If you’ve been watching the FTSE 250 today, you might have noticed a quiet giant waking up. Serco Group (LSE: SRP), the company that runs everything from naval design to justice services, just popped ~7%.

For a mature support services company, a move like this isn't just noise—it's a signal. The market is pricing in a fundamental shift. Below is the analytical deep dive into why Serco is rallying, what’s changed in their business model, and the critical factors driving this momentum.

The Catalyst: Why the Sudden 7% Jump?

The rise today was driven by a powerful pre-close trading update that acted as a "beat and raise" for the market.

1. Profit Guidance Upgrade (The "Beat")

Investors love certainty, and they love it even more when companies outperform expectations.

- The News: Serco raised its 2025 underlying operating profit guidance to £270m, up from the previous £260m.

- Revenue Momentum: The company expects 2025 revenue to hit £4.9bn, a 3% increase at constant currency.

2. The 2026 "Goldilocks" Outlook (The "Raise")

The stock didn't just move on 2025 numbers; it moved because 2026 looks even stronger.

- 2026 Profit Target: Initial guidance for next year is ~£300m.

- Margin Expansion: Operating margins are expected to hit 6.0%, reaching the top end of their medium-term target range of 5-6%.

3. Shareholder Yield Bonanza

Serco is aggressively returning cash. They just completed a £50m share buyback, bringing the total returned to shareholders via buybacks to £390m since 2021. This reduction in share count naturally boosts Earnings Per Share (EPS), a metric highly favored by the market.

Source: Kalkine Group

Latest Business Updates: Defense is the New Offense

The "old" Serco was often viewed as a generalist outsourcer. The "new" Serco is increasingly looking like a High-Tech Defense Prime.

- Defense Sector Dominance: Order intake for the year reached a massive £5.5bn with a book-to-bill ratio of 110%. Crucially, two-thirds of these new awards were in the Defense sector, particularly across the UK and North America.

- The MT&S Integration: The $327m acquisition of the MT&S (Mission Training and Satellite Ground Network) business from Northrop Grumman is now fully integrated. This gives Serco elite capabilities in the US naval and space markets.

- Leadership Transition: Serco announced Mark Reid (formerly of Proximus) as the new Group CFO, succeeding the retiring Nigel Crossley. The market typically views a smooth transition to a candidate with international experience as a "de-risking" event.

- Strategic Disposal: They sold their Hong Kong operations in September 2025, further cleaning up the portfolio to focus on higher-margin, core government sectors.

The New Business Model: "Impact at Scale"

Serco has pivoted away from low-margin, generic facilities management. Their current strategy focuses on complex, highly regulated environments with high barriers to entry.

- Geographic Tilt: North America is now the powerhouse, set to represent approximately 50% of Group underlying operating profit following the MT&S deal.

- Technology-Led Services: By integrating software and engineering (like MT&S) with frontline delivery, they are moving away from being a "body shop" toward being a "solutions provider."

- Structural Demand: Governments are facing increasingly complex challenges—from naval modernization to migration logistics—driving long-term demand that is largely decoupled from the broader economic cycle.

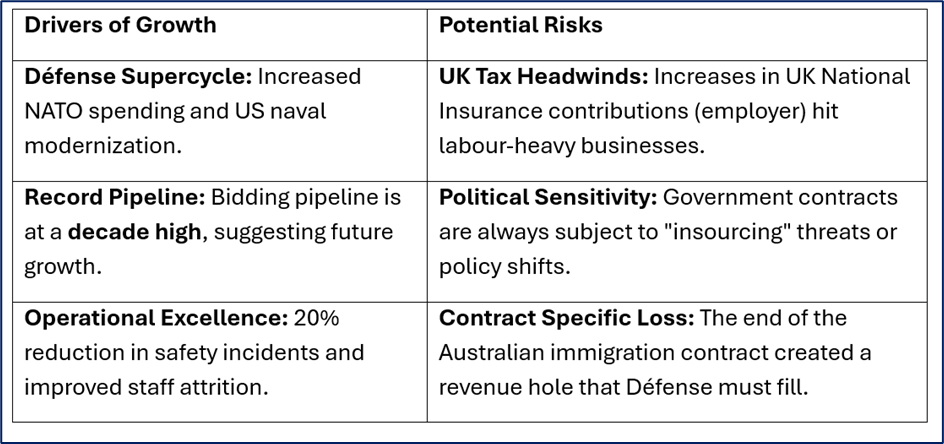

Key Drivers & Risks to Watch

While the momentum is strong, the "Serco Story" has specific headwinds that analysts are monitoring closely.

Source: Kalkine Group

Conclusion: A Re-Rating in Progress?

Serco’s move today suggests that the market is finally beginning to view it not as a legacy outsourcer, but as a specialized defense and justice powerhouse. With profit targets moving toward the £300m mark for 2026 and margins hitting their ceiling, the company is demonstrating "operating leverage"—where profits grow faster than revenue.

As it sheds non-core assets like the Hong Kong business and integrates high-margin US defense tech, the question for the FTSE 250 is no longer if Serco can grow, but how high its new "defense-led" valuation can go.

Source: Trading View, 17 December 2025, 12:55 PM GMT

Please wait processing your request...

Please wait processing your request...