Why the Stock Popped ~1% on Christmas Eve 2025

Melrose Industries (LSE: MRO) closed up approximately 1% on December 24, 2025. While a 1% move on a half-trading day might seem like "noise," in the context of Melrose’s late-2025 trajectory, it signals high-conviction accumulation.

The move wasn't driven by a single explosive headline, but rather a "Perfect Storm" of three compounding factors:

Source: Kalkine Group

- The "Santa Buyback" Support: Melrose has been aggressively executing its buyback program throughout December (as confirmed by daily "Transaction in Own Shares" filings). On low-volume days like Christmas Eve, this persistent buying pressure creates a natural floor and upward drift.

- Aerospace Supercycle Validation: Investors are positioning ahead of the Q1 2026 reporting season. With GE Aerospace and Rolls-Royce signalling strong 2025 finishes, Melrose—a key Risk & Revenue Sharing Partner (RRSP)—is being bid up as a "read-across" play. The market is effectively pricing in a "beat" on the back of higher-than-expected engine flying hours.

- Defensive Rotation: As geopolitical uncertainty lingered into year-end 2025, capital rotated into "hard" defence and aerospace assets. Melrose’s GKN Aerospace division, with its deep entrenchment in both civil and defence supply chains, is seen as a safe haven.

Latest Business Model: The "Pure Play" Powerhouse

Gone are the days of the "Buy, Improve, Sell" conglomerate. By late 2025, Melrose has successfully completed its transformation into a pure-play aerospace giant (GKN Aerospace).

- Core Identity: A Tier 1 supplier to almost every major aircraft and engine platform (Airbus, Boeing, Lockheed Martin, GE, Rolls-Royce).

- The "Engine" of Profit: The Engines Division is the crown jewel, accounting for >70% of profits. It operates on a "Razor and Blade" model:

- Razor (OE): Building engine structures (often at low margin).

- Blade (Aftermarket): The RRSPs (Risk & Revenue Sharing Partnerships). Melrose gets a cut of the revenue every time an engine is repaired or flown. With global fleets aging and flying more in 2025, this is a cash-printing machine.

- Structures Division: Once a drag, now a stabilized asset focusing on higher-margin defence contracts and composite wing technologies, approaching its target of ~9-10% margins.

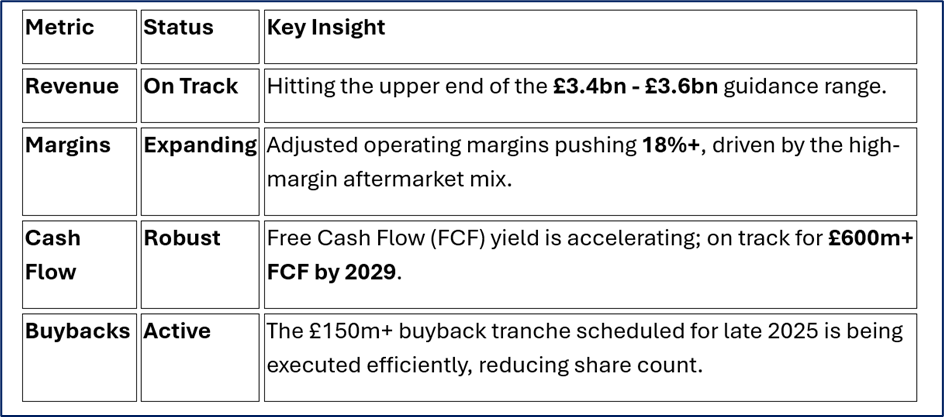

Operational & Financial Pulse (Late 2025 Update)

The market's confidence stems from the tangible delivery of the "2025 Commitments":

Source: Company Data

Critical Update: The Structures restructuring program is effectively complete as of Dec 2025. The heavy cash restructuring costs are ending, meaning 2026 is set to be the first year of "clean" cash conversion.

SWOT Analysis (Executive Summary)

Source: Kalkine Group

Strengths (The Moat)

- RRSP Cash Cow: 17 of 19 major engine partnerships are in the "cash generation" phase. These contracts last 30+ years and are incredibly sticky.

- Aftermarket Exposure: ~70% of profits come from flight hours/repairs, insulating Melrose from new aircraft delivery delays (e.g., Boeing production issues).

- Technology Leadership: GKN is a leader in additive manufacturing (3D printing) for engines and lightweight composites.

Weaknesses (The Internal Drag)

- Supply Chain Complexity: Managing thousands of suppliers for the Structures division remains operationally heavy compared to the leaner Engines division.

- FX Sensitivity: Heavy exposure to USD revenue vs. GBP reporting means currency fluctuations (like a strengthening Pound) can mask underlying growth.

Opportunities (The Upside)

- Defence Spending: Global re-armament is driving demand for GKN’s military airframe components (F-35, 6th gen fighters).

- "Fix and Keep": Now that they aren't selling businesses, they can compound returns internally.

- M&A Potential: GKN Aerospace itself becomes an attractive acquisition target for a US defence prime.

Threats (The Risks)

- Titanium Scarcity: Continued supply chain bottlenecks for raw titanium affecting production rates.

- Tariffs: Any new UK/US or EU/US trade friction could impact the seamless movement of aerospace parts.

- Geopolitics: Disruptions to air travel (closing airspaces) directly reduce "flying hours," hurting the high-margin RRSP revenue.

Key Risks to Watch in 2026

- The "Boeing" Factor: If OEM build rates (737 MAX or 787) stall again, Melrose’s Structures division suffers, even if Engines are fine.

- Labor Inflation: Aerospace engineering wages are skyrocketing. Can Melrose pass these costs on to customers with fixed-price contracts?

- Execution Risk: The transition from "Turnaround Specialist" to "Long-term Operator" requires a different management skillset. Investors are watching for any strategic drift.

Conclusion: A "Compounder" in the Making?

Melrose’s 1% rise on December 24, 2025, is a microcosm of its broader story: Quiet Accumulation. The market is waking up to the fact that Melrose is no longer a chaotic collection of businesses, but a focused, cash-generative aerospace proxy trading at a discount to its US peers (like GE Aerospace or TransDigm).

With the "heavy lifting" of restructuring finished in 2025, the story for 2026 is simple: Cash Flow Conversion. If they deliver the promised cash returns, that 1% rise is just the start.

Please wait processing your request...

Please wait processing your request...