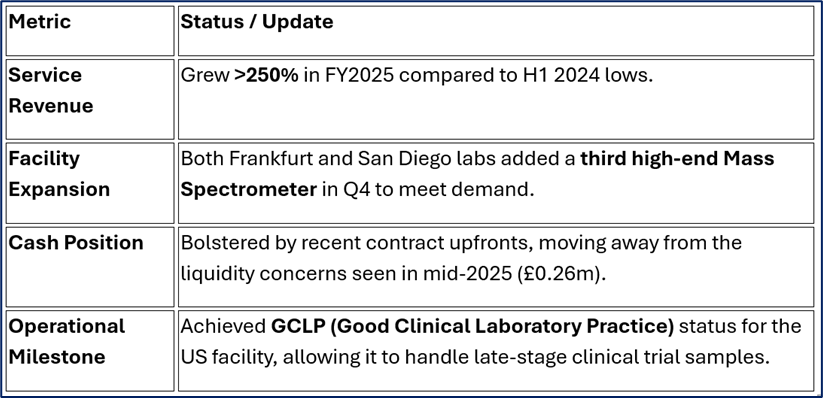

Financial & Operational Updates (Year-End 2025)

Source: Company Data

SWOT Analysis

Source: Kalkine Group

Strengths

- Monopoly on TMT: Holds the core patents for Tandem Mass Tags, the gold standard for protein quantification.

- Strategic Geography: Dual-hub operations in the EU (Frankfurt) and US (San Diego) insulate the company from regional economic shocks.

Weaknesses

- Liquidity & Spread: As an AIM-listed stock, PRM often suffers from wide bid-ask spreads (sometimes up to 60%), leading to high volatility.

- Historical Debt: Previous reliance on shareholder loans for CAPEX.

Opportunities

- AI Integration: Proteomics is the next frontier for AI drug discovery (e.g., AlphaFold 3). PRM’s high-dimensional data is exactly what AI models need.

- Precision Medicine: As FDA approvals shift toward "personalized" drugs, the demand for PRM’s biomarker validation services is expected to scale.

Threats

- R&D Budget Cuts: Global shifts in NIH funding or US biopharma austerity can delay service contracts.

- Alternative Tech: Data-Independent Acquisition (DIA) methods are competing with TMT-based workflows.

The Risk Factor: What to Watch

Despite the 10.8% rally, Proteome Sciences remains a "high-beta" play. The primary risk in 2026 is execution lag. The company has the orders, but it must now process them without technical downtime. Additionally, any further "global turmoil" regarding tariffs could impact the cost of importing specialized reagents into their European hubs.

Conclusion

The 10.8% jump on December 31 reflects a market finally pricing in the structural shift from a struggling reagent seller to a vital, high-capacity CRO. With a multi-million-pound pipeline extending into 2027 and a strategic foothold in the US, Proteome Sciences enters 2026 with its strongest fundamental backdrop in a decade.

Please wait processing your request...

Please wait processing your request...