3 FTSE 250 Stocks Trending Up: Hochschild, Atalaya, & Pan African Resources

The FTSE 250 miners are currently staging a dramatic resurgence, capitalizing on what analysts are calling a "perfect storm" for commodities as of January 26, 2026. With gold smashing through the $5,100/oz barrier and copper tightening globally, the mid-cap mining sector is becoming a focal point for volume and volatility. Yesterday’s trading session saw distinct bullish momentum for Hochschild Mining, Atalaya Mining, and Pan African Resources, driven not just by soaring spot prices but by pivotal operational breakthroughs that have fundamentally de-risked their investment cases.

As inflation remains sticky and geopolitical fractures deepen, these three miners have released timely updates that suggest they are transitioning from capital-intensive development phases into periods of significant free cash flow generation.

Hochschild Mining PLC (LON: HOC)

Source: Kalkine Group

Surge Drivers & Recent Performance Hochschild Mining’s stock recently hit new multi-year highs, riding the tailwinds of a silver price explosion that has seen the metal breach $110/oz. The primary catalyst for the January 26 surge is the market's reaction to the company’s ability to leverage these historic prices despite operational headwinds. Investors are cheering the "pure-play" precious metals exposure Hochschild offers, which acts as a leveraged bet on silver and gold. The sentiment is further buoyed by the stabilising production at its flagship Inmaculada mine, which has calmed fears regarding permit renewals that plagued the stock in previous years.

Business Model Hochschild operates as a leading underground precious metals producer with a primary focus on high-grade silver and gold deposits in the Americas. Its core operations include the Inmaculada and Pallancata mines in southern Peru, the San Jose mine in Argentina, and the recently commissioned Mara Rosa gold mine in Brazil. The business model relies on discovering and operating high-grade epithermal vein deposits, processing ore into doré or concentrate, and shipping to international refineries.

Latest Financial & Operational Update (Source: 2025 Full Year Production Update, Jan 2026)

- Production: The company reported that 2025 production numbers contained "no nasty surprises," broadly meeting revised guidance.

- Guidance: 2026 forecasts indicate a slight dip in output and a rise in All-In Sustaining Costs (AISC), but this is vastly outweighed by the current gold price of ~$5,100/oz and silver prices.

- Mara Rosa: The Brazilian mine produced ~40,060 ounces in 2025, undershooting targets, but a new management team is in place to target 67,000–80,000 ounces in 2026.

- Financial Health: Net debt has been reduced significantly, aided by strong cash flows from Argentine operations.

SWOT Analysis

- Strengths: High-grade asset base; significant leverage to silver prices; diversified footprint across three countries.

- Weaknesses: High cost structure relative to peers; operational teething issues at Mara Rosa; declining grades at mature assets like San Jose.

- Opportunities: Exploration potential at Royropata (Peru) could extend mine life significantly; M&A opportunities in the Americas; sustained bull market in precious metals.

- Threats: Geopolitical instability in Peru and Argentina; currency controls in Argentina affecting cash repatriation; fluctuations in energy and labour costs.

Outlook & Risks The outlook for Hochschild is cautiously optimistic, hinged entirely on the "margin expansion" story. While costs are rising, the revenue per ounce is rising faster. The critical risk remains operational execution at Mara Rosa; if the new team fails to rectify the mechanical filtration issues, it could drag on the group's overall efficiency. Additionally, any sharp correction in silver prices would disproportionately hurt HOC given its high beta nature.

Atalaya Mining PLC (LON: ATYM)

Source: Kalkine Group

Surge Drivers & Recent Performance Atalaya Mining is trending upwards as copper prices hit record highs above $5/lb, driven by supply deficits and green energy demand. The stock’s momentum on January 26 is supported by a robust Q4 operational update that confirmed the company beat its production guidance for the full year 2025. The market is rewarding Atalaya for its reliability and its fortress balance sheet, which stands in stark contrast to many debt-laden peers in the sector.

Business Model Atalaya is a European copper producer operating the historic Riotinto Copper Project in southwest Spain. Its business model focuses on open-pit mining and processing of sulphide ores to produce copper concentrates with silver by-products. The company is actively expanding its resource base through satellite deposits (San Dionisio, San Antonio) and developing its proprietary E-LIX technology to unlock value from complex polymetallic ores, potentially revolutionizing its recovery rates.

Latest Financial & Operational Update (Source: Q4 2025 Operations Update, Jan 14, 2026)

- Production Beat: Achieved 51,139 tonnes of copper in FY2025, hitting the upper end of its 49k-52k tonne guidance range.

- Record Throughput: The processing plant set a new throughput record, signaling high operational efficiency.

- Financials: Maintained a strong net cash position despite heavy capital investment in the E-LIX plant and solar power initiatives.

- Expansion: Confirmed progress on the San Dionisio expansion, which will provide higher-grade ore to the plant.

SWOT Analysis

- Strengths: Tier-1 jurisdiction (Spain); strong balance sheet with net cash; proprietary E-LIX technology offering potential cost advantages.

- Weaknesses: Single-asset risk (heavy reliance on Riotinto); lower-grade ore body compared to major global mines.

- Opportunities: Approval of the Touro project in Galicia could double production profile; successful commercialization of E-LIX technology; expansion of the Riotinto district resource.

- Threats: Energy cost volatility (though mitigated by solar plant); regulatory delays regarding the Touro environmental permits; water scarcity in southern Spain.

Outlook & Risks Atalaya's outlook is robust, with 2026 production guidance positioning it well to capture high copper prices. The integration of higher-grade ore from San Dionisio is a key value driver. The primary risk lies in the execution of the E-LIX rollout and the perennial wait for the "Project Touro" approvals. However, as a producing asset in a safe jurisdiction during a copper supply crunch, the downside appears buffered by strong fundamentals.

Pan African Resources PLC (LON: PAF)

Source: Kalkine Group

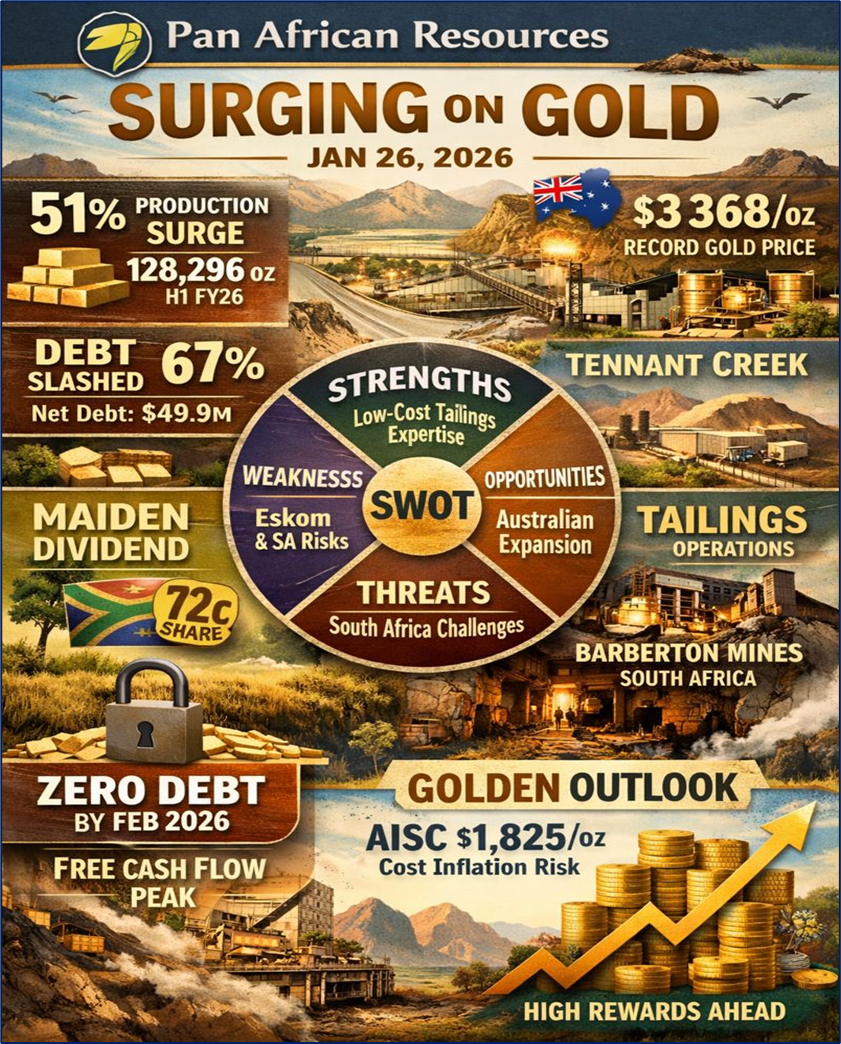

Surge Drivers & Recent Performance Pan African Resources was a standout performer on January 26, 2026, with shares jumping over 5% following a stellar operational update. The company announced a massive 51% surge in gold production for the half-year, driven by the successful integration of its Australian assets and the ramp-up of its tailings operations. The announcement of a maiden interim dividend was the "cherry on top" that triggered the buy-side volume, signaling management's confidence in sustained cash flows.

Business Model Pan African is a mid-tier African gold producer with a dual focus: high-margin, long-life surface tailings retreatment operations (Elikhulu, Mogale) and high-grade underground mining (Barberton, Evander) in South Africa. It has recently diversified geographically by acquiring the Tennant Creek assets in Australia. The model prioritizes low-cost gold recovery from waste (tailings), which reduces geological risk and environmental liability, funding its growth and dividends.

Latest Financial & Operational Update (Source: Operational Update H1 FY26, Jan 26, 2026)

- Production Explosion: Gold production rose 51% to 128,296oz for the six months ended Dec 2025.

- Debt Collapse: Net debt was slashed by 67% to just $49.9m; the company expects to be fully de-geared (zero net debt) by the end of February 2026.

- Dividend: Declared a maiden interim dividend of ZA 12 cents per share, a major signal of financial maturity.

- Realized Price: Achieved an average gold price of $3,368/oz, up 43% year-on-year.

SWOT Analysis

- Strengths: Industry-leading expertise in tailings retreatment; very low cost of production at Elikhulu; rapidly deleveraging balance sheet; geographic diversification into Australia.

- Weaknesses: Exposure to South African power grid instability (Eskom) and crime; deep underground mines at Barberton are labour-intensive and costly.

- Opportunities: Expansion of the Mogale Tailings Retreatment (MTR) plant; further high-grade discoveries at Tennant Creek (Australia); renewable energy projects reducing reliance on the grid.

- Threats: Wage inflation and union strikes in South Africa; illegal mining activities disrupting operations; volatility in the ZAR/USD exchange rate.

Outlook & Risks The outlook for Pan African is exceptionally strong as it enters a "harvest phase." With the heavy capital expenditure for the MTR project largely behind it and the Australian assets contributing, free cash flow is set to peak. The main risks are cost inflation (AISC expected to rise to $1,825/oz) and the perpetual operational risks associated with deep-level mining in South Africa. However, the move to become debt-free by February 2026 provides a massive buffer against these risks.

Conclusion

The simultaneous rise of Hochschild, Atalaya, and Pan African Resources highlights a broader rotation back into tangible assets. These companies have moved beyond mere speculation, delivering concrete production beats, debt reductions, and dividend initiations at the precise moment commodity prices are skyrocketing. While risks regarding cost inflation and geopolitical stability remain, the current trajectory for these FTSE 250 miners suggests they are well-positioned to capitalize on the 2026 commodity supercycle.

Please wait processing your request...

Please wait processing your request...