Greenland for Sale? Trump’s Shock Ultimatum Sends London Stocks into a Tailspin; Gold Rockets to Record Highs

The FTSE 100 suffered its steepest one-day decline in months on Tuesday, January 20, 2026, as a "perfect storm" of geopolitical brinkmanship and cooling domestic data battered investor sentiment. The blue-chip index tumbled 1.02% (down 104 points) to trade near 10,091, wiping out a significant chunk of its early January gains.

While the "Santa Rally" of 2025 pushed the index toward the historic 10,000 mark, today’s volatility highlights the fragile nature of the 2026 outlook. From a sudden trade war over Greenland to a weakening UK jobs market, here is the full breakdown of why the "Smart Money" is shifting to safe havens.

1. The Macro Drivers: Why the FTSE 100 Slid Today

The primary catalyst was a shock escalation in trade rhetoric from U.S. President Donald Trump. In a move that caught global diplomats off-guard, the White House threatened a 10% additional tariff on imports from European nations—including the UK—unless the U.S. is permitted to purchase Greenland.

- Trade War 2.0: Markets are pricing in the risk of retaliatory tariffs from the EU (estimated at €93 billion), threatening the profit margins of UK-based multinationals.

- Cooling UK Labor Market: Domestic data released this morning showed unemployment remaining at a four-year high of 5.1%, while wage growth slowed to 4.7%. This signals a cooling economy, yet the Bank of England (BoE) appears hesitant to cut rates further in February, leaving businesses squeezed by high borrowing costs.

- AstraZeneca Delisting Jitters: A specific weight on the index came from pharmaceutical giant AstraZeneca, which saw shares drop over 2.5% following news it would delist its ADRs and debt from the Nasdaq, fueling concerns about capital liquidity.

2. Sector Spotlight: The Winners and Losers

Source: Kalkine Group

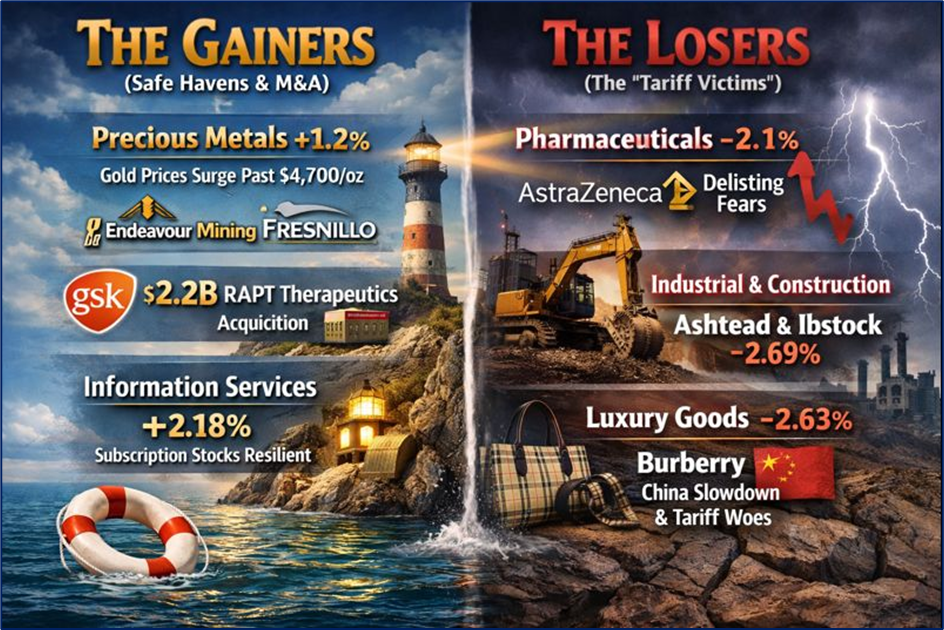

The Gainers (Safe Havens & M&A)

Despite the sea of red, a few sectors managed to stay afloat, primarily driven by a flight to safety and opportunistic deals.

- Precious Metals (+1.2%): Gold miners like Endeavour Mining and Fresnillo surged as Gold prices vaulted past $4,700/oz.

- Healthcare (M&A): GSK made headlines with a $2.2 billion acquisition of RAPT Therapeutics, providing some defensive support to the biotech space.

- Information Services: Informa (+2.18%) led the gainers list as investors rotated into stocks with resilient, subscription-based revenue models.

The Losers (The "Tariff Victims")

- Pharmaceuticals (-2.1%): Led by AstraZeneca, the sector felt the heat of both delisting news and general risk-off sentiment.

- Industrial & Construction: Ashtead (-2.69%) and Ibstock fell sharply on fears that trade tensions will stall global infrastructure spending.

- Luxury Goods: Burberry (-2.63%) remains under pressure as weak domestic demand in China—confirmed by recent retail data—clashes with potential U.S. tariff hikes.

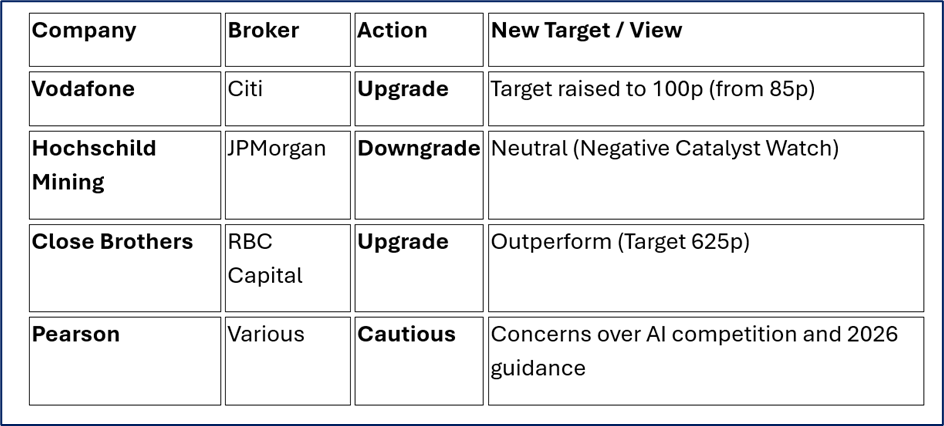

3. Analyst Upgrades & Downgrades

Source: Market Data

4. Technical Analysis Summary

Source: Trading View

The FTSE 100 has been trading within a rising channel since April 2025.

- Resistance: The recent record high of 10,250 remains a major psychological and technical ceiling.

- Support: Immediate support sits at 10,000. Analysts warn that a sustained break below 9,930 would negate the current uptrend and could trigger a slide toward the 9,625 level.

- RSI: The Relative Strength Index has pulled back from "Overbought" territory (above 70), suggesting today's move was a necessary, albeit painful, "breather" for the market.

5. The "Smart Money" View: What the Banks are Saying

- J.P. Morgan: Remains positive on 2026 global equities but cites a 35% probability of a recession this year, urging investors to focus on "front-loaded fiscal stimulus" opportunities.

- Amundi: Views the current dip as "precautionary profit-taking" rather than a fundamental collapse, suggesting the macroeconomic backdrop of decelerating inflation still favors risk assets in the medium term.

- BlackRock: Reports indicate "Smart Money" is increasing exposure to UK mid-caps (FTSE 250) over the blue-chips, betting that BoE rate cuts later in 2026 will benefit domestically-focused firms more than tariff-exposed multinationals.

Conclusion: A Buying Opportunity or the Start of a Slump?

Today’s -1.02% drop is a stark reminder that while the FTSE 100 looks strong on paper, it remains "hypersensitive" to geopolitical shocks. The "Greenland Tariff" may be a temporary negotiation tactic, but it has injected a dose of reality into a market that was perhaps too optimistic about a smooth 2026.

For the retail investor, the message is clear: Volatility is back. While the 10,000-point milestone is still within reach for Q1, the path there is now paved with trade-war landmines and labor market uncertainty.

Please wait processing your request...

Please wait processing your request...