The primary driver behind today's price action is the strategic strengthening of the Board, announced this morning. GoldStone has appointed Richard Kofi Amegashie and Michael Jones as Independent Non-Executive Directors.

Source: Kalkine Group

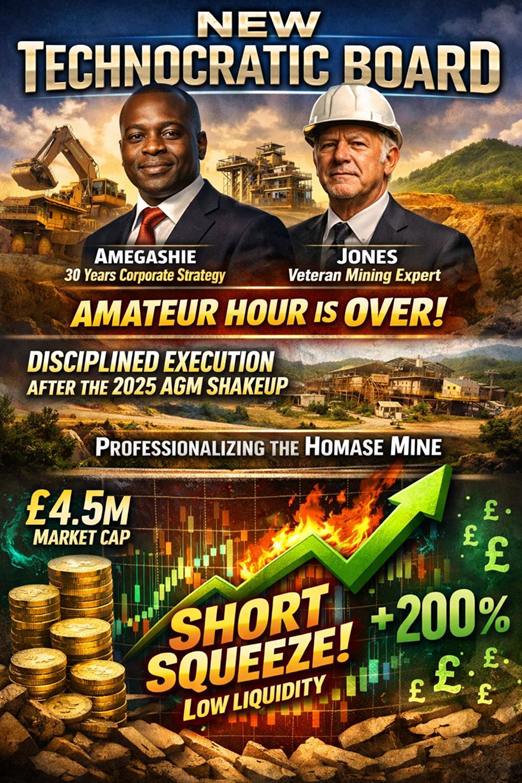

- Institutional Credibility: The addition of Amegashie (30 years of international corporate strategy) and Jones (a veteran mining engineer and capital markets expert) signals to investors that the "amateur hour" is over.

- Operational Reassurance: The market is reacting to the promise of "disciplined execution." After the turbulence of the 2025 AGM—where former Chair Angela List was ousted—this new "Technocratic Board" is seen as a move toward professionalizing the Homase Mine's ramp-up.

- Short Squeeze/Low Liquidity: With a market cap hovering around £4.5m–£5m, even modest buy-side volume can cause double-digit percentage moves.

Business Model: The 2025 Pivot

GoldStone has transitioned from a pure exploration play into a Junior Producer.

- Asset Core: The Akrokeri-Homase Gold Project (AKHM) in Ghana, situated in the world-class Ashanti Gold Belt (near AngloGold Ashanti’s 70Moz Obuasi Mine).

- Revenue Stream: Utilizing Heap Leach processing, which allows for lower CAPEX and faster processing of oxide ores.

- Growth Strategy: Using cash flow from the current Homase open pit to fund the exploration of the high-grade Akrokeri Underground Mine, which historically produced gold at a staggering 24 g/t.

Latest Updates: Financial & Operational

Operations (Homase Mine)

- Production Velocity: The company recently reported steady pours, including a notable 355.6 oz pour in September 2025.

- Throughput Target: Focus remains on delivering 48,000 tonnes per month of agglomerated ore to the heap leach pads.

- Infrastructure: Significant upgrades to the heap leach facilities were completed in H2 2025, funded entirely via internal cash flow.

Financials (H1 2025 Results)

- Revenue Surge: Revenue climbed to $6.7M (up from $2.6M in H1 2024).

- Gross Profit: Exploded by over 200% year-on-year, driven by high gold prices and optimized stacking.

- Balance Sheet: While still carrying ~$8.2M in borrowings, the successful conversion of the Gold Loan interest into shares has eased immediate liquidity pressure.

SWOT Analysis

Source: Kalkine Group

The Risk Factors

Investing in AIM-listed junior miners is not for the faint of heart.

- Funding Gaps: The company noted at the AGM that it may need further share issuance authorities to secure long-term funding.

- Management Stability: The fallout from the 2025 AGM and the investigation into "disclosed confidential information" by a former chairman suggests lingering internal friction.

- Environmental/Regulatory: Ghana is tightening environmental scrutiny on heap leach operations, which could increase compliance costs.

Conclusion: A Turnaround in Progress?

Today’s 16% rally is a vote of confidence in the New Board. While the financials show a company still grappling with debt, the 200% jump in gross profit proves that the underlying engine—the Homase Mine—is capable of generating serious cash in a high-gold-price environment.

If the new directors can streamline operations and clean up the balance sheet without further massive dilution, GoldStone could be one of the most significant "deep value" recoveries on the AIM market going into 2026.

Source: Trading View, 22 December 2025, 12:15 PM GMT

Please wait processing your request...

Please wait processing your request...