Marston’s PLC (LSE: MARS), one of the UK's leading pub operators with an estate of over 1,300 sites, sent its shares soaring by over 10% today following the release of its preliminary results for the 52 weeks ended September 27, 2025. The results confirm a dramatic and successful pivot in the company's operating model, showcasing massive profit expansion and a successful debt reduction strategy that defied the challenging consumer environment.

The market reaction is a clear vote of confidence, signalling that Marston's is no longer solely a macro-sensitive UK pub chain, but an efficiently run, high-margin hospitality business.

The Core Driver: Financial Results that Shatter Expectations

The immediate catalyst for the stock surge is the exceptional leap in profitability, which was ahead of market expectations. This financial step-change underscores the success of management's strategic focus on efficiency and margin expansion.

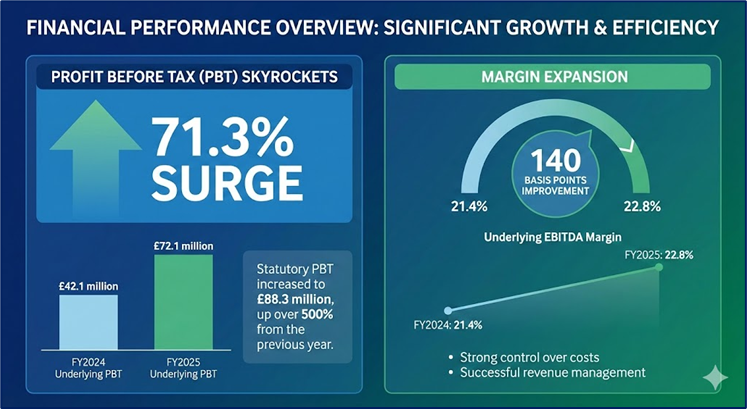

- Profit Before Tax (PBT) Skyrockets: Underlying PBT surged by a remarkable 71.3% to £72.1 million (FY2024: £42.1 million). The statutory PBT result was an even more dramatic increase to £88.3 million, up over 500% from the previous year.

- Margin Expansion: Underlying EBITDA margin improved by 140 basis points to 22.8% (FY2024: 21.4%), demonstrating strong control over costs and successful revenue management.

- Revenue Stability: Total revenue remained largely flat at £897.9 million, successfully offsetting the impact of around £50 million in non-core pub disposals undertaken in the prior period.

- Recurring Free Cash Flow (RFCF) Beat: RFCF reached £53.2 million, exceeding the £50 million target set at the Capital Markets Day and achieved ahead of schedule.

Source: Kalkine Group

Operational Excellence: The Engine Behind the Margins

The impressive financial turnaround is rooted in Marston’s aggressive and successful operational overhaul, which has targeted higher-margin formats and technological integration.

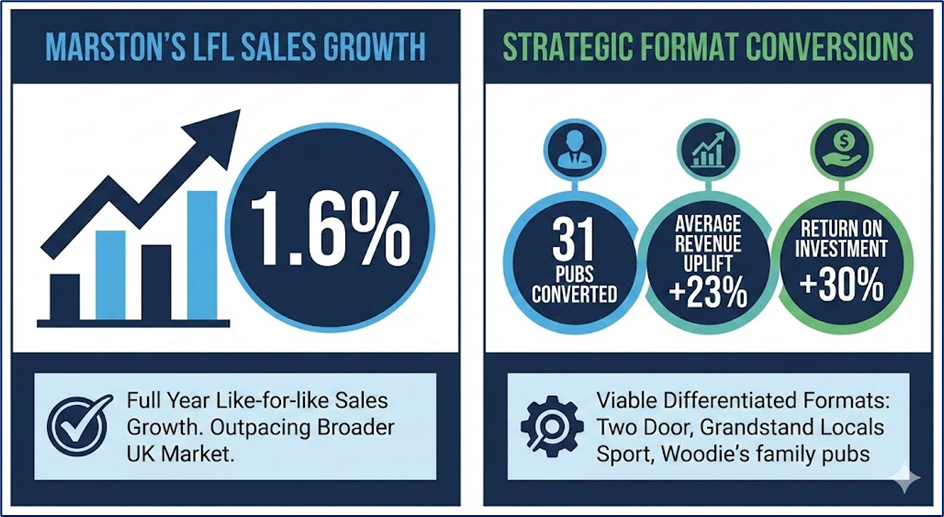

- LFL Sales Growth: Like-for-like (LFL) sales for the full year grew by 1.6%, confirming Marston’s continued ability to outpace the broader UK market.

- Strategic Format Conversions: The company successfully converted 31 pubs (e.g., to Two Door, Grandstand Locals Sport, and Woodie’s family pubs), which are delivering average initial revenue uplifts of 23% and a 30% Return on Investment (ROI). This proves the viability of their differentiated formats.

- Digital Transformation: The accelerated rollout of its Order & Pay digital platform across managed sites is driving a 10%+ uplift in revenue per transaction by enhancing speed of service and upsell opportunities.

- Record Guest Satisfaction: Operational improvements, including data-driven labor efficiency and superior procurement, have directly translated into record high guest satisfaction scores.

Source: Kalkine Group

Business Model & Guidance: A Deleveraging Growth Story

Marston's current business model is clearly shifting from one of legacy asset management to one of high-margin, guest-centric hospitality focused on managed pubs.

- Debt Reduction: The strong free cash flow generation has enabled a significant reduction in Net Debt (pre-IFRS 16), which decreased to £837.5 million (FY2024: £883.7 million), and reduced the crucial Net Debt/EBITDA ratio to 4.6x (FY2024: 5.2x). This is a vital step toward strengthening the balance sheet.

- Accelerated Capex: The company is reinvesting its success, with capital expenditure rising to £61.2 million (FY2024: £46.2 million). This investment is strategically directed towards accelerating the rollout of the high-ROI pub formats in FY2026.

- Guidance (FY2026 Outlook): The outlook remains strongly positive. Christmas bookings are already tracking 11% ahead of the same point last year, and the company views itself as well-positioned for continued progress, supported by the World Cup 2026 calendar and the ongoing acceleration of profitable format conversions.

Risk Factors: Navigating Macroeconomic Tides

Despite the strong results, Marston’s still faces inherent industry risks that require disciplined management:

- Consumer Sentiment: The UK consumer remains under pressure from high inflation and interest rates, which could potentially impact discretionary spending on food and drink.

- Cost Inflation: While efficiency measures have absorbed most of the pressure, cost inflation, particularly in wages (National Living Wage) and utilities, remains a persistent headwind.

- Competition: The highly fragmented pub sector faces intense competition, especially in the festive season, demanding continuous innovation in offering and pricing.

Conclusion: Marston's is Back in the Game

Today’s preliminary results confirm a fundamental shift in the Marston's story. The company has delivered a second consecutive year of major profit growth, moving decisively past the challenges of the recent past. The 71% PBT surge is not accidental; it is the direct result of a well-executed strategy focusing on operational discipline, digital integration, and high-yielding format conversions.

By generating significant recurring free cash flow and actively deleveraging its balance sheet, Marston's is building a resilient, high-quality hospitality platform. The strong Christmas bookings provide a tailwind for FY2026, bolstering the view that this is a sustainable recovery, transforming Marston's into a powerful engine for value creation in the UK pub sector.

Source: Trading View, 25 Nov 2025, 10 AM GMT

Please wait processing your request...

Please wait processing your request...