Image source: Shutterstock

Highlights

- Smith & Nephew’s FY24 revenue grew by 4.7% YoY, reaching USD 5,810 million, driven by strategic initiatives and improved product availability

- Smith & Nephew's 12-Point Plan helped mitigate challenges in US Orthopaedics and China's VBP programmes, contributing to growth

- The company phased out one-third of its global hip and knee brands, further enhancing revenue performance

- Smith & Nephew forecasts around 5% revenue growth in 2025, despite a USD 25 million headwind from China's VBP extension

Smith & Nephew PLC (LSE:SN.) is a medical technology company with a diverse portfolio. It specialises in the development, production, marketing, and sale of medical devices and related services.

Smith & Nephew's revenue for the financial year 2024 (FY24) increased by 4.7% year-over-year, reaching USD 5,810 million, compared to USD 5,549 million in FY23. This growth was driven by the company's 12-Point Plan, which helped improve performance despite challenges in the US Orthopaedics market and China’s VBP programmes. Key initiatives, such as improved product availability, portfolio simplification, and a significant reduction in overdue orders, were instrumental in driving the revenue boost. Additionally, one-third of global hip and knee brands were phased out, contributing to the overall growth.

The company's trading profit for FY24 rose by 8.1% YoY, reaching USD 1,049 million, up from USD 970 million in FY23. This increase was primarily driven by productivity savings of 410bps and operating leverage of 390bps, which helped offset significant challenges. These headwinds included input cost inflation, merit adjustments, and foreign exchange impacts, along with a negative impact from the Chinese market.

Company Outlook

Smith & Nephew aims for revenue growth of around 5% in 2025, despite a USD 25 million headwind from China's VBP extension. First-quarter growth is expected to be between 1% and 2%, with improvements expected later in the year. The company anticipates a trading profit margin of 19% to 20%, driven by cost reductions and network optimisation. Margin strength is expected to increase in the second half as the impact from China eases. Additionally, Smith & Nephew forecasts trading cash conversion of 80% to 90%, restructuring costs of USD 45 million, and a tax rate of 19% to 20%.

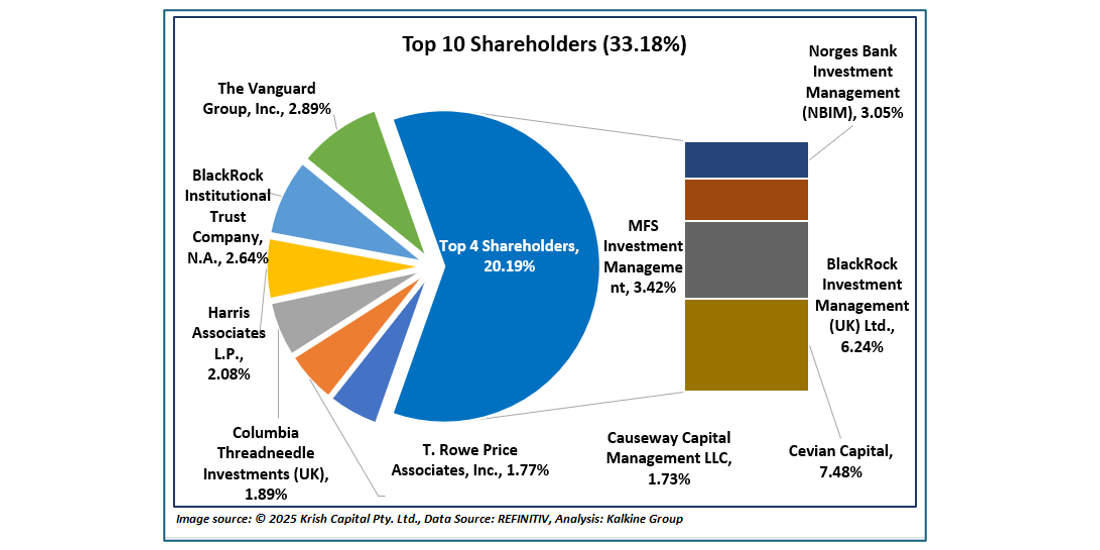

Top 10 Shareholders

The top 10 shareholders of Smith & Nephew collectively account for approximately 33.18% of the total shareholdings in the company. Cevian Capital holds the largest stake with around 7.48%, followed by BlackRock Investment Management (UK) Ltd., which holds approximately 6.24%, as shown in the chart below:

Stock Information

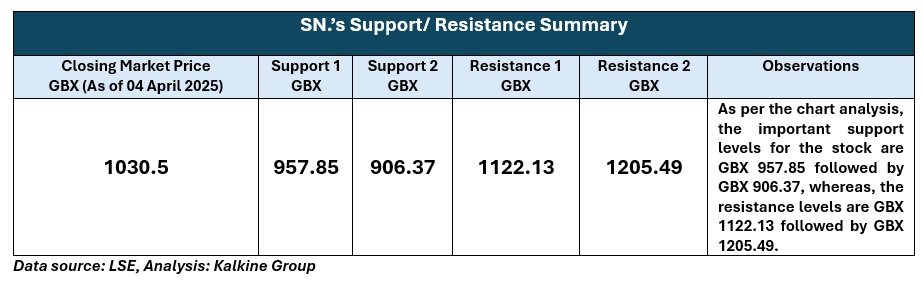

The stock has dropped by approximately 10.66% in the past month and has decreased by about 6.40% over the last six months. Its 52-week low and high are GBX 911.00 and GBX 1,245.26, respectively. Currently, the stock is trading below the average of its 52-week high and low, with a closing price of GBX 1,030.5 as of 04 April 2025.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference data for all price data, currency, technical indicators, support, and resistance levels is 04 April 2025. The reference data in this report has been partly sourced from EODHD/Others.

Technical Indicators Defined

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Please wait processing your request...

Please wait processing your request...