The 7.71% surge in XP Power (LSE: XPP) shares on January 23, 2026, signals a definitive shift in market sentiment, marking the stock as a compelling "turnaround play" for early 2026. After a volatile 2024-2025 dominated by semiconductor cyclicality and debt concerns, investors are rushing back in following a pivotal Full Year Trading Update released just days prior.

The jump isn't just noise; it reflects a "sigh of relief" rally as the company confirmed it has successfully navigated its liquidity crunch, completed a major manufacturing transition to Malaysia, and is seeing order books swell once again. With the semiconductor cycle turning and a strategic exit from lower-margin businesses, the market is pricing in a return to profitable growth.

Latest Key Reasons for Surge & Drivers

Source: Kalkine Group

- Beating the "Cliff Edge" Fears (Liquidity Improved): The primary driver is the significant reduction in net debt. The latest update confirmed net debt dropped to £41.6 million (as of Dec 31, 2025), a massive reduction of £19.1 million from the previous quarter. This alleviates the bankruptcy/capital raise fears that plagued the stock in 2025.

- Strong Second-Half Recovery: The company confirmed a "significantly improved" second-half performance. Q4 revenue rose 2% to £61.2 million, but more importantly, order intake jumped 29% year-on-year. This indicates that customer destocking is over and demand is returning.

- Strategic RF Market Exit: Management announced a bold decision to exit the Radio Frequency (RF) market. While this reduces top-line revenue slightly, it is a low-margin, high-volatility segment. Investors cheered this move as it focuses capital on high-return "Power" divisions.

- Operational De-risking (China to Malaysia): The risk of keeping a major facility in Kunshan, China, has been neutralized. The new facility in Perak, Malaysia, is now complete and operational for 2026. This diversification mitigates geopolitical risks and lowers tariff exposure, a key win for institutional investors.

Current Business Model

XP Power operates on a "Design-In" model, which creates a high economic moat (defensive competitive advantage).

- Critical "Heart" of the Machine: They design power converters that are the "heart" of complex industrial machines. They are not a commodity supplier; they are an engineering partner.

- Sticky Revenue Stream: Once an XP Power unit is designed into a customer's machine (e.g., a semiconductor lithography tool or a hospital surgical robot), it stays there for the product's entire 5-7 year lifecycle. This guarantees recurring revenue without needing to re-win the business every year.

- Three Key Sectors:

- Semiconductor Manufacturing Equipment: Powering the machines that make chips (highly cyclical but high growth).

- Healthcare: Powering X-ray, MRI, and surgical devices (highly regulated, very stable).

- Industrial Technology: Robotics, test equipment, and smart grid tech.

Latest Company Financial & Operational Updates

(Source: XP Power Full Year Trading Update, Jan 19, 2026)

- Revenue & Orders: Full-year revenue for 2025 ended at £229.7 million (down 7% YoY), but the trajectory is the story: Q4 momentum is positive. Order book stands healthy at £116.1 million.

- Profitability: Adjusted Operating Profit for 2025 is expected to land around £17.3 million, which aligns with market consensus. This "meeting of expectations" was critical for restoring trust.

- Dividend Status: The dividend was paused in 2024 to preserve cash. While no new dividend was declared in the January update, the rapid debt reduction significantly brings forward the timeline for reinstating the payout, likely fueling the recent buying frenzy.

- Manufacturing: The closure of the Chinese facility in December 2025 and the full transition to Malaysia is a completed milestone, removing a major "execution risk" overhang.

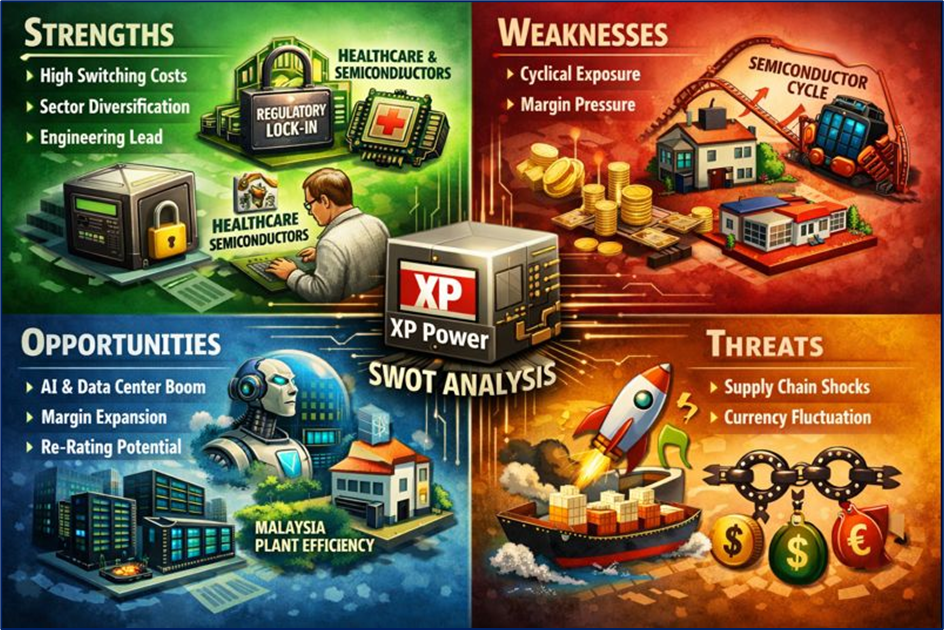

SWOT Analysis (as of Jan 2026)

Source: Kalkine Group

Strengths

- High Switching Costs: Customers cannot easily swap out XP Power units without expensive regulatory re-certification.

- Sector Diversification: The stability of Healthcare offsets the volatility of the Semiconductor sector.

- Engineering Lead: A massive library of proprietary designs makes them a default choice for engineers at blue-chip OEMs.

Weaknesses

- Cyclical Exposure: Despite diversification, ~40% of revenue is tied to the boom-and-bust semiconductor cycle.

- Margin Pressure: The transition between factories (China to Malaysia) has temporarily depressed margins, though this is expected to normalize in 2026.

Opportunities

- AI & Data Center Boom: The massive demand for chips (driven by AI) requires more semiconductor manufacturing equipment—XP Power's "sweet spot."

- Margin Expansion: Exiting the low-margin RF business and ramping up the efficient Malaysia factory could push operating margins back toward historical highs (18-20%).

- Re-rating: The stock is currently priced as a "distressed" asset. If it is re-rated as a "growth" asset, the multiple expansion could be significant.

Threats

- Supply Chain Shocks: Any disruption in raw material availability in Southeast Asia could impact the new Malaysia plant.

- Currency Fluctuation: As a UK-listed company with global revenues (mostly USD) and costs in Asian currencies, FX volatility impacts reported earnings.

Outlook & Risks

Outlook: The outlook for 2026 is cautiously bullish. The "destocking" phase (where customers used up old inventory instead of buying new) appears to have ended in Q4 2025. With the order book up nearly 30% and the distraction of the factory move behind them, management can focus purely on fulfilling demand. The semiconductor industry is widely forecasted to have a strong 2026, which serves as a massive tailwind for XP Power.

Risks:

- Execution Risk: Ramping up a new factory in Malaysia carries risks of teething issues or quality delays.

- Global Recession: If the global economy hard-lands, capital expenditure on industrial robots and medical devices will be cut, hurting XP's order book.

Compelling Conclusion

XP Power's 7.71% surge is a textbook example of a "relief rally" transitioning into a "recovery play." The company has survived its darkest hour—the cash crunch of 2024/25—and emerged leaner, with a better manufacturing footprint and a focused portfolio minus the RF drag. For investors, the narrative has shifted from “Will they survive?” to “How fast can they grow?” With the semiconductor super-cycle restarting and debt under control, XP Power is no longer fighting for air; it is preparing to swim.

Please wait processing your request...

Please wait processing your request...