Saga PLC stock is one of the strongest-performing FTSE 250 travel stocks in 2026, as the UK travel recovery, cruise demand, and over-50s leisure spending accelerate. After delivering triple-digit gains over the past year, investors are increasingly asking: Is Saga a genuine FTSE 250 multibagger — or has the easy money already been made?

This in-depth Saga PLC stock outlook for January 2026 analyses share price performance, UK travel demand trends, macroeconomic and GBP impacts, analyst forecasts, valuation risks, and whether Saga shares are a buy, hold, or sell for short-, medium-, and long-term investors.

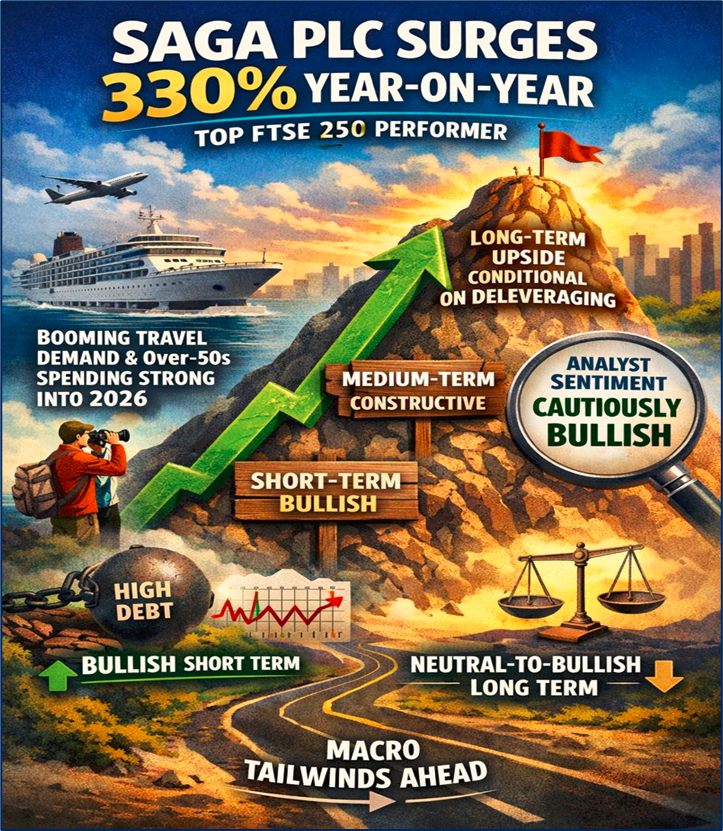

Key Takeaways – Saga PLC Stock Outlook (January 2026)

- Saga PLC stock is among the top-performing FTSE 250 shares, rising roughly 330% year-on-year, driven by travel recovery and restructuring progress

- UK travel demand, cruise bookings, and over-50s leisure spending remain structurally strong into 2026

- Analyst sentiment is cautiously bullish, though debt levels and earnings volatility remain core risks

- Short-term momentum is bullish, medium-term outlook constructive, long-term upside conditional on deleveraging

- Saga stock currently appears bullish short term and neutral-to-bullish long term, supported by macro tailwinds

Source: Kalkine Group

Is Saga PLC Stock Surging in January 2026 — and Why Are Investors Paying Attention?

Saga plc has emerged as one of the most searched FTSE 250 stocks in January 2026, attracting retail investors, recovery-focused funds, and UK value hunters.

The Saga share price has massively outperformed both the FTSE 250 and FTSE 100, supported by:

- Rebounding cruise and holiday demand

- Improved operational execution

- A shift toward a more focused, capital-light business model

As of 2 February 2026, Saga stock is trading around GBX 534, up approximately 2.7% on the day, reflecting continued bullish sentiment.

With investors rotating into UK domestic recovery stocks, travel and leisure shares, and undervalued mid-caps, Saga sits squarely at the intersection of several high-ranking investment themes dominating Google and financial media search trends.

How Do Global Markets and the UK Economy Affect Saga Stock in 2026?

Global equity markets entering 2026 are shaped by:

- Cooling inflation

- Expectations of interest-rate peaks

- Selective “risk-on” sentiment

These dynamics have supported mid-cap stocks and cyclical sectors, particularly travel, leisure, and consumer services.

In the UK specifically:

- Consumer confidence has stabilised

- Services inflation is easing

- Real wage growth is gradually recovering

Saga’s focus on financially resilient over-50s consumers positions the company well relative to discretionary travel peers more exposed to younger, debt-sensitive demographics.

What Role Does GBP and the FTSE 250 Play in Saga’s Share Price?

The GBP outlook remains a key variable for UK travel stocks in 2026. A relatively soft but stable pound:

- Supports domestic and inbound tourism

- Does not materially inflate Saga’s cost base

From a market-structure perspective:

- The FTSE 100 is dominated by global exporters and defensives

- The FTSE 250 is more sensitive to UK growth and services demand

Saga’s FTSE 250 listing makes it a direct beneficiary of renewed global interest in undervalued UK mid-cap equities.

What Is Saga’s Business Model — and Why Does It Matter Now?

Saga operates a diversified travel and insurance services model focused on the over-50s demographic, a segment benefiting from long-term UK demographic tailwinds.

Core business pillars include:

- Ocean and river cruises

- Package holidays and escorted tours

- Insurance broking and financial services partnerships

In recent years, Saga has:

- Exited capital-intensive underwriting

- Simplified operations

- Focused on higher-margin, lower-risk income streams

This strategic shift has improved earnings visibility and resilience, a key reason behind the stock’s re-rating.

What Do the Latest Financial and Operational Updates Show?

Recent updates underline several bullish themes:

- Strong cruise booking volumes and improving load factors

- Travel division profitability exceeding expectations

- Tight cost discipline and operational efficiency

- Clear focus on cash generation and balance-sheet repair

While Saga’s historical earnings have been volatile, earnings quality is improving, and markets are increasingly pricing in a more sustainable recovery.

How Does Saga Compare With Other UK Travel and FTSE Stocks?

Saga’s hybrid structure makes peer comparison nuanced.

Relative positioning:

- Higher volatility than large insurers like Aviva

- More differentiated customer base than mass-market travel firms

- Greater recovery leverage than defensive FTSE 100 stocks

Saga stands out due to brand loyalty, demographic focus, and integrated offerings, though leverage remains higher than some peers.

Is Saga Stock Bullish or Bearish in the Short Term?

Short-Term Outlook (3–6 months): Bullish Bias

Supporting factors:

- Strong technical momentum

- Robust travel demand through peak booking cycles

- FTSE 250 rotation into recovery and value stocks

Risks to watch: profit-taking, GBP volatility, macro headlines.

What Is the Medium-Term Outlook for Saga Shares?

Medium-Term Outlook (6–18 months): Constructive but Selective

Performance will depend on:

- Sustaining travel demand beyond peak cycles

- Continued debt reduction

- Margin stability in insurance broking

Successful execution could drive further valuation re-rating.

Is Saga a Long-Term Investment or a Trading Opportunity?

Long-Term Outlook (18+ months): Neutral-to-Bullish (Conditional)

Long-term upside improves if Saga delivers:

- Consistent free cash flow

- Balance-sheet deleveraging

- Stable earnings across cycles

Without these, Saga remains more of a high-beta recovery stock than a defensive compounder.

What Are Analysts Saying About Saga PLC Stock in 2026?

Analyst sentiment remains cautiously optimistic:

- Majority ratings lean toward Buy or Outperform

- Target prices remain wide due to uncertainty

- Travel recovery cited as the primary upside catalyst

Saga is widely viewed as a recovery and turnaround play, not a low-risk income stock.

Key Risks Investors Must Consider

- Elevated debt and refinancing sensitivity

- Earnings volatility tied to travel cycles

- UK economic slowdown risks

- Fuel and cost inflation exposure

- Regulatory and consumer-protection changes

These risks explain why Saga still trades at a discount to more stable peers.

FAQ – Saga PLC Stock

Is Saga PLC stock a buy in 2026?

Saga looks attractive for short-term momentum and recovery investors; long-term investors should remain selective.

Why has Saga’s share price risen so sharply?

Travel demand recovery, restructuring progress, and renewed FTSE 250 interest.

Does Saga pay a dividend?

Saga currently prioritises balance-sheet strength over dividends.

Is Saga a travel stock or an insurance stock?

Saga is best viewed as a hybrid consumer services company, with travel as the main earnings driver.

Final Investment Conclusion: Buy, Hold or Sell?

Saga PLC presents a compelling but asymmetric investment opportunity in 2026.

The stock is bullish in the short term, supported by momentum, travel recovery, and FTSE 250 rotation. Long-term upside depends on disciplined execution and debt reduction.

For investors seeking UK recovery exposure, travel sector upside, and turnaround potential, Saga warrants close monitoring. Conservative, income-focused investors should approach with risk management in mind.

Please wait processing your request...

Please wait processing your request...