Snapshot: The "Santa Rally" Outperformer

While the broader FTSE 100 index struggled to find momentum on a shortened Christmas Eve trading session (closing down ~0.2%), Schroders PLC (LSE: SDR) emerged as a standout performer. The stock climbed approximately 1.8% to close at GBX 407.40, marking it as one of the day’s top gainers alongside Persimmon and Melrose.

This move wasn't just holiday noise. It signals a potential shift in investor sentiment as we head into 2026, driven by a strategic turnaround that is finally bearing fruit.

- The "Why" Behind the Move: 3 Immediate Catalysts

Why did Schroders pop on a quiet half-day session when the rest of the market drifted lower?

Source: Kalkine Group

- Defensive Rotation into High Yield: With uncertainty lingering over 2026 growth forecasts, investors often rotate into high-quality, dividend-paying stocks before year-end. Schroders’ dividend yield, currently hovering around 5.3%, looks increasingly attractive as global interest rates begin to stabilize or fall (following the Fed’s Q3 2025 cuts).

- Institutional Accumulation: An RNS release on December 22, 2025, detailed changes in "Holdings in Company," often a signal that major institutional players are adjusting positions. The late buying pressure on Dec 24 likely reflects funds "window dressing" their portfolios to show exposure to a recovering asset manager before the books close for 2025.

- The "Private Assets" Premium: The market is still digesting the bullish signals from the Schroders Capital Investor Day (Dec 2, 2025). Investors are waking up to the fact that Schroders is no longer just a traditional stock-picker; it is becoming a private markets powerhouse.

Schroders has spent 2024 and 2025 fundamentally rewiring its engine. The old model (pure active public equities) is being supplemented by two high-margin growth engines:

- Schroders Capital (Private Assets): This is the crown jewel. By late 2025, Schroders Capital AUM reached ~£71.6bn. The new "Future Growth Capital" joint venture with Phoenix Group is a game-changer, unlocking billions in UK pension cash for private equity and infrastructure. This aligns perfectly with the UK government's "Mansion House" reforms.

- Wealth Management (Cazenove): Schroders has simplified its structure, regaining full ownership of Cazenove Capital while exiting sub-scale markets like Indonesia and Brazil. This division is now a "compounding machine," hitting £136bn+ in AUM with consistent positive inflows (5% net new business in Q3).

- Financial Health Check (Q4 2025 Context)

The Q3 2025 update (released Oct 2025) provided the hard numbers backing the current bullishness:

- Record AUM: Group Assets Under Management hit a record £816.7bn.

- Inflow Turnaround: The most critical metric—Net New Business (NNB)—flipped from negative in 2024 to +£9.4bn positive inflows YTD in 2025.

- Cost Discipline: The "simplification" program is delivering on its promise of £150m in annualized savings, improving operating margins even as they invest in new tech.

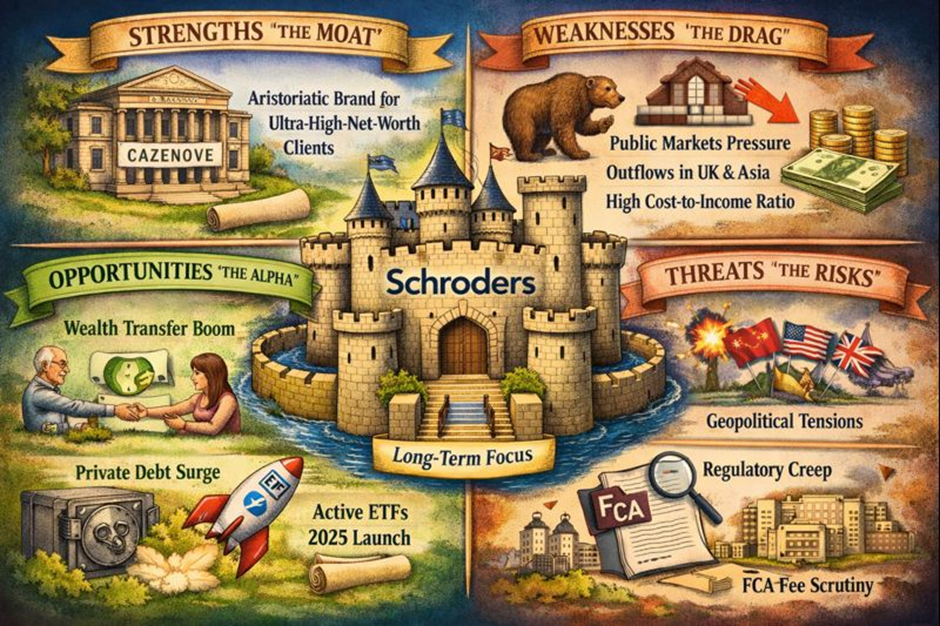

- SWOT Analysis: The Late 2025 View

Source: Kalkine Group

Strengths (The Moat): Schroders possesses a rare "aristocratic" brand in Cazenove that retains ultra-high-net-worth clients regardless of market cycles. Their balance sheet is robust with no significant debt maturity walls, and the family ownership structure (the Schroder family controls ~47%) allows them to take a long-term view that CEO-hopping competitors cannot match.

Weaknesses (The Drag): The legacy "Public Markets" business (traditional stock/bond funds) remains sensitive to fee compression. Outflows in Asian equities and UK institutional mandates have been a persistent drag, offsetting gains elsewhere. The cost-to-income ratio, while improving, remains higher than US peers like BlackRock.

Opportunities (The Alpha):

- The "Great Wealth Transfer": As baby boomers pass wealth to millennials, Schroders' modernized wealth platform is positioned to capture these flows.

- Private Debt Boom: With banks retreating from lending, Schroders' private credit arm is filling the void, earning higher spreads.

- Active ETFs: The 2025 launch of Active ETFs in Europe opens a new distribution channel to younger, tech-savvy investors who previously ignored mutual funds.

Threats (The Risks):

- Geopolitics: Significant exposure to Asia/China markets makes Schroders vulnerable to trade tensions or cooling growth in the East.

- Regulatory Creep: The UK FCA's scrutiny on "value for money" continues to cap fees on retail products.

- Key Risks to Watch in 2026

Despite the optimism, the path isn't entirely clear.

- Execution Risk: The pivot to private assets requires flawless execution. If the Phoenix JV fails to deploy capital effectively, the growth premium priced into the stock will vanish.

- Market Beta: If the "Soft Landing" narrative for the global economy turns into a "Hard Landing" in early 2026, asset managers—whose revenues are tied to asset prices—will be the first to fall.

Conclusion: A "Santa Rally" or a Structural Shift?

The 1.8% rise on Christmas Eve 2025 is more than just holiday cheer. It validates Schroders' grueling two-year transformation. The market is finally rewarding the company for fixing its flows (positive NNB) and finding a new growth story (Private Assets).

Schroders enters 2026 not as a dusty City incumbent, but as a diversified wealth and private capital manager trading at a reasonable 15x P/E with a juicy 5%+ yield. For investors, the stock has moved from the "Value Trap" bucket to the "Quality Recovery" bucket.

Please wait processing your request...

Please wait processing your request...