The London Stock Exchange has seen its share of volatility this year, but Kenmare Resources (LSE: KMR) is stealing the spotlight as we close out 2025. On December 30, the stock jumped approximately 12%, leaving retail investors and analysts scrambling to unpack the move.

Is this a "Santa Rally" or a fundamental shift in the mineral sands giant's narrative? Here is the deep-dive breakdown of the latest business model, financial updates, and the forces driving this double-digit breakout.

The Catalyst: Why the 12% Surge Today?

While Kenmare has faced a challenging 2025—including a $100 million non-cash impairment earlier this year—the late-December rally appears driven by three converging factors:

Source: Kalkine Group

- Project Milestone at WCP A: A major operational update released in mid-December confirmed that the Wet Concentrator Plant (WCP) A upgrade and its transition to the high-grade Nataka ore zone are progressing ahead of revised Q4 targets. This project is the "crown jewel" that unlocks 70% of Moma’s mineral resources.

- M&A Speculation Re-ignited: Following the rejection of a takeover bid earlier in the year (which the board claimed "undervalued the business"), fresh rumors of a revised offer from a strategic consortium have begun circulating in the city.

- Ilmenite Price Stabilization: After a weak 2024 and early 2025, market data indicates that titanium feedstock prices are stabilizing, coupled with a "buy the dip" sentiment as KMR was trading near 52-week lows in mid-December.

The Latest Business Model: Efficiency Over Volume

Kenmare operates the Moma Titanium Minerals Mine in Mozambique, one of the world's largest deposits. Their business model has shifted from pure extraction to "High-Margin Life Extension."

- Product Mix: They produce Ilmenite and Rutile (used for whiteness in paints, plastics, and paper) and Zircon (used in ceramics).

- The "Nataka" Pivot: The business is moving its largest plant (WCP A) to the Nataka zone. This isn't just a move; it's a decades-long life extension for the mine, ensuring production through 2045.

- Vertical Logistics: Kenmare owns its own jetty and transshipment vessels, allowing them to control the supply chain from the mine site directly to global customers, insulating them from some third-party port risks.

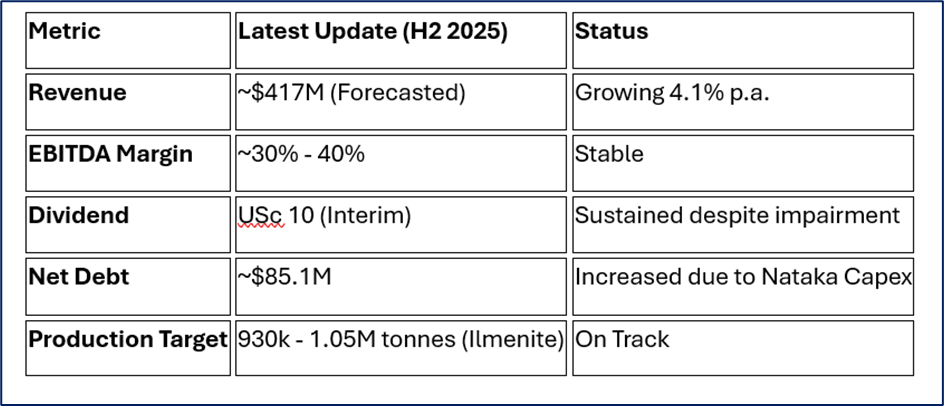

2025 Financial & Operational Snapshot

Source: Company Data

Operational Highlights:

- Selective Mining Operation (SMO): Commissioned in 2025, this small-scale, low-cost dredge allows for mining in peripheral areas, adding 50,000 tonnes of Heavy Mineral Concentrate (HMC) annually.

- ESG Leadership: Kenmare has successfully reduced Scope 1 and 2 emissions by over 12% against their 2021 baseline, a key metric for institutional "Green" funds.

SWOT Analysis (2025 Context)

Source: Kalkine Group

Strengths

- Low Cost: One of the lowest-cost producers globally due to dredge mining and dedicated power lines.

- Longevity: 100+ years of mine life at Moma ensures long-term cash flow potential.

- Market Share: Accounts for ~6-8% of global titanium feedstock supply.

Weaknesses

- Geographical Risk: 100% of production is concentrated in Mozambique.

- Debt Load: Capex for the Nataka transition has pushed net debt higher compared to 2023 levels.

- Technical Volatility: Recent $100M impairment highlights sensitivity to long-term price assumptions.

Opportunities

- M&A Target: Trading at a significant discount to book value (P/B ~0.3x) makes it a prime acquisition target.

- Titanium Metal Demand: Growing use in aerospace and high-tech manufacturing provides a secondary growth engine.

- Implementation Agreement: A successful license extension/renewal could lead to a massive stock re-rating.

Threats

- Political Instability: Regional security concerns in Mozambique remain a perennial "discount factor."

- Currency Fluctuations: Revenues in USD but costs in multiple currencies create hedging complexities.

- Substitute Products: Advancements in synthetic titanium could threaten long-term feedstock demand.

Key Risks to Watch

Investors shouldn't ignore the "Mozambique Discount." While the Moma mine is far from the conflict-prone northern Cabo Delgado region, political risk remains the primary reason for Kenmare's historically low P/E ratio. Additionally, the $341 million capital budget for the Nataka transition leaves little room for operational errors or delays.

Conclusion

Kenmare Resources is finishing 2025 with a "bang," fueled by operational progress and a market that finally seems to realize how undervalued the company's assets are. While the 12% jump is impressive, the stock remains a "show me" story—investors will be looking for the final Nataka commissioning in 2026 to prove that the dividend remains bulletproof.

Please wait processing your request...

Please wait processing your request...