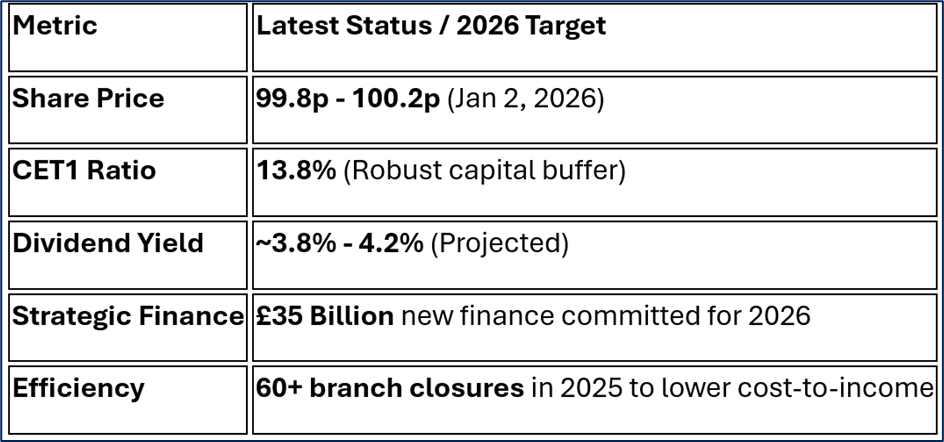

On January 2, 2026, Lloyds Banking Group (LSE: LLOY) joined a wider FTSE 100 rally, with its shares climbing approximately 1% to break the psychological £1 (GBX 100) barrier.

This milestone represents a significant recovery for the UK's largest mortgage lender, reaching price levels not seen since before the 2008 financial crisis.

- Key Reasons & Drivers for the Jan 2 Surge

Source: Kalkine Group

- The FTSE 10,000 Milestone: Lloyds’ 1% gain was part of a broader "New Year relief rally" that saw the FTSE 100 hit an all-time high of 10,000 points. Sentiment was buoyed by easing inflation and a stable UK economic outlook.

- Buyback Momentum: The bank recently completed a £1.7bn share buyback (Dec 2025), reducing the share count by over 2.2 billion. Investors are now anticipating a fresh buyback announcement alongside the upcoming 2025 preliminary results.

- Rate Cut Resilience: While the Bank of England cut rates to 3.75% in late 2025, Lloyds has managed its "structural hedge" effectively, protecting its Net Interest Margin (NIM) more successfully than analysts initially feared.

- Housing Market Optimism: Forecasts of a 4% rise in house prices for 2026 have invigorated Lloyds, which holds a 20% share of the UK mortgage market.

- Latest Business Model: "Helping Britain Prosper" 2.0

Lloyds has transitioned from a traditional "high street bank" into a digitally-led financial services group.

- Mass Affluent Focus: Launch of Lloyds Premier, targeting individuals with over £100,000 in assets, shifting the model toward higher-margin wealth management.

- Digital Ecosystem: Over 22 million active digital users. The bank is no longer just lending; it is a data-driven platform using AI to automate 60% of lending decisions.

- Income Diversification: Moving away from pure interest income by growing "capital-light" fees in insurance (Scottish Widows) and commercial banking.

- Financial & Operational Updates (2025-2026)

Source: Company Data

- SWOT Analysis (2026 Context)

Source: Kalkine Group

Strengths

- Mortgage Dominance: Unrivaled 20% market share via Lloyds, Halifax, and Bank of Scotland.

- Low-Cost Funding: A massive £496bn deposit base provides cheap capital.

- Digital Scale: Largest digital bank in the UK, reducing operational overhead.

Weaknesses

- UK Concentration: Almost 100% of revenue is UK-based; no geographic hedge against a domestic slowdown.

- Legacy Systems: High ongoing costs to decommission old IT infrastructure (though 10% was retired in 2025).

- Sensitivity to Rates: Profits remain highly correlated to BoE base rate fluctuations.

Opportunities

- AI Monetization: Expected to generate £150m in incremental value by the end of 2026 via its AI Centre of Excellence.

- SME Growth: A dedicated £9.5bn fund for SMEs in 2026 to capture the business recovery.

- Housing Stimulus: Potential government planning reforms could trigger a surge in first-time buyer volumes.

Threats

- Motor Finance Probe: The FCA’s final rules on motor finance redress (due early 2026) remain a "dark cloud" despite a £1.95bn provision.

- Fintech Cannibalization: Neo-banks like Monzo and Revolut are aggressively targeting the "Mass Affluent" segment Lloyds wants.

- Regulatory Squeeze: Potential for higher "windfall" taxes if bank profits remain at record levels.

- Key Risks to Watch

- Macro-Stagflation: If UK growth stays below 1.4% while inflation proves "sticky," credit impairments (bad loans) could rise from their current record lows of 0.18%.

- Valuation Ceiling: At a P/E ratio of ~12.8x, Lloyds is no longer "cheap" compared to its 10-year average of 9.7x. Much of the good news may already be priced in.

- Operational Resilience: Transitioning to cloud-based banking carries inherent cyber-security and migration risks.

Conclusion

The 1% rise on Jan 2, 2026, is a victory for Lloyds’ "Black Horse" strategy. Breaking the 100p mark validates the bank's aggressive share buybacks and digital pivot. While it remains a "defensive" play with a solid dividend, its growth in 2026 will depend entirely on whether the UK housing market can sustain its recovery and if the motor finance investigation concludes without further multi-billion pound hits to the balance sheet.

Please wait processing your request...

Please wait processing your request...