As the UK retail sector navigates a complex "K-shaped" economic recovery in 2026, institutional sentiment has shifted toward "quality compounders" with international scalability. Global fund managers from BlackRock to Schroders, alongside investment banks like Deutsche Bank and Morgan Stanley, are prioritizing retailers that demonstrate "differentiation" and "technological resilience" over pure discounters.

The following analysis focuses on three FTSE-listed retail giants positioned for wealth compounding through 2026, characterized by high free cash flow and aggressive international expansion.

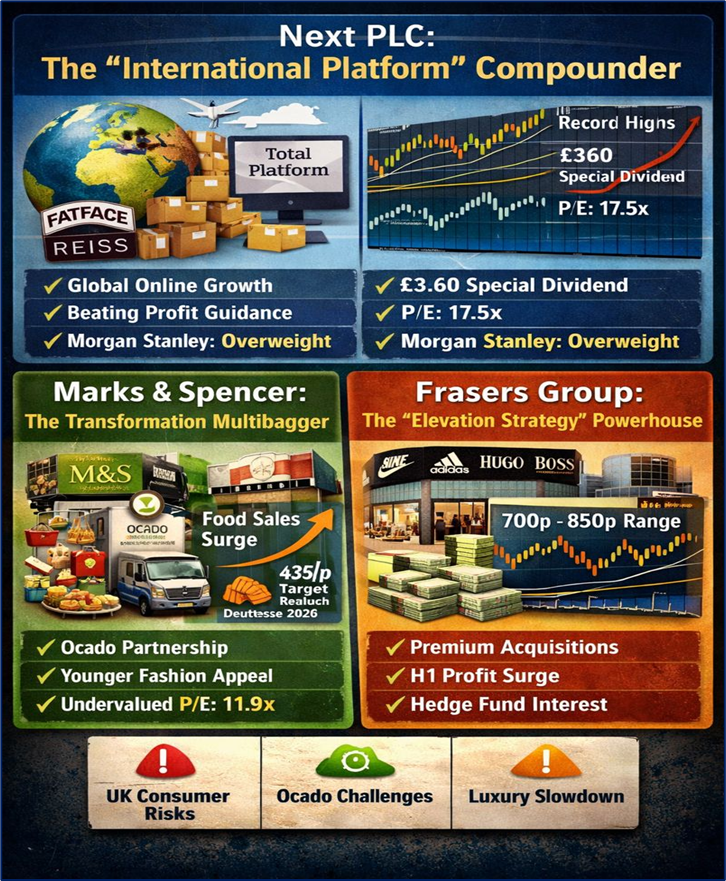

Source: Kalkine Group

Next PLC (NXT): The "International Platform" Compounder

Key Reasons and Drivers

Next has successfully transitioned from a traditional UK high-street retailer into a global "Total Platform" operator. Its primary driver is the exponential growth of its international online segment and its ability to act as a third-party logistics and digital provider for other brands (FatFace, Reiss, etc.). Analysts at AJ Bell and Deutsche Bank highlight its consistent ability to beat profit guidance, having raised estimates five times in the 2025/26 financial year alone.

Current Technical Analysis

Next is currently trading at record highs, recently crossing the £140 per share mark. The stock is characterized by a strong uptrend, supported by a 50-day moving average that has remained comfortably above the 200-day average throughout late 2025. While the Relative Strength Index (RSI) occasionally touches overbought territory (above 70), pullbacks have historically been shallow, finding strong support at psychological levels.

Financial and Operational Updates

- Latest Business Model: A hybrid of direct retail and "Total Platform" services. Over 38% of international sales are now online, reducing physical footprint risk.

- Latest Dividend: Next announced a £3.60 special dividend via a B-share scheme in January 2026, alongside a standard yield of approximately 2-3%.

- Valuation: Currently trades at a P/E multiple of approximately 17.5x 2026 earnings. While historically high for Next, analysts argue this reflects its "tech-lite" growth profile.

- Outlook: Guidance for FY 2026/27 projects a 4.5% rise in pre-tax profit to £1.20 billion, focusing on market share gains in Europe and the Middle East.

Risks and Institutional View

- Risks: UK consumer spending fatigue and "tough comparatives" from a stellar 2025.

- Smart Money View: Morgan Stanley remains "Overweight," citing Next as the most defensive growth play in the FTSE 100 due to its superior capital allocation.

Marks and Spencer Group (MKS): The Transformation Multibagger

Key Reasons and Drivers

M&S has undergone a radical "Reshaping for Growth" program. The primary wealth-compounding driver is its Food division, which has consistently outperformed the wider market for over 37 consecutive months. The integration with Ocado Retail is finally showing a pathway to profitability, while the "Fashion, Home & Beauty" segment has seen a major style perception shift, attracting a younger demographic.

Latest Financial and Operational Updates

- Business Model: Focused on "trusted value" and store rotation, replacing aging department stores with high-efficiency food-led sites.

- Latest Dividend: The interim dividend was hiked by 20% in late 2025, reflecting a robust balance sheet with net debt reduced to £1.8 billion.

- Valuation: Forward P/E stands at 11.9x, which is considered undervalued by Interactive Investor compared to its historical growth trajectory and peers like Tesco.

- Technical Paragraph: The stock has recovered strongly from a mid-2025 cyber-incident dip. It is currently testing resistance at the 400p level. Institutional accumulation (Smart Money) is evident in the rising "On-Balance Volume" (OBV) indicator.

Outlook and Risks

- Outlook: 2026 is the year of the "Sparks Loyalty" relaunch, intended to use AI for hyper-personalized offers to drive frequency.

- Risks: Execution risk in the Ocado JV and potential "fashiontainment" competition from global players like Gap or Amazon.

- Analyst Upgrades: Deutsche Bank recently upgraded its price target to 435p, citing "strong grocery momentum."

Frasers Group (FRAS): The "Elevation Strategy" Powerhouse

Key Reasons and Drivers

Under CEO Michael Murray, Frasers is executing an "Elevation Strategy"—moving away from "pile 'em high" sports retail toward premium partnerships with Nike, Adidas, and Hugo Boss. Its aggressive acquisition strategy (XXL ASA, Braehead Shopping Centre) and strategic stakes in luxury brands make it a unique retail-conglomerate play for 2026.

Business Model and Financials

- Business Model: An ecosystem of sports, premium lifestyle, and financial services (Frasers Plus).

- Latest Valuation: Trading at a discount to its net asset value per share of £5.32. Jefferies maintains a Buy rating with an 1,100p price target.

- Financial Update: Reported a 97% jump in pre-tax profit to £412.1 million in H1 2026, though this was aided by fair value gains on investments like Hugo Boss.

- Technical Paragraph: The stock is currently in a consolidation phase between 700p and 850p. Technical analysts look for a breakout above the 200-day moving average to signal a long-term trend reversal toward previous highs.

Risks and Conclusion

- Risks: Exposure to the "aspirational" luxury segment, which is currently "subdued." High net debt due to recent acquisitions (£1.03 billion).

- Institutional View: Hedge Funds have been attracted to Frasers' "deep value" metrics and aggressive share buybacks (£200m planned for 2026).

Please wait processing your request...

Please wait processing your request...