1. The Catalyst: Why Ocado Surged Today

The primary driver for the ~8% surge today is a specific, high-value financial update regarding Ocado’s critical partnership with US grocery giant, Kroger.

- The News: Ocado announced it will receive a $350 million (£275 million) lump-sum cash payment from Kroger.

- The Reason: This payment is compensation for Kroger’s decision to shut down three existing automated warehouses (Customer Fulfilment Centres or CFCs) and cancel the construction of a fourth one.

- The Market Reaction: While losing active warehouses is strategically negative, the market is cheering the immediate cash injection. Ocado has been burning cash to build this technology; getting a guaranteed $350m upfront (equivalent to years of fees) significantly de-risks their balance sheet in the short term.

In simple terms: Investors were terrified Kroger would walk away for free. Instead, Kroger is paying a hefty "break-up fee" for those specific sites, proving Ocado's contracts have teeth.

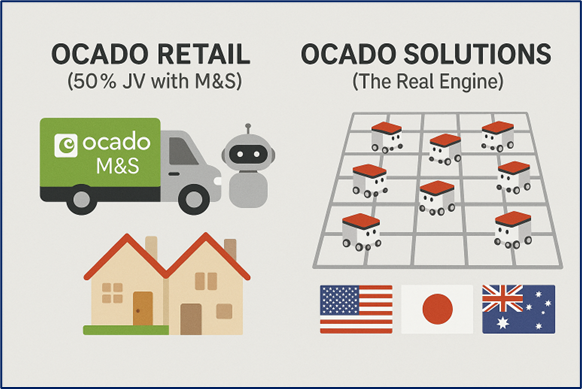

2. Business Model: The "Microsoft of Grocery"

To understand why this news matters, you must understand Ocado’s unique "dual" business model. They are not just a supermarket; they are a tech company.

- Ocado Retail (50% JV with M&S): This is the online supermarket UK consumers know. It delivers groceries to homes using automated vans and robots. It is a joint venture with Marks & Spencer.

- Ocado Solutions (The Real Engine): This is the B2B side. Ocado builds "hives"—massive grids of robots—for other supermarkets around the world (Kroger in the US, AEON in Japan, Coles in Australia). They license their hardware and software to these grocers.

- The Economic Moat: Supermarkets pay Ocado upfront fees to build the hive and recurring fees to operate it. This is where the long-term stock value lies.

Source: Kalkine Group

3. Why the Surge Makes Sense

Bulls (optimists) argue that today’s surge is justified because the $350m payment solves Ocado’s biggest immediate problem: Liquidity (Cash).

- Cash Flow Target Secured: Ocado has promised investors it will be "cash flow positive" by the financial year 2026. This $350m payment effectively guarantees they hit that target, removing the fear that they would need to ask shareholders for more money (dilution).

- Contract Validation: It proves that Ocado’s contracts are ironclad. Kroger couldn't just abandon the tech; they had to pay a massive penalty to reduce their capacity.

- Removal of Uncertainty: For weeks, rumors swirled that Kroger was unhappy. This settlement draws a line under that uncertainty. The partnership continues, albeit smaller (5 active sites remaining).

4. The Hidden Risks

Despite the 8% jump, the long-term picture remains complicated. The "Tocdo" surge might be a relief rally rather than a fundamental turnaround.

- The "Growth Story" is Broken: Ocado’s stock price was originally built on the idea that they would build hundreds of warehouses globally. Kroger closing three of them suggests the demand for automated grocery delivery in the US is lower than predicted.

- One-Off vs. Recurring Revenue: The $350m is a one-time sugar hit. Ocado lost the recurring annual fees those warehouses would have generated for the next 10-20 years. They traded long-term annuity income for immediate cash.

- Short Interest: Ocado is historically one of the most "shorted" stocks in London (meaning hedge funds are betting the price will fall). Today’s rise may be partly due to a "short squeeze"—funds buying the stock quickly to exit their negative bets—rather than genuine belief in the company.

5. Latest Business Updates (Dec 2025)

- Tech Rollout: Ocado is currently rolling out its "Re:imagined" technology—lighter, faster, 3D-printed robots that are cheaper to manufacture.

- UK Retail Performance: The UK joint venture with M&S is performing well, gaining market share as inflation eases, though it remains a low-margin business compared to the tech licensing side.

- Kroger Status: Despite closing three sites, Kroger and Ocado continue to operate five other sites (Dallas, Monroe, etc.). The partnership is "downsized," not dead.

6. Conclusion: A Bittersweet Victory

The surge in Ocado shares today is a classic case of "bad news that could have been worse."

The market is relieved that Ocado extracted a massive $350m payment from Kroger, securing its balance sheet for the next two years. However, the fundamental reality is that their biggest partner is shrinking, not expanding.

Today is a win for the accountants (better cash flow), but a question mark for the strategists (slower US growth).

Source: Trading View, 5 December 2025, 9:30 AM GMT

Please wait processing your request...

Please wait processing your request...