1. Executive Summary: Why is the Stock Up ~3%?

On 7 January 2026, Dowlais Group's share price rise of approximately 3% is primarily driven by the mechanics of its pending takeover by American Axle & Manufacturing (AAM).

Unlike a fixed-cash buyout, the agreed £1.16bn deal is structured as a mix of cash and new AAM shares. Consequently, Dowlais’ stock has become a derivative of American Axle’s performance. If AAM shares rise in pre-market or US trading, the implied value of the offer for Dowlais shareholders increases immediately, forcing the London listing to re-rate upwards to close the arbitrage gap.

Secondary drivers include:

- Increased Deal Certainty: Recent filings (Form 8.3s) indicate institutional positioning and progress toward final regulatory clearances (the "scheme of arrangement").

- Strategic Streamlining: The market is reacting positively to the finalized disposal of GKN Hydrogen, which eliminates a cash-burning unit and improves the group's immediate earnings profile.

2. Key Drivers & Market Movers

A. The "Cash + Stock" Deal Correlation

The takeover offer grants Dowlais shareholders 0.0863 new AAM shares + 42p in cash per share.

- The Driver: As of Jan 7, 2026, positive sentiment surrounding US automotive stocks or a specific uptick in AAM’s valuation directly lifts the "implied value" of the Dowlais bid. The 3% rise suggests AAM stock is strengthening, or the GBP/USD exchange rate is moving in favor of the deal value.

B. Removal of the "Hydrogen Drag"

Dowlais recently completed the sale of GKN Hydrogen to Langley Holdings.

- Why it matters: While the hydrogen technology was promising, it was loss-making (£9m operating loss in prior years) and capital-intensive. Exiting this venture allows the company to present a cleaner, higher-margin profile (pure-play Automotive & Metallurgy) to its future owners, removing a key concern for risk-averse investors.

C. "Bargain Basement" Valuations

Despite the premium offered by AAM, analysts have noted that the exit valuation (approx. 4.1x EV/EBITDA) is historically low.

- The Catalyst: Some investors may be buying in anticipation that shareholder pushback could force a sweetened offer, or simply because the spread between the current price and the deal price offers a "safe" annualized return if the deal closes on schedule in Q1/Q2 2026.

3. Latest Business Model (Post-Hydrogen)

Dowlais has effectively returned to its core competencies, operating as a specialized automotive engineering giant.

- GKN Automotive (The Core):

- Driveline: Global leader in sideshafts and propshafts (50% market share).

- ePowertrain: Designing eDrive systems for Electric Vehicles (EVs). The strategy is "propulsion agnostic"—supplying parts for ICE, Hybrids, and EVs alike.

- GKN Powder Metallurgy:

- Producing precision sintered metal components and magnets for EV motors.

- Strategic Shift: This unit is now positioned as a vertical integration asset for the combined AAM-Dowlais entity.

- Divested: GKN Hydrogen (Sold to focus capital on the automotive transition).

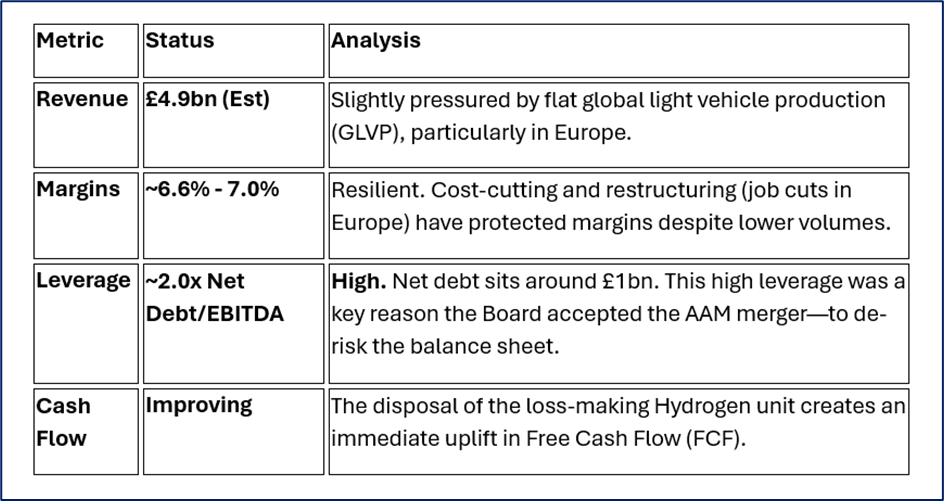

4. Financial & Operational Health Check (Jan 2026 Context)

Source: Company Data

5. SWOT Analysis

Source: Kalkine Group

Strengths (Internal):

Dowlais holds an unrivaled market dominance in driveshafts—it is the "category king" with deep relationships with nearly every major global OEM (Volkswagen, Ford, GM). Its technology moat in eDrive systems is substantial, and the recent restructuring has made the operational base leaner.

Weaknesses (Internal):

The company is burdened by high debt in a high-interest-rate environment, restricting its ability to invest aggressively in R&D without external help (hence the merger). It also suffers from low margins compared to software-defined auto players, characteristic of legacy Tier 1 suppliers.

Opportunities (External):

The merger with American Axle is the massive opportunity. It promises $300m in cost synergies, creating a trans-Atlantic giant capable of weathering the EV transition. Furthermore, the hybrid vehicle resurgence plays perfectly into Dowlais' hands, as hybrids require complex drivelines (more content per vehicle than pure EVs).

Threats (External):

Regulatory Intervention remains the biggest immediate threat; antitrust authorities in the EU or China could delay the AAM deal. Long-term, a faster-than-expected EV slowdown or aggressive Chinese competition in the supply chain could erode their pricing power.

6. Risks to the Long Thesis

- Deal Breakage Risk: If the AAM takeover collapses (due to regulator blocking or shareholder revolt), Dowlais shares could plummet back to pre-bid levels (approx. 60p-70p), as the standalone debt load would worry the market.

- Exchange Rate Volatility: As the deal includes a cash component and US-listed shares, significant fluctuations in GBP/USD can erode the real value of the return for UK investors.

- Automotive Cycle Downturn: 2026 is forecast to be a "flat" year for auto production. Any recessionary dip in global car sales will hit Dowlais’ volumes immediately.

7. Conclusion

The ~3% rise on 7 January 2026 is a technical move driven by the arbitrage mathematics of the American Axle takeover bid. Investors are re-pricing Dowlais stock to match the rising value of the AAM shares offered in the deal. Fundamentally, the company has strengthened its hand by selling its loss-making Hydrogen business, making it a cleaner asset for the merger. While the "easy money" has been made since the initial bid announcement, today's move reflects growing market confidence that the deal will close and that the combined entity holds value.

Please wait processing your request...

Please wait processing your request...