Severfield PLC (LSE: SFR), the UK’s structural steel powerhouse, closed the 2025 trading year on a high note, with its share price jumping ~3.2% on December 31, 2025, to finish at GBX 28.90.

After a turbulent year defined by a high-profile "bridge crisis" and a significant profit warning in March, the year-end rally signals a shift in retail sentiment toward a "trough-is-in" recovery narrative for 2026.

The 31st December Rally: Key Drivers

While the broader FTSE All-Share remained relatively flat, Severfield’s outperformance was driven by a confluence of technical and fundamental factors:

Source: Kalkine Group

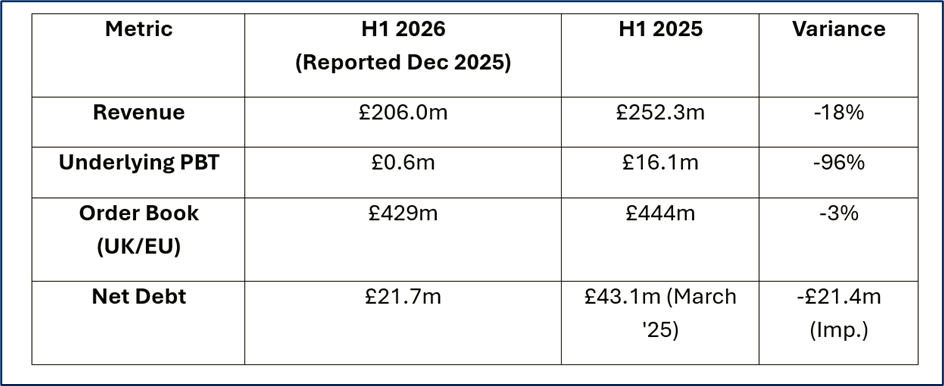

- Beating the "Break-Even" Bar: Investors are still reacting to the December 2nd Interim Results, where Severfield reported an underlying profit of £0.6m. While this was a 96% drop year-over-year, it crucially beat analyst expectations of a "small loss," proving the company’s resilience in a brutal pricing environment.

- India’s Explosive Momentum: The JSW Severfield Structures (JSSL) joint venture in India is the group’s "hidden gem." With a record order book of £286m (up 45% YoY) and a new facility in Gujarat coming online in early 2026, the market is beginning to value the India business as a high-growth engine distinct from the sluggish UK market.

- De-risking the "Bridge Crisis": The completion of the insurance settlement—securing £20.0m in proceeds for bridge remedial works—has removed a massive overhang of uncertainty that plagued the stock since late 2024.

- Short Covering & Window Dressing: As a classic "value play" with a P/E ratio now sitting around 6.5x, institutional fund managers likely adjusted positions on the final day of the year to include "beaten-down" recovery stories for their 2026 portfolios.

The 2026 Business Model: From Steel Fabricator to Solutions Partner

Severfield has evolved its model to combat the "commodity" trap of simple steel fabrication.

- Core Construction: Dominating the UK market with a 150,000-tonne annual capacity, focusing on complex "anchor" projects like data centers, nuclear (Sellafield), and stadia (Everton Stadium).

- Modular & Product Innovation: The Severstor division provides modular housing units for power and data sectors, offering higher margins than traditional structural steel.

- Global Diversification: Shifting capital toward India (JSSL), where steel demand is skyrocketing due to infrastructure expansion and a shift away from concrete.

- Operational Gearing: By cutting costs and reducing capex in 2025, the company is now lean. Even a small 5% recovery in market demand in 2026 could lead to a massive "bounce-back" in profits due to high operational gearing.

Latest Financial & Operational Snapshot

Source: Company Data

- Operational Wins: Secured £190m of new work in H1 2026.

- Cash Position: Net debt nearly halved in six months, providing a £50m+ headroom in their revolving credit facility.

- Leadership: New CEO Paul McNerney is set to unveil a refreshed "Strategic Roadmap" in early 2026, which the market is eagerly anticipating.

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Market Leadership: UK’s largest structural steel player with unparalleled technical expertise in "mega-projects."

- Diversified Sectors: Exposure to high-growth areas like Data Centres and Offshore Wind (Hornsea 3).

- Fortress Balance Sheet: Significant debt reduction and successfully extended banking facilities to 2027.

Weaknesses

- Low Margins: Current operating margins are thin due to "commodity" project substitution during the 2025 lull.

- Bridge Legacy: While insurance is settled, the remedial work program still requires management bandwidth through 2026.

Opportunities

- India Upside: Potential to sell a 24.9% stake in the Indian JV for up to £20m, providing a massive cash injection.

- Green Steel Transition: Lead the market in low-carbon steel fabrication as ESG requirements for tier-1 contractors tighten.

- Strategic Pivot: The new CEO may shift focus toward higher-margin maintenance and modular services.

Threats

- Delayed Tendering: Client decision-making in the UK remains slow due to high interest rates and subdued economic confidence.

- Raw Material Volatility: Any sudden spike in global steel or energy prices could squeeze the fixed-price contracts currently in the order book.

Critical Risks to Watch

- The "L-Shaped" Recovery: If the anticipated 2026/27 market recovery in the UK commercial sector stalls, the "bounce-back" narrative could fail.

- Project Concentration: The absence of multiple "mega-anchor" projects means the company is more reliant on a higher volume of smaller, more competitive bids.

- Execution Risk: Any further technical issues similar to the 2024 bridge welding problems would be catastrophic for the stock's hard-won "recovery" reputation.

Conclusion

Severfield’s 3.2% gain on New Year's Eve is more than just a daily fluctuation; it is a signal that the market has likely priced in the "worst-case scenario" of 2025. With a record order book in India, a stabilized balance sheet, and a valuation that looks "dirt cheap" compared to historical norms, the steel giant enters 2026 as a classic contrarian play. Investors are no longer looking at the losses of the past; they are looking at the "operational gearing" potential of the future.

Please wait processing your request...

Please wait processing your request...