Why activist pressure, margin recovery, and healthcare tailwinds could make Smith & Nephew one of 2026’s most compelling recovery plays

Key Takeaways (January 2026)

- Share Price Trend: Smith & Nephew (SN.) trades near 1,240p, rebounding from 52-week lows and showing renewed upside momentum.

- Primary Catalyst: The newly launched RISE strategy (Reach, Innovate, Scale, Execute) alongside the Integrity Orthopaedics acquisition is reshaping growth expectations.

- Activist Involvement: Cevian Capital now owns ~5%, pushing hard for efficiency and >20% trading margins by 2028.

- 2026 Financial Outlook: Management guides for ~6% underlying revenue growth and Free Cash Flow of ~$800m.

- Dividend Appeal: A dependable yield of 2.3%–3.0%, increasingly attractive as interest rates decline.

Why Is Smith & Nephew Attracting Investor Attention in 2026?

Looking for the best FTSE 100 recovery stocks to buy now? Smith & Nephew has rapidly moved back into the spotlight as one of the UK market’s most credible turnaround stories.

After years of operational underperformance, the global medical-technology leader is entering 2026 with a reset strategy, activist oversight, and improving macro conditions. With the UK economy stabilising and the Bank of England expected to cut interest rates, defensive healthcare stocks with reliable cash flows are back in favour.

What makes SN. different is that this is not just a defensive play. The stock trades at a deep valuation discount to US peers despite owning high-quality franchises in Orthopaedics, Sports Medicine, and Advanced Wound Care. If execution improves even modestly, the upside could be significant.

Global and UK Market Forces Shaping the Outlook

Global MedTech Industry Trends

The global orthopaedics market is expected to exceed $70 billion in 2026, growing at roughly 6% CAGR. Demand is driven by:

- An ageing population

- A rebound in elective surgeries

- Innovation in robot-assisted and smart implant systems

Smith & Nephew’s CORI Surgical System directly targets this high-growth segment.

Key challenge: Input costs and supply-chain inefficiencies — though these pressures have eased meaningfully since 2024.

UK Economy & FTSE 100 Context

- UK GDP Growth (2026E): ~1.2%–1.4% (slow but stable)

- FTSE 100: Recently tested the 10,000 level, reflecting renewed global investor confidence

- GBP/USD: Stable around $1.30, reducing FX volatility for SN.’s dollar-heavy revenue base

Investor rotation away from speculative growth and toward quality value sectors like Healthcare is a major tailwind.

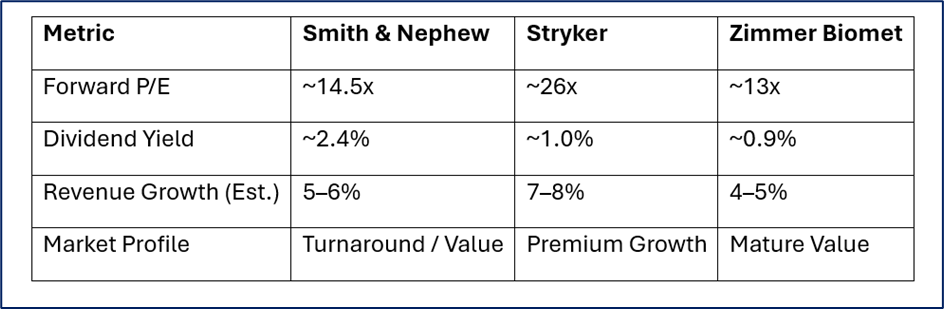

Peer Comparison: Valuation Gap Tells the Story

Source: Market Data

Takeaway: If SN. executes on margins and re-rates even halfway toward US peer multiples, shareholders could see meaningful multiple expansion.

Smith & Nephew Share Price Outlook

Short Term (3–6 Months): Neutral → Constructive

- Range-bound between 1,200p–1,300p

- Market awaits FY2025 results (March 2, 2026) for proof that RISE is delivering

Medium Term (6–12 Months): Bullish

- Cost savings begin flowing through earnings

- Rate cuts boost demand for dividend-paying healthcare stocks

- Activist oversight limits downside risk

Long Term (1–3 Years): Very Bullish

- Margin recovery to 20%+ could unlock a full valuation re-rating

- Orthopaedic procedure backlog provides multi-year demand visibility

- Takeover optionality remains if valuation stays depressed

Investor Playbook: How to Position in 2026

- Short-Term Traders: Buy weakness near 1,200p with tight risk controls around earnings.

- Income Investors: Dividend reinvestment (DRIP) while yields remain above inflation.

- Long-Term Value Investors: Accumulate patiently — this is a margin-led turnaround, not a hype trade.

Bull, Bear, and Base Case

Bull Case

- RISE strategy restores operational discipline

- Sports Medicine innovation accelerates growth

- Activist pressure forces sustained margin improvement

Bear Case

- Execution disappoints (again)

- China pricing pressure resurfaces

- Stock revisits ~1,000p if targets slip

Base Case

- Expectations are low

- “Good” results drive outsized upside

- Risk/reward remains asymmetrically favourable

Latest Business & Strategic Updates

- RISE Strategy (Dec 2025): Clear focus on growth markets, faster innovation, and margin discipline.

- Integrity Orthopaedics Acquisition (Jan 2026): Strengthens high-margin Sports Medicine portfolio.

- Cash Flow Strength: ~$800m FCF supports M&A, dividends, and buybacks.

- Inventory Clean-Up: One-off $200m provision clears the deck for future profitability.

Analyst Sentiment (January 2026)

- Consensus: Hold leaning Buy

- Price Targets:

- Barclays: 1,280p

- Jefferies: 1,450p

- RBC Capital: 1,500p

- Berenberg: 1,250p

Valuation Reality: A return to historical averages implies 25%+ upside.

Key Risks to Watch

- Delays to margin targets

- Renewed China VBP pricing pressure

- Misinterpretation of GLP-1 drug impact on joint replacement demand

Final Verdict: Buy, Sell, or Hold?

Verdict: BUY (for patient investors)

Smith & Nephew is no longer a falling knife. It is a credible turnaround backed by activist capital, improving cash flow, and a clear operational roadmap. Downside risk is cushioned by dividends and free cash flow, while upside is driven by margin recovery and valuation re-rating.

Action Point: Watch the March 2, 2026 earnings release closely. Confirmation of margin progress could mark the start of the next leg higher.

Please wait processing your request...

Please wait processing your request...