Oxford Biomedica (LSE: OXB) caught the eyes of retail and institutional investors alike on December 23, 2025, as its share price climbed approximately 6%. After a transformative year that saw the company re-enter the FTSE 250, this pre-Christmas rally signals a growing market consensus that the "New OXB" strategy is hitting its stride.

Why the 6% Jump? The Key Drivers

The rally on December 23 isn't just a "Santa Rally"; it’s the culmination of a year-long pivot toward becoming a global leader in the high-stakes world of cell and gene therapy (CGT).

Source: Kalkine Group

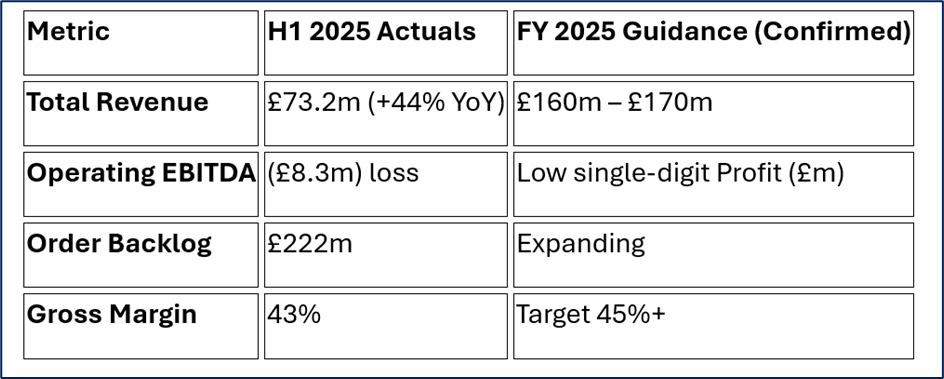

- Late-Stage Commercial Momentum: Throughout H2 2025, OXB has seen a surge in manufacturing orders as clients move from clinical trials toward commercial launches. Investors are betting on the "weighted" H2 revenue model previously guided by management.

- The "One OXB" Integration: The market is rewarding the successful integration of its US and French sites. Having a "pure-play" CDMO (Contract Development and Manufacturing Organisation) model across three major territories (UK, US, France) has reduced geographic risk.

- Path to Profitability: With H1 2025 showing a 59% reduction in EBITDA losses, the 6% jump likely reflects end-of-year confidence that the company will achieve its goal of low single-digit operating EBITDA profitability for the full year 2025.

Latest Business Model: The CDMO Pivot

Oxford Biomedica has officially shed its skin as a drug-developer-plus-manufacturer to become a Pure-Play CDMO.

The "One OXB" Strategy

Instead of relying on royalties from a few blockbusters (like the Novartis Kymriah deal), OXB now functions as the "intel inside" for dozens of biotech firms.

- Multi-Vector Approach: They no longer just do Lentivirus. They have expanded heavily into AAV (Adeno-associated virus) and Adenoviral vectors, making them a one-stop shop for the industry.

- End-to-End Services: From early-stage "process development" (helping biotechs design the virus) to "commercial GMP manufacturing" (producing it at scale for the public).

Latest Financial & Operational Updates

The 2025 fiscal year has been a "repair and grow" story.

Financial Health at a Glance

Source: Kalkine Group

Operational Milestones

- US Expansion: Completed the 100% acquisition of its US subsidiary in June 2025, allowing for a unified commercial push in the world’s largest healthcare market.

- Capacity Boost: Announced a refit of UK suites to increase GMP manufacturing capacity, expected to be fully online by H1 2026.

- New Revenue Streams: Successfully launched "Procurement and Storage Services," adding £8.6m in H1 alone by managing supply chains for its clients.

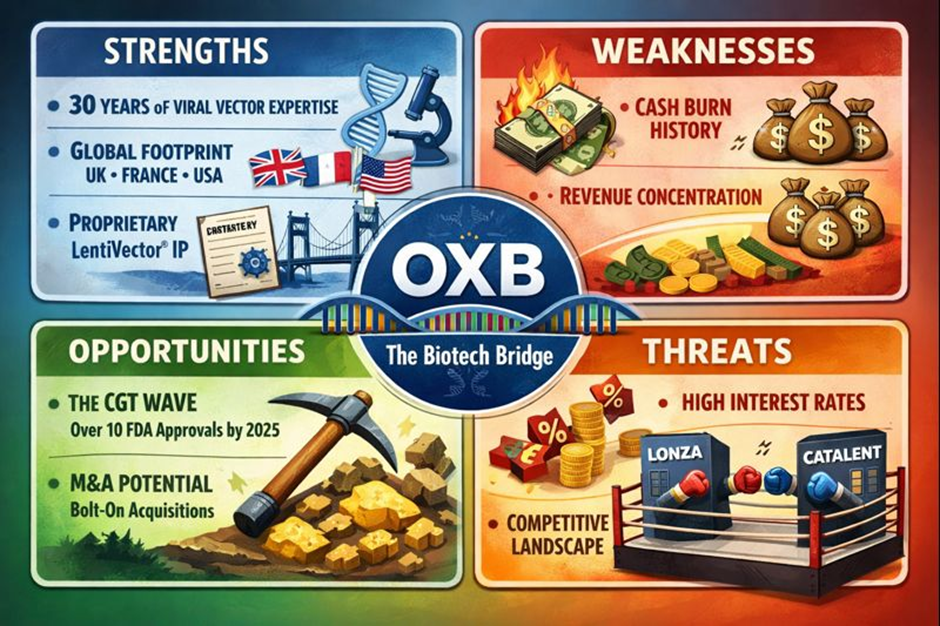

SWOT Analysis: The 2025 Reality

Source: Kalkine Group

Strengths

- Deep Heritage: 30 years of experience in viral vectors—a "moat" that is hard for new competitors to replicate.

- Global Footprint: Operational bases in the UK, France, and the US provide a unique "Atlantic bridge" for biotech clients.

- Proprietary IP: Patents like the LentiVector® platform provide superior yields, making them a preferred partner.

Weaknesses

- Cash Burn History: While narrowing, the company has historically burned through significant cash to fund its expansion.

- Revenue Concentration: Though diversifying, a large chunk of revenue still stems from a handful of key partnerships.

Opportunities

- The CGT Wave: Over 10 FDA approvals for cell and gene therapies were expected in 2025; OXB is the "picks and shovels" provider for this gold rush.

- M&A Potential: With a strengthened balance sheet, OXB is now a hunter, looking for smaller tech-bolt-ons to improve manufacturing yields.

Threats

- High Interest Rates: As a growth-oriented stock, OXB remains sensitive to the cost of capital for its biotech clients.

- Competitive Landscape: Giants like Lonza and Catalent are aggressive in the viral vector space, leading to potential price wars.

The Risks: What Could Go Wrong?

- Clinical Failure: If a major client’s Phase III trial fails, OXB loses the future manufacturing revenue associated with that drug.

- Regulatory Hurdles: The FDA and EMA are increasingly strict on manufacturing standards for gene therapies. Any "Notice of Observation" (Form 483) could halt production.

- Dilution: While the £60m share placing in late 2024/early 2025 shored up the balance sheet, investors remain wary of further equity raises.

Conclusion

Oxford Biomedica’s 6% rise on December 23, 2025, appears to be a vote of confidence in the company's industrialization. By moving away from the volatility of drug discovery and toward the steady, high-margin world of specialized manufacturing, OXB is positioning itself as a cornerstone of the UK’s life sciences sector. With a record backlog and a clear path to being "in the black," the FTSE 250 stock is no longer just a "Covid vaccine play," but a fundamental pillar of the genomic medicine revolution.

Source: Trading View, 23 December 2025, 1:15 PM GMT

Please wait processing your request...

Please wait processing your request...