While most of the City was checking out for the holidays, Metro Bank (LSE: MTRO) caught a festive bid on December 24, 2025, closing up approximately 1.51% at GBX 121.

This isn't just a holiday fluke. After a tumultuous few years, the "challenger" that almost folded is transforming into a lean, specialist lending machine. Here is the analytical deep dive into why Metro Bank is suddenly the FTSE 250’s favorite comeback story.

The Christmas Eve Catalysts: Why the Spike?

The 1.5% climb on December 24 was fueled by a "perfect storm" of regulatory relief and internal confidence:

Source: Kalkine Group

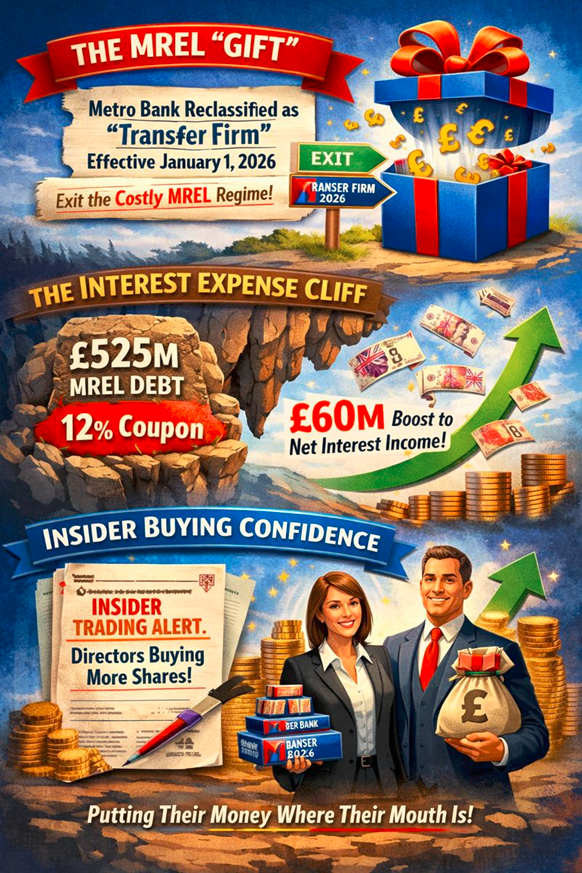

- The MREL "Gift": On December 19, the Prudential Regulation Authority (PRA) confirmed Metro Bank would be reclassified as a "Transfer Firm" effective January 1, 2026. This allows them to exit the costly MREL (Minimum Requirement for Own Funds and Eligible Liabilities) regime.

- The Interest Expense Cliff : Metro currently pays a staggering 12% coupon on £525 million of MREL debt. By exiting this regime, analysts expect a massive uplift in Return on Tangible Equity (RoTE)— potentially adding £60m to net interest income (NII) annually.

- Insider Buying Confidence: Regulatory filings on Dec 24 showed further Director/PDMR shareholding activity, signaling to retail investors that leadership is literally putting their money where their mouth is.

The 2025 Business Model: From "Dogs & Free Pens" to Specialist Powerhouse

The "Old" Metro Bank focused on expensive rapid branch expansion and generic retail lending. The 2025 Pivot is far more surgical:

- Asset Rotation: Shifting away from low-yield residential mortgages into high-margin specialist lending (SME, Commercial, and Specialist Mortgages).

- The Store Strategy: No longer just "banks," the 76 stores are now optimized as SME Hubs. Metro remains the only UK high street bank with 7-day-a-week opening, using this to maintain the lowest cost of deposits in the sector (approx. 95bps–102bps).

- Efficiency First: A brutal £80m annual cost-reduction plan is now fully baked into the 2025 financials, creating a "positive jaws" effect (income growing faster than expenses).

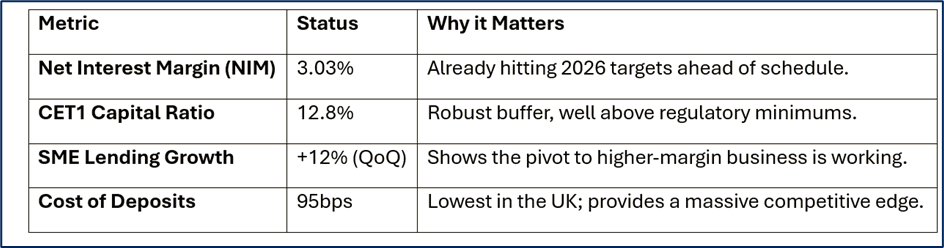

Latest Financial & Operational Pulse (Q3/Q4 2025)

Source: Company Data

SWOT Analysis

Source: Kalkine Group

Strengths

- Funding Edge: Phenomenal ability to attract low-cost deposits through its "service-led" branch model.

- Operational Momentum: Consistently meeting or beating guidance for the last four quarters.

- Niche Positioning: Dominates the SME "in-person" service gap left by Barclays and Lloyds.

Weaknesses

- Scale: Still a minnow compared to the "Big Four," making it vulnerable to price wars.

- Legacy Brand Scars: The 2019 accounting error and 2023 rescue deal still weigh on some institutional sentiment.

- Technology Lag: Heavy reliance on physical stores is expensive compared to digital-only neobanks like Monzo.

Opportunities

- Rate Environment: Higher-for-longer rates benefit banks with low-cost deposit bases like Metro.

- MREL Redemption: If they call their 12% debt early in 2026, earnings could skyrocket.

- M&A Target: At a 0.7x–0.8x price-to-book ratio, they remain a "cheap" acquisition target for a mid-tier player.

Threats

- UK Macro Squeeze: Any spike in SME defaults due to a cooling UK economy would hit their new core portfolio.

- Regulatory Scrutiny: The PRA remains "once bitten, twice shy" regarding Metro’s reporting.

- CRE Exposure: Commercial Real Estate remains a sensitive area for mid-sized lenders.

The Risk Radar

Investing in a turnaround is never a "sure thing." The primary risks for 2026 include:

- Execution Risk: The bank is targeting a mid-teens RoTE by 2027. This is an ambitious "hockey stick" recovery.

- Refinancing Friction: While MREL relief is coming, the transition and potential early redemption fees could cause short-term capital volatility.

- Liquidity Attrition: As customers seek higher yields elsewhere, maintaining that "lowest cost of deposits" title will become harder.

The Bottom Line

Metro Bank is no longer the "broken bank" of 2023. The 1.5% move on December 24 reflects a market finally pricing in a structurally more profitable business. By shedding expensive debt and doubling down on SMEs, Metro has positioned itself as a high-beta play on the UK’s mid-cap recovery.

Please wait processing your request...

Please wait processing your request...