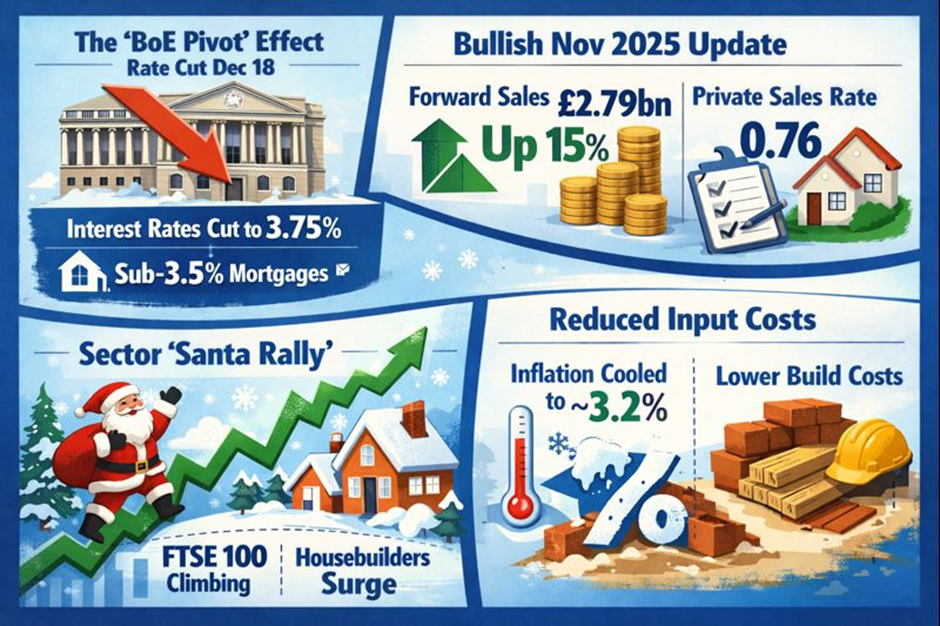

The Christmas Eve Move: What Happened?

On a shortened trading day (December 24, 2025), Persimmon PLC (LSE: PSN) closed up ~1.02% at GBX 1,336. While a 1% move might seem modest, in a low-volume holiday session, it signals institutional positioning and "quiet confidence" heading into 2026. This wasn't just festive cheer; it was a response to a pivotal December for the UK housing sector.

Key Reasons & Drivers (Why the Green Candle?)

Source: Kalkine Group

- The "BoE Pivot" Effect (Dec 18 Rate Cut)

The heavy lifting happened last week. The Bank of England’s decision on December 18 to cut the base rate to 3.75% (down from 4.0%) is the primary engine. Mortgage lenders have already started pricing this in, with sub-3.5% five-year fixed deals appearing for the first time in years.

- Impact: Lower rates directly boost Persimmon’s core demographic—first-time buyers (FTBs) sensitive to monthly payments.

- Bullish Nov 2025 Trading Update

Investors are still digesting the surprisingly strong November update.

- The Stat: Forward sales are up 15% year-on-year to £2.79bn.

- The Signal: A net private sales rate of 0.76 (vs 0.70 in 2024) proves demand is returning before the full rate-cut effect kicks in.

- Sector-Wide "Santa Rally"

The FTSE 100 often drifts higher on Christmas Eve due to low liquidity ("window dressing" by fund managers). However, housebuilders outperformed the index, suggesting sector rotation away from defensives and into cyclical recovery plays for 2026.

Recent data indicates stabilization in build costs. With inflation cooling to ~3.2% (Nov 2025), Persimmon’s vertically integrated model (making its own bricks/timber) is capturing margin expansion faster than peers who rely entirely on external supply chains.

Latest Business Model: "The Factory Advantage"

Persimmon isn’t just a builder; it’s a manufacturer. In 2025, this vertical integration became their "moat."

- Space4 (Timber Frame): Now producing ~45-50% of their homes using timber frames (up from 25% in 2023). This speeds up build times and reduces on-site labor reliance.

- Brickworks & Tileworks: By manufacturing their own concrete bricks and roof tiles, Persimmon saves roughly £1,600 - £2,100 per plot. In a competitive market, this margin buffer allows them to undercut peers on price while maintaining profitability.

- FibreNest: Their owned ISP ensures homes are "internet ready," adding a recurring revenue stream and boosting customer satisfaction scores (now consistently above 90%).

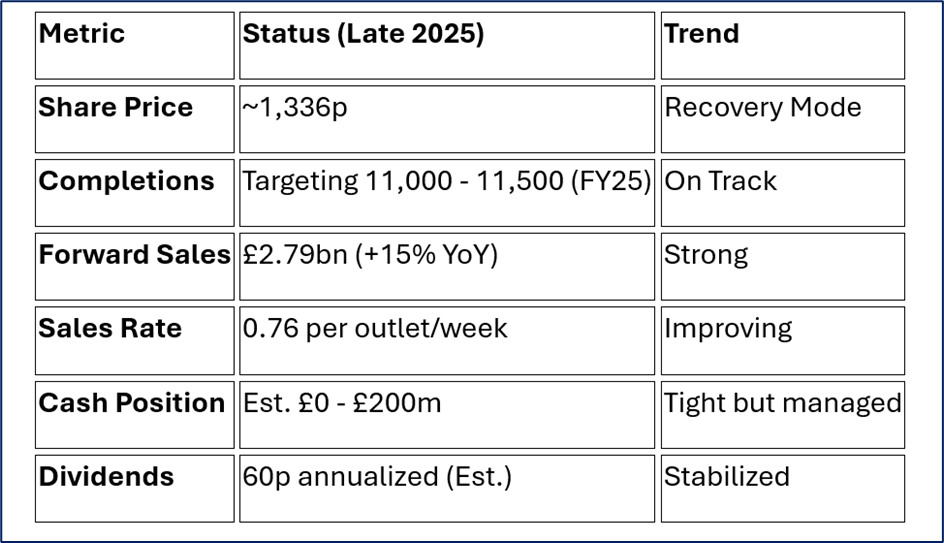

Financial & Operational Pulse (Q4 2025 Update)

Source: Company Data

Analyst Note: The valuation remains attractive at ~14x P/E compared to the historical average, especially if 2026 volume targets (12,000+ homes) are hit.

SWOT Analysis (Strategic Snapshot)

Source: Kalkine Group

Strengths (Internal)

- Land Bank: High-quality land holdings (c. 82,000 plots) bought at historically lower costs than competitors.

- Margins: Vertical integration (Brickworks/Space4) protects gross margins against supply chain shocks.

- Brand Tiering: Distinct brands (Persimmon for affordability, Charles Church for premium) capture a wider market share.

Weaknesses (Internal)

- Legacy Perception: Despite recent 5-star HBF ratings, the brand still battles historical stigma regarding build quality in some regions.

- Geographic Concentration: Heavy exposure to regions where economic recovery is slower (e.g., North of England) compared to London-centric peers.

Opportunities (External)

- Planning Reform: The government's 2025 "Grey Belt" release initiative could unlock cheap land for Persimmon’s standard house types.

- Green Premium: Expanding timber-frame production (Space4) aligns with new Future Homes Standard regulations, potentially allowing premium pricing for energy-efficient homes.

Threats (External)

- Regulatory "Tax": Increasing costs from Section 106 agreements and the Residential Property Developer Tax (RPDT).

- Rate Volatility: Any surprise uptick in inflation in early 2026 could reverse the mortgage rate improvements, freezing the FTB market again.

Key Risks to Watch in 2026

- Mortgage Availability: While rates are cutting, lenders are strict on "affordability tests." If unemployment ticks up (current UK rate ~4.3%), approvals could stall.

- Cost Inflation Reboot: Energy prices remain volatile. A spike in energy costs hurts the manufacturing side (Brickworks) and the consumer wallet simultaneously.

- Labour Shortage: As volume recovers to 12,000+ homes, the industry-wide shortage of bricklayers and joiners could cap growth, though Space4 (off-site manufacturing) mitigates this.

Conclusion: The "Sleep Well" Stock?

Persimmon’s 1% rise on Christmas Eve 2025 wasn't a fluke; it was a validation of stability. The company has successfully navigated the "affordability crunch" of 2023-2024 and emerged leaner, with a more efficient manufacturing engine.

While it lacks the explosive growth of a tech stock, PSN enters 2026 with a stronger order book, lower interest rate tailwinds, and a manufacturing edge that peers cannot easily replicate. For the retail investor, the story has shifted from "recovery" to "efficiency."

Please wait processing your request...

Please wait processing your request...