The final trading week of 2025 is starting with a bang for real estate investors. On December 29, 2025, Land Securities Group PLC (LSE: LAND) surged by over 7% (significantly outperforming the broader FTSE 100), reaching price levels near GBX 623.

While the "Santa Rally" is lifting some boats, Landsec’s move is powered by a fundamental shift in its business model and a series of high-conviction "insider buys" that have retail investors paying close attention.

The December 29 Catalyst: Why the Spike?

The 7% jump isn't just holiday spirit. Several specific drivers are coalescing:

Source: Kalkine Group

- Massive Insider Confidence: Just before the Christmas break, Non-Executive Director Anne Richards acquired shares worth nearly £100,000. This follows a pattern of insider buying throughout December, signaling to the market that those with the best view of the books see the stock as undervalued.

- Yield Stabilization: As we head into 2026, UK gilt yields have stabilized. For a REIT (Real Estate Investment Trust) like Landsec, lower volatility in interest rates makes their 6.5% dividend yield look incredibly attractive compared to cash.

- Portfolio Revaluation Optimism: Markets are front-running the 2026 recovery. With Landsec's retail portfolio (like Bluewater and Liverpool ONE) showing 5% rental growth, investors are betting that the "valuation floor" has finally been hit.

Latest Business Model: The "Fewer, Bigger, Better" Pivot

Landsec has shed its skin as a traditional "office landlord." The 2025 business model is built on three aggressive pillars:

- Retail Destinations: Moving away from high-street shops to "Mega-Malls." They recently invested £610m into Liverpool ONE and Bluewater, targeting an accretive 7.7% income yield.

- Central London Growth: Focusing exclusively on "Green" high-spec offices. They are disposing of £2bn in older assets to fund a £1bn development pipeline in the West End.

- The Residential Pivot: Landsec is building a £2bn residential platform, transforming underused urban space into 9,000+ homes to create a "recession-proof" income stream.

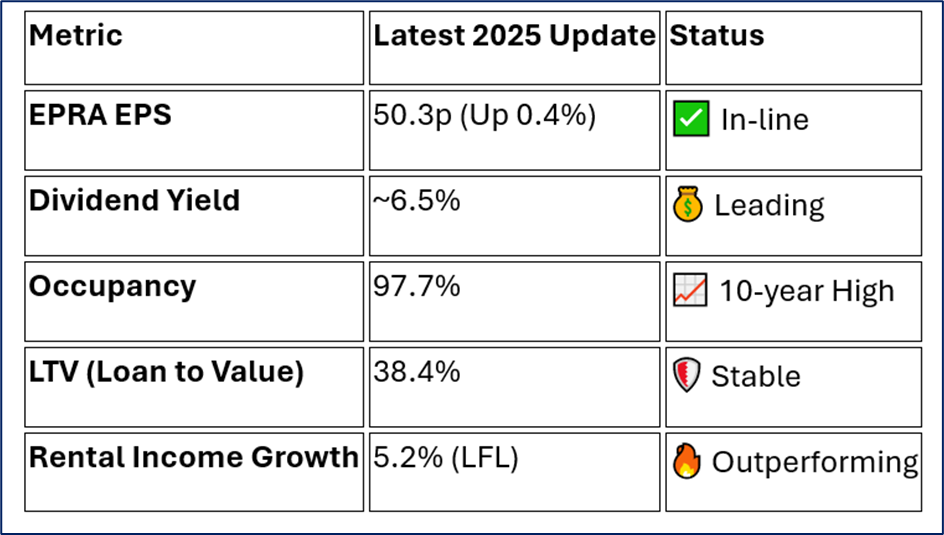

2025 Financial & Operational Snapshot

Source: Company Data

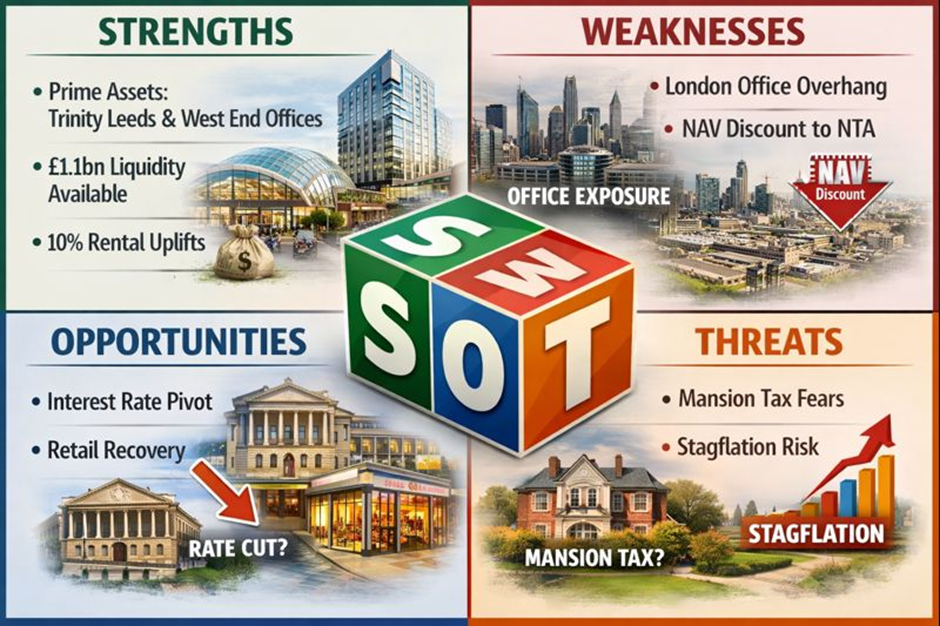

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Prime Asset Base: Ownership of "trophy" assets like Trinity Leeds and West End offices that retain value even in downturns.

- Liquidity: £1.1bn in cash and undrawn facilities; no major debt refinancing needed until 2027.

- Pricing Power: 10% rental uplifts on new leases show they can pass inflation costs to tenants.

Weaknesses

- Office Overhang: While they are selling, a significant portion of the portfolio is still tied to London offices, which face long-term "work from home" headwinds.

- Net Asset Value (NAV) Discount: The stock still trades at a significant discount to its 863p NTA (Net Tangible Assets), though this is closing.

Opportunities

- Interest Rate Pivot: If the Bank of England cuts rates further in Q1 2026, REITs are the primary beneficiaries.

- Retail Recovery: The "flight to physical" retail is accelerating as online costs (shipping/returns) rise for brands.

Threats

- Mansion Tax / Budget Fears: Rumors of a "mansion tax" on properties over £2m (from April 2028) could dampen the luxury residential outlook.

- Economic Stagflation: Sticky inflation could force the BoE to keep rates "higher for longer" than the market expects.

Key Risks for Retail Investors

- Capital Recycling Execution: Landsec is trying to sell £2bn of offices. If they can't find buyers at book value, the NAV will take a hit.

- Consumer Spending: Their retail success depends on the UK consumer. If 2026 brings a recession, footfall at Bluewater could drop.

- Refinancing Cliff: While safe until 2027, the cost of debt in two years will likely be higher than the expiring low-interest bonds.

Conclusion

Landsec's performance on December 29 is a classic "value unlock" signal. The company has successfully pivoted from a stagnant office giant to a dynamic operator of "best-in-class" destinations. With 97.7% occupancy and a upgraded earnings guidance for 2030, the market is finally beginning to price in the transformation.

Please wait processing your request...

Please wait processing your request...