J Sainsbury plc (LSE: SBRY) kicked off the 2026 trading year on a high note, with its stock climbing approximately 1% to reach 328p during the first full session of the year on January 2, 2026.

While the broader FTSE 100 showed modest gains, Sainsbury’s outperformed many of its retail peers, signaling a "festive hangover" that was surprisingly upbeat for investors.

The Jan 2 Catalyst: Why the Stock Moved

Source: Kalkine Group

The primary driver for the ~1% uptick was a mix of market positioning and technical momentum following the Christmas trading period.

- Positive Festive Read-throughs: Early industry data suggested that UK grocers experienced a record-breaking Christmas. Sainsbury’s, specifically, benefitted from its "Next Level" strategy, which emphasized premium Taste the Difference ranges—a high-margin winner during the holidays.

- Share Buyback Support: On January 2, the company confirmed ongoing transactions in own shares. This consistent buyback program (part of a commitment to return over £800m to shareholders in FY25/26) provided a "floor" for the share price by reducing supply.

- Total Voting Rights Update: A regulatory announcement regarding total voting rights on Jan 2 reminded the market of the stabilized capital structure following the phased withdrawal from Financial Services.

Latest Business Model: "Food First" & Beyond

Sainsbury’s has evolved from a traditional grocer into a streamlined, multi-brand retail ecosystem. Its 2026 model rests on three pillars:

- Grocery Dominance: The "Food First" initiative has been superseded by the "Next Level Sainsbury’s" strategy. The focus is now on volume growth—selling more physical items rather than just relying on inflation to boost revenue.

- Argos Integration: Argos has been transformed into a digital-first retailer housed largely within Sainsbury’s supermarkets. This "store-in-store" model reduces overheads while driving footfall.

- Financial Services Exit: By Jan 2, 2026, Sainsbury’s had significantly progressed its exit from core banking, moving toward a "distributed" model where third parties provide the products, allowing Sainsbury’s to focus on retail margins.

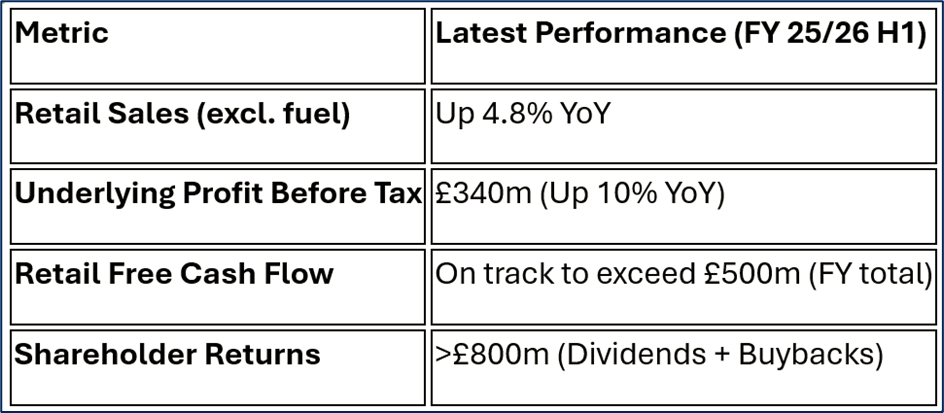

Financial & Operational Health Check

Source: Company Data

Operational Highlights:

- Nectar Power: The Nectar loyalty program now uses AI-driven "Your Nectar Prices," which has been a critical tool in fighting off discounters like Aldi.

- Cost Savings: The company is currently halfway through its ambitious £1 billion cost-saving target by 2027, achieved through warehouse automation and AI-led inventory management.

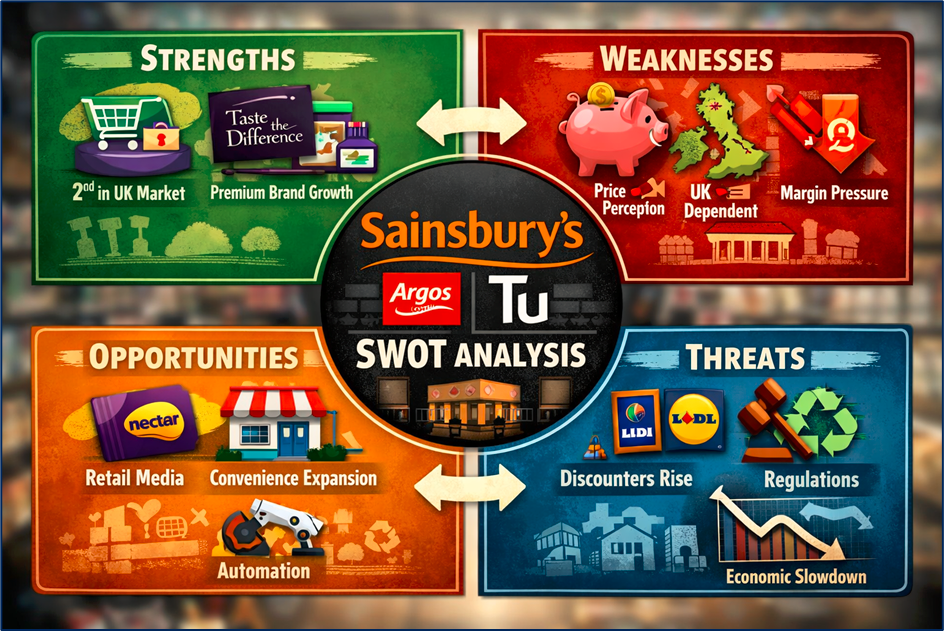

SWOT Analysis (2026 Outlook)

Source: Kalkine Group

Strengths

- Brand Equity: Ranked 2nd in UK grocery market share.

- Premium Positioning: "Taste the Difference" is the fastest-growing premium own-label brand.

- Omnichannel Strength: Seamless integration between Sainsbury's, Argos, and Tu clothing.

Weaknesses

- Price Perception: Still viewed as more expensive than Aldi/Lidl, despite the "Aldi Price Match."

- Geographic Limitation: Almost entirely dependent on the UK economy; no international hedge.

- Margin Pressure: High labor costs and business rates continue to squeeze the bottom line.

Opportunities

- Retail Media: Using Nectar data to sell advertising space to brands, creating a high-margin revenue stream.

- Convenience Expansion: Opening 25+ new convenience stores to capture "top-up" shoppers.

- Automation: Full rollout of machine-learning forecasting to reduce food waste.

Threats

- Aggressive Discounters: Aldi and Lidl continue to expand their UK footprint.

- Regulatory Hurdles: Potential for stricter labor laws or environmental packaging taxes.

- Consumer Shift: If the UK economy slows in mid-2026, shoppers may trade down to cheaper rivals.

Key Risks to Watch

Investors should remain aware of operational execution risks. The integration of 14 newly acquired supermarket sites is a major capital expenditure. Additionally, while the exit from banking is positive for long-term focus, the restructuring costs (estimated at £72m post-tax) can create "noise" in the statutory profit figures.

Conclusion

Sainsbury’s performance on January 2, 2026, reflects a company that has successfully "stuck to its knitting." By focusing on food quality and aggressive cost-cutting, it has managed to stay relevant in a brutal retail landscape. The stock’s 1% rise isn't just a daily fluke; it’s a nod to a business model that is finally delivering both volume growth and shareholder returns.

Please wait processing your request...

Please wait processing your request...