Key Takeaways

- UK bank shares are rallying ahead of the 26 November 2025 Budget, fuelled by reports that the government will avoid new banking taxes.

- The FTSE 350 Banks Index has outperformed the wider market as investor sentiment shifts from caution to optimism.

- Analysts expect the Budget to prioritise stability, competitiveness, and confidence over fiscal tightening.

- Cooling inflation and a resilient economy are setting the stage for a renewed focus on growth and lending.

- If confirmed, the shift could restore London’s appeal as a global financial hub and boost long-term market confidence.

UK Bank Stocks Are Back in the Game

London’s banking heavyweights are staging a comeback. After months of policy uncertainty and fiscal speculation, the UK’s biggest lenders are back in the spotlight — and this time, the rally has real political momentum behind it.

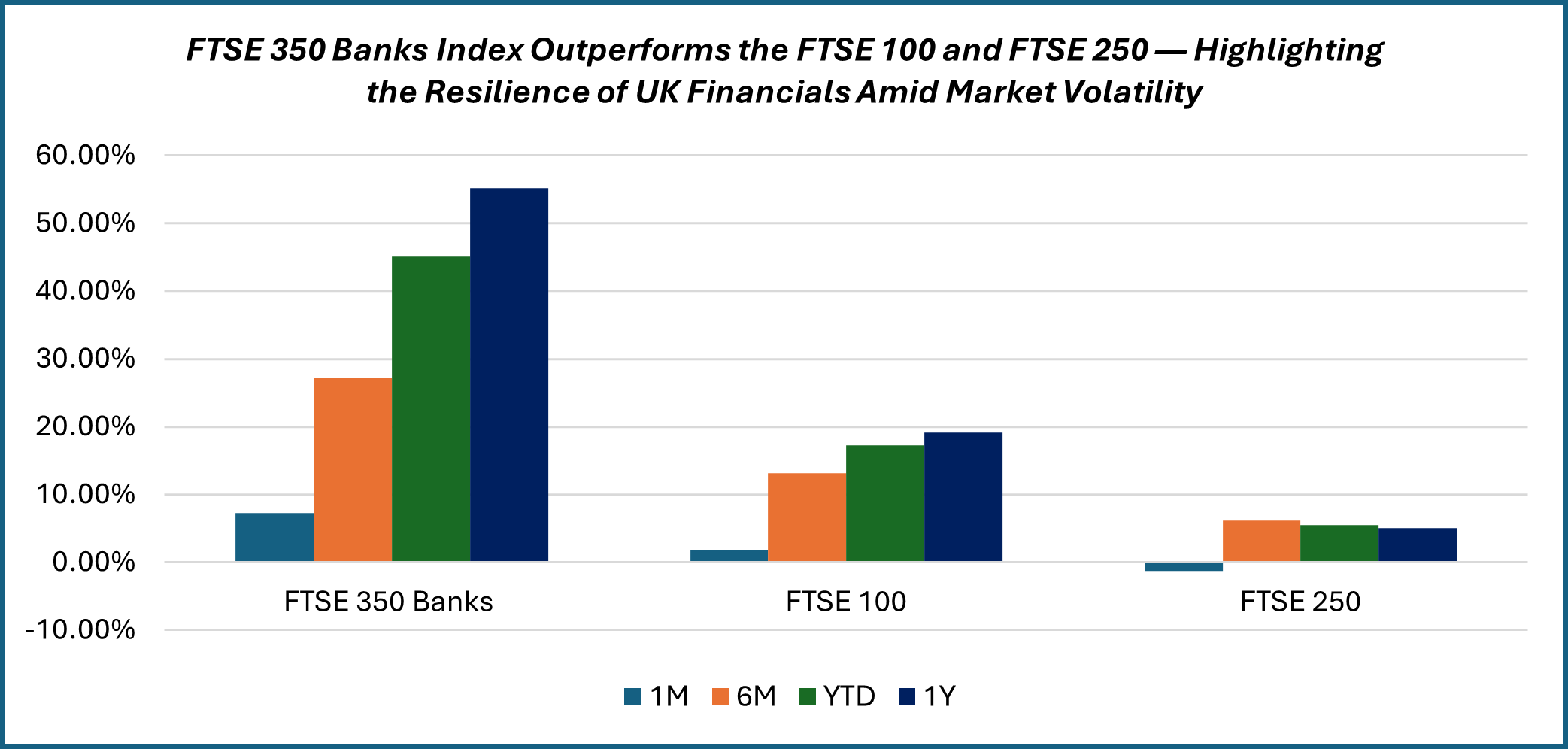

In early November 2025, the FTSE 350 Banks Index surged ahead of both the FTSE 100 and FTSE 250, following reports that Chancellor Rachel Reeves is unlikely to impose new levies on financial institutions in her upcoming Budget on 26 November 2025.

Data Source: EODHD/Others, Analysis: Kalkine Group, 10 November 2025

That single policy hint was enough to light up London’s trading floors — signalling relief across the City and triggering sharp rebounds in bank stocks.

What’s Fueling the Rally

For most of the year, the sector had been under pressure. Persistent rumours of a “windfall-style” tax — estimated to raise around £8 billion — had kept investors wary. But recent leaks suggest that the Treasury has dropped that idea in favour of a pro-growth, stability-focused fiscal stance.

The market reaction was instant:

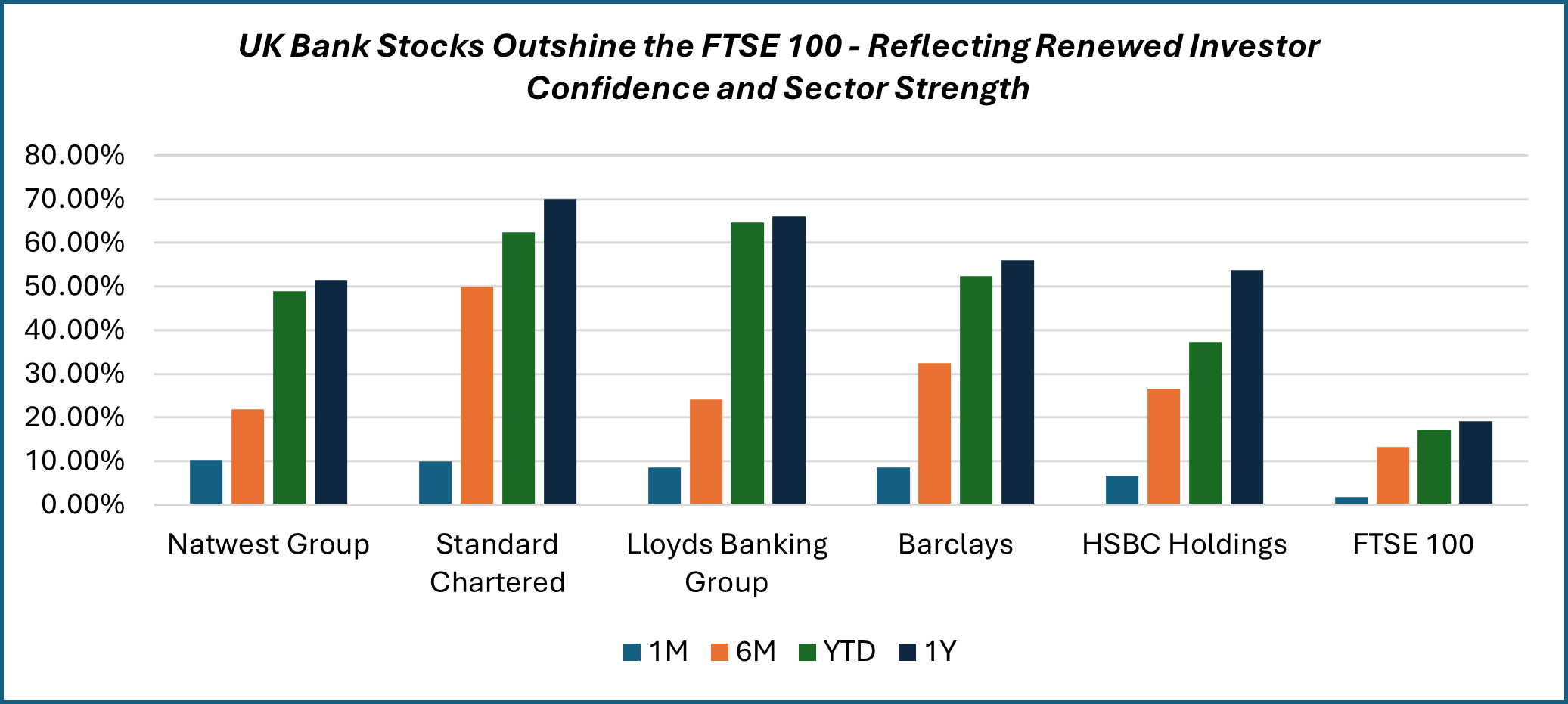

- NatWest Group PLC (LSE:NWG) - Shares have climbed about 10% over the past month, reflecting upbeat customer activity and growing market confidence that the upcoming Budget will avoid new levies on banks.

- Standard Chartered PLC (LSE:STAN) - Up roughly 9.8% in one month, as investors are responding to improved sentiment around cross-border trade flows and the group’s exposure to fast-growing Asian and African markets.

- Lloyds Banking Group PLC (LSE:LLOY) - Gained around 8.5% in the past month. The lift comes amid a recovery in UK retail lending and optimism that fiscal stability could support the domestic financial landscape.

- Barclays PLC (LSE:BARC) - Up nearly 8.6% in one month, reflecting the bank’s diversified business mix and fading tax concerns have helped restore market appetite for the stock.

- HSBC Holdings PLC (LSE: HSBA) - Gained by over 6% in last one month which highlights HSBC’s global reach and resilient income streams as factors aligning it with the broader upswing across UK banking names.

Data Source: EODHD/Others, Analysis: Kalkine Group, 10 November 2025

This isn’t just about share prices moving north — it’s about confidence returning to the sector. Investors see a government that’s choosing financial stability over fiscal short-termism.

The Macro Backdrop: A Turning Point

Throughout 2025, UK bank stocks lagged behind other sectors due to weak mortgage demand, cautious lending, and higher funding costs. Yet the landscape is now shifting.

- Inflation is easing, suggesting that the Bank of England (BoE) could begin rate cuts in 2026.

- The government’s new fiscal tone appears less punitive and more pragmatic.

Why This Matters for Retail Investors

Beyond the trading screens, the implications ripple through the broader economy:

- Policy clarity breeds confidence: Uncertainty around tax policy had been a major drag. The absence of new levies removes that cloud.

- London’s global image improves: A pro-finance Budget could strengthen the City’s standing as a trusted global hub for investment capital.

- Balance sheet flexibility: While not advice, stable policy typically gives banks more freedom to manage dividends, buybacks, and lending operations.

- Economic spillover: Healthier banks tend to mean easier lending conditions for small businesses and consumers — a key driver of real economy growth.

What to Watch in the 26 November Budget

As the Budget countdown begins, markets will be parsing every detail. Key focus areas include:

- No new banking taxes: Confirmation of this could spark another leg up in valuations.

- Fiscal tone: A business-friendly stance, especially toward green finance and small business lending, may further support sentiment.

- Growth forecasts: If GDP outlook stabilises, it reinforces confidence in the UK’s recovery story.

- Regulatory reforms: Any easing of capital or ring-fencing rules could unlock more liquidity in the system.

In essence, predictability — not stimulus — could be the biggest market driver this time.

The Market Mood: From Anxiety to Optimism

For much of the past year, investors viewed the UK financial sector through a lens of uncertainty: higher taxes, tight credit, and limited growth. Now, the tone is changing. The possibility of a stable policy regime, combined with a cooling economy and resilient balance sheets, has injected a sense of cautious optimism back into the market. The City of London thrives on confidence — and the Budget narrative seems to be restoring just that.

Please wait processing your request...

Please wait processing your request...