The "Recruitment Recovery" Trade: Why Now?

The ~3.7% lift on December 29 is largely driven by macro-positioning and internal efficiency gains hitting their stride.

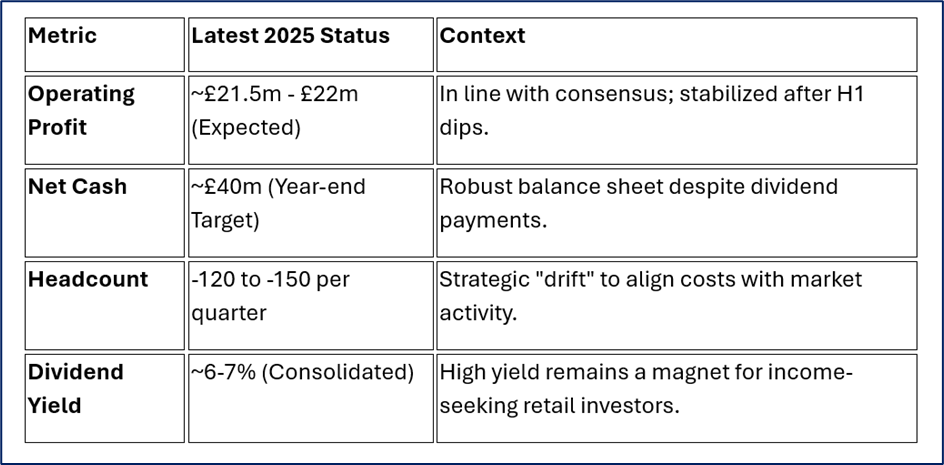

Source: Kalkine Group

- Bottoming Out in Major Markets: Recent Q3 and Q4 data signaled that while Germany and France remain soft, the US and Asia (specifically India and Hong Kong) have entered their second and fourth consecutive quarters of growth, respectively. Investors are betting that the "recruitment trough" is over.

- Cost-Optimization Alpha: The market is reacting to the successful execution of PageGroup’s £15 million cost-savings program announced earlier in 2025. With these structural cuts now largely complete, the "operating leverage" for 2026 looks significantly higher.

- The "January Effect" Front-Running: In the recruitment world, the New Year often brings a surge in hiring budgets. Savvy retail and institutional investors are likely "front-running" the January 13, 2026, Q4 Trading Update, expecting a stabilization in UK and European markets.

The 2025 Business Model: Agility Over Scale

PageGroup has shifted away from the "headcount-at-all-costs" model of 2022. The latest model focuses on:

- High-Margin Disciplines: Strategic focus on Page Executive (senior leadership) and Technology, which now represent a massive chunk of Group gross profit.

- Flexible Labor Shift: Increasing the ratio of Temporary and Interim roles (currently outperforming Permanent) to provide stable cash flow during economic volatility.

- Organic Scalability: Unlike competitors who grow through M&A, PageGroup maintains a "home-grown" management model, allowing them to shrink teams via natural attrition during downturns and scale instantly during booms.

Financial & Operational Flashlight

Source: Company Data

SWOT Analysis

Source: Kalkine Group

Strengths

- Global Diversification: Strength in India and the US offsets the malaise in the UK/Germany.

- Pricing Power: Despite lower volumes, fee rates have remained historically high.

- Cash Rich: No debt and a healthy cash pile allow for "special dividends" when markets normalize.

Weaknesses

- Permanent Recruitment Exposure: Highly sensitive to "candidate confidence," which has been low due to global inflation.

- UK Concentration: The closure of some UK Page Personnel lines has led to short-term revenue drag.

Opportunities

- AI Efficiency: Implementation of Copilot and AI-driven CRM tools is reducing the time-to-hire, boosting consultant productivity.

- The 2030 Strategy: Targeting an operating profit of £400m by 2030—nearly double the current run rate.

Threats

- Structural Wage Stagnation: If salary hikes stay muted, the commission-based model faces a ceiling.

- Geopolitical Tariffs: Increased global trade uncertainty (specifically US/China) can freeze hiring in the manufacturing and tech sectors.

The Risk Radar

While the stock is trending upward, risks remain. The conversion of interviews to offers is still the "most significant challenge" for the board. If the Q4 update (Jan 13) shows that European hiring is still in the freezer, today’s gains could quickly evaporate. Additionally, any further "derecognition of overseas losses" could impact the effective tax rate and net earnings.

Conclusion

PageGroup’s 3.7% jump on Dec 29 isn't just a random fluctuation; it’s a signal that the market is beginning to reward the firm’s aggressive cost restructuring and its geographic hedge. With the stock trading significantly below its 52-week highs but showing technical support near 225p, it is currently a "recovery story" in progress.

Please wait processing your request...

Please wait processing your request...