Fresnillo, the world’s largest primary silver producer, just gave retail investors a late Christmas present. On December 29, 2025, the stock climbed approximately 2-3%, hitting a new 12-month high and trading comfortably above GBX 3,300 and then fizzle out down by 2.63% and closed at GBX 3,116, due to ferocious sell off in silver from higher levels ($74/oz).

While the FTSE 100 has been steady, Fresnillo is acting like a growth stock in a miner’s uniform. But why the sudden jump today? Is this just another volatility spike, or is the market pricing in a fundamental shift for 2026?

Here is the analytical breakdown of the move, the drivers, and the risks—no spreadsheets, just straight talk.

- The Catalyst: Why the Stock Popped

The immediate trigger for the ~2% rise wasn't a company press release; it was the commodity market screaming "scarcity."

Source: Kalkine Group

- Silver Hits All-Time Highs: Spot silver prices touched an intraday record above $80 per ounce on Dec 29. Fresnillo is a "leveraged play" on silver; when the metal moves, the miner moves harder.

- The China Factor: Markets are reacting nervously to new restrictions on Chinese silver exports set to take effect on January 1, 2026. Traders are front-running the potential supply shock, bidding up silver prices and, by extension, Fresnillo shares.

- The "Fear & Rates" Trade: With US interest rate cuts widely expected in 2026, the dollar is softening. A weaker dollar makes commodities cheaper for foreign buyers, fueling demand. Combined with geopolitical jitters, silver is winning on two fronts: as an industrial necessity and a monetary hedge.

- Key Drivers: The Engine Room

Beyond the daily price action, three structural engines are driving Fresnillo’s valuation upward:

- The Green Energy Supercycle: Silver is the "glue" of the green economy. Solar panels, EVs, and data centers for AI all require massive amounts of silver. We are seeing a transition from "cyclical demand" to "structural deficits."

- Operational Margins: Fresnillo’s All-In Sustaining Cost (AISC) is hovering around $17–$20 per ounce. With silver trading at $80+, their margins are essentially printing cash. This operational leverage means a 10% rise in silver prices can lead to a disproportionately larger jump in free cash flow.

- Analyst Upgrades: Institutional confidence is returning. Major banks like Citi and Canaccord recently hiked their price targets, validating the bull case. The market listens when the big money changes its tune from "Hold" to "Buy."

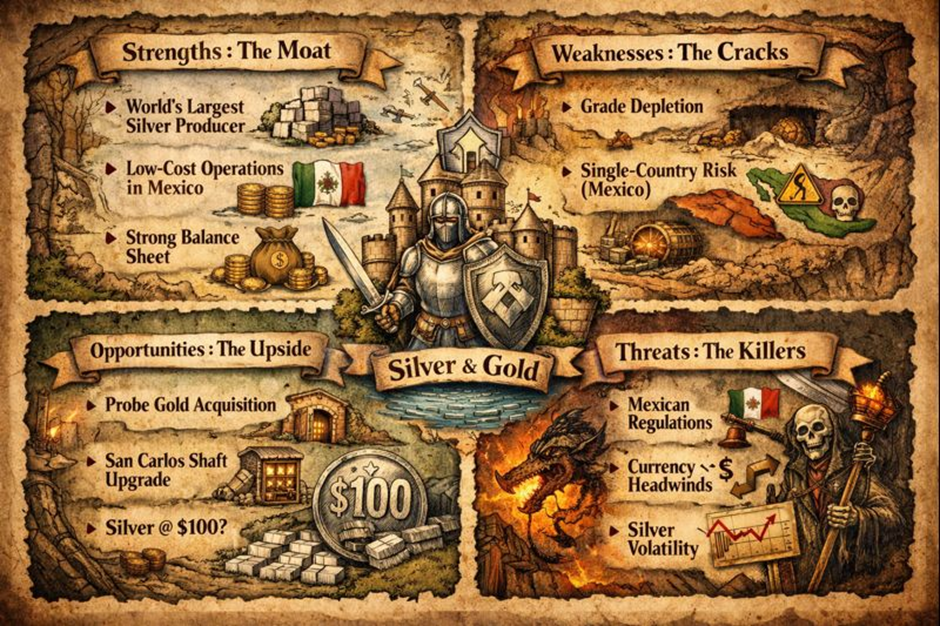

- SWOT Analysis

Here is the strategic landscape for Fresnillo as we head into 2026.

Source: Kalkine Group

Strengths (The Moat)

- Scale: Still the world's largest primary silver producer. Size matters in mining.

- Cost Advantage: Low-cost operations (mostly in Mexico) allow them to remain profitable even if silver prices crash by 50%.

- Balance Sheet: Strong cash position with manageable debt ratios, allowing them to pay healthy dividends (including the recent special dividend).

Weaknesses (The Cracks)

- Grade Depletion: The "easy" silver is gone. Q3 2025 reports showed silver production down due to lower ore grades at key mines like Saucito. They have to process more rock to get the same amount of metal.

- Single-Country Risk: Almost all operations are in Mexico. They are not geographically diversified, exposing them entirely to Mexican political and security risks.

Opportunities (The Upside)

- Probe Gold Acquisition: The recent move to acquire Probe Gold signals a hunger for growth and diversification beyond their legacy assets.

- Efficiency Projects: The commissioning of the San Carlos shaft is a game-changer, expected to significantly lower haulage costs starting in 2026.

- Silver @ $100: If the "industrial squeeze" continues, triple-digit silver is no longer a fantasy. Fresnillo would be the prime beneficiary.

Threats (The Killers)

- Mexican Regulatory Climate: Changes in mining laws or bans on open-pit mining in Mexico remain a looming shadow.

- Currency Headwinds: A strengthening Mexican Peso increases their local labor and energy costs (which are paid in Pesos), eating into USD-denominated profits.

- Volatility: Silver is known as "the devil's metal" for a reason. It crashes as fast as it soars.

- The Business Model: 2026 Evolution

Fresnillo isn't just digging holes anymore; they are optimizing them.

- Old Model: Maximize volume at all costs.

- New Model (2025-2026): Value over Volume. The company has shifted focus to operational excellence. They are accepting slightly lower production volumes (due to grade decline) but are aggressively cutting costs through technology (like the San Carlos shaft) and grid efficiencies.

- The "Smart Miner" Pivot: They are increasingly integrating renewable energy into their mining operations to lower power costs and meet ESG mandates, which attracts premium institutional investors.

- Financial & Operational Reality Check

Let’s look at the numbers from the latest Q3 and H1 updates:

- Q3 Production: A mixed bag. Silver output dropped ~6.6% quarter-on-quarter, but Gold production is trending toward the upper end of guidance. The market forgave the silver drop because the price of silver made up the difference.

- Revenue & Profit: H1 2025 saw revenues up 27% and profits nearly doubling. The "price effect" is currently masking the "production volume" struggle.

- Dividends: The company returned over $500m to shareholders in 2025. For retail investors, this yield is a massive cushion against volatility.

- The Risks: What Could Go Wrong?

Don't let the green arrows fool you; risks are real.

- The "Paper Silver" Crash: If the global economy enters a hard recession, industrial demand for silver (electronics, solar) could plummet.

- Security in Mexico: The security situation in certain Mexican states is volatile. Any disruption to supply chains or personnel safety could halt operations overnight.

- Inflation: While they sell inflation hedges (gold/silver), they also suffer from inflation costs (diesel, steel, labor). If costs rise faster than metal prices, margins shrink.

Conclusion: The Runaway Train?

Fresnillo’s 2% rise today is a symptom of a larger fever: the world is realizing it might not have enough silver.

The company is in a "Sweet Spot." They have operational challenges (grades are falling), but the commodity price boom is so powerful it doesn't matter right now. They are generating cash, paying dividends, and sitting on the most valuable inventory in the mining sector.

The Verdict: If you believe in the Green Energy transition and $100 silver, Fresnillo is the vehicle. If you worry about Mexican politics or a global recession, it’s a high-beta risk.

Please wait processing your request...

Please wait processing your request...