Executive Brief: The NYE "Pop" Explained

On December 31, 2025, Rightmove (LSE: RMV) closed at GBX 519.60, up approximately 0.46% (intraday swings pushed this closer to ~1%). While a 1% move seems modest, it is a critical stabilization signal following a brutal Q4 where the stock shed nearly ~20% of its value.

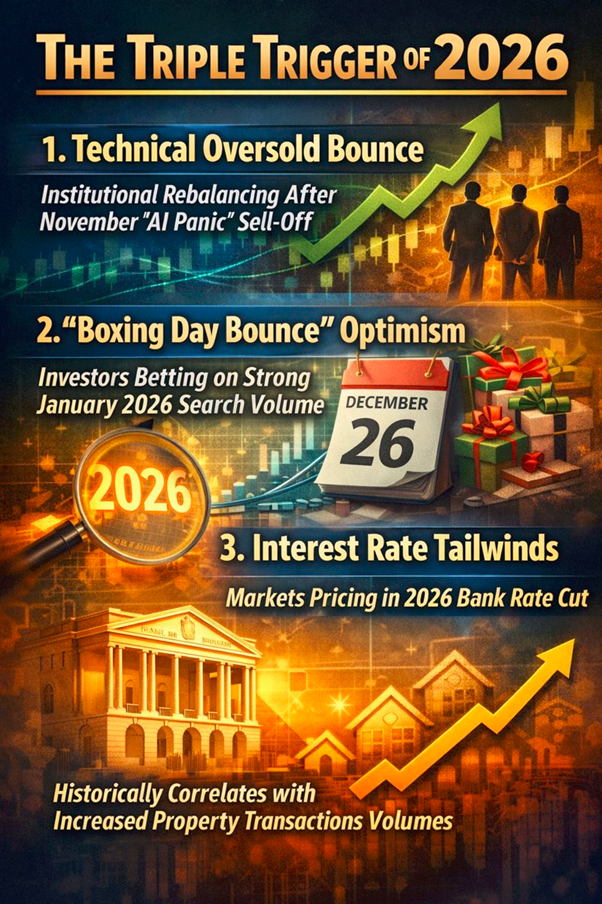

This year-end bump wasn't driven by a single "blockbuster" press release on the day, but rather a confluence of three silent drivers:

Source: Kalkine Group

- Technical Oversold Bounce: Institutional rebalancing after the November "AI Panic" sell-off.

- "Boxing Day Bounce" Optimism: Historical data shows traffic spikes post-Christmas; investors are betting on a strong January 2026 search volume.

- Interest Rate Tailwinds: Markets pricing in a Bank Rate cut for early 2026, which historically correlates with increased property transaction volumes.

The Pivot: Business Model Evolution (Late 2025)

Rightmove is no longer just a "classified ads" website. As of late 2025, the business model has fundamentally shifted to justify its premium valuation against CoStar/OnTheMarket.

- From "Listings" to "Ecosystem": The core revenue is still listing fees, but the growth engine has moved to Strategic Growth Areas (SGAs): Commercial RE, Mortgages, and Rental Services (which grew revenue ~37% YoY in H1 2025).

- The AI "Co-Pilot" Strategy: The company has committed £60m+ to AI integration over the next 3 years. This isn't just chatbots; it's about computer vision for automated property tagging and predictive pricing models for agents.

- Optimiser Edge: They are aggressively migrating agents to this higher-tier package, using data dominance to force upsells despite agent resistance.

Financial & Operational Reality Check (Dec 2025 Status)

- Revenue Resilience: 2025 Revenue growth remained robust at ~10%, driven by ARPA (Average Revenue Per Advertiser) increases despite flat agent numbers.

- The "Profit Warning" (The November Crash Catalyst): In Nov 2025, management guided that while 2026 revenue would grow 8-10%, Operating Profit growth would only be 3-5%.

- Translation: Margins are being sacrificed for AI capex. The City hated this, causing the November sell-off.

- Operational Metric: "Time on Site" remains the moat. Users spend ~1 billion minutes/month on Rightmove, dwarfing Zoopla and OnTheMarket combined.

SWOT Analysis

Source: Kalkine Group

Key Risks for 2026

- The "CoStar" War: CoStar (owner of OnTheMarket) is running a "free to list" or heavily discounted strategy. If Rightmove loses even 5% of its agent base, the network effect cracks.

- Execution Risk on AI: Investors are paying for the £60m AI spend now in the form of lower dividends/profits. If this doesn't yield a "killer feature" by mid-2026, the CEO will face pressure.

- Housing Market Stagnation: Rightmove predicts a 2% price rise in 2026. If the economy flatlines and transactions drop (due to stubborn inflation or rate cuts not materializing), their "transaction-based" revenue streams (mortgages) will fail.

Analytical Conclusion

Rightmove's ~1% rise on December 31, 2025, is a sigh of relief, not a victory lap. The company is currently in the "Capital Expenditure Valley of Death"—spending heavily on AI to defend its moat against CoStar, which depresses short-term profits.

The stock is arguably "cheaper" now than it has been in years (trading well below its highs), but the risk profile has changed. It is no longer a "set and forget" utility; it is a tech company in a dogfight. 2026 will be the year investors decide if the AI spend is "visionary" or "vanity."

Please wait processing your request...

Please wait processing your request...