The London Stock Exchange opened its 2026 doors with a green spark as SSE PLC (LSE: SSE) climbed ~2.3% on January 2nd, closing at approximately 2,231p.

While the broader FTSE 100 showed modest gains, SSE outperformed its peers, driven by a combination of regulatory clarity, strategic "green" financing, and a clear roadmap for the UK’s energy transition.

Key Drivers: Why SSE Lit Up the Market

Source: Kalkine Group

The rally on the first trading day of 2026 wasn't a fluke; it was the culmination of several year-end milestones:

- The £1 Billion "Green" Boost: In late December 2025, SSE’s transmission arm (SSEN Transmission) secured a £1bn green loan backed by the UK government's National Wealth Fund. This facility ensures the "Orkney Link" and other critical North Sea grid projects are fully funded.

- Regulatory De-risking: Ofgem’s recent approval of a £28bn package for energy transmission networks has provided investors with the "gold standard" of utility certainty: guaranteed returns on massive infrastructure spend.

- Dividend Deadline: January 2, 2026, served as the final date for shareholders to elect for the Scrip Dividend Scheme. This mechanism allows investors to receive new shares instead of cash, a move that often stabilizes the stock price by signaling long-term investor commitment.

- Market Rotation: As 2026 begins, institutional capital is rotating back into "Defensive Growth" stocks. SSE’s unique mix of regulated "bond-like" income from grids and high-growth potential from offshore wind makes it a prime target for balanced portfolios.

The 2026 Business Model: "The Integrated Energy Powerhouse"

SSE has shifted its business model away from retail energy (selling to homes) to focus entirely on Low-Carbon Infrastructure.

- SSEN Transmission & Distribution: The "backbone." This segment earns regulated returns by building and maintaining the wires that carry electricity. By 2026, this is the company's largest profit driver.

- SSE Renewables: The "growth engine." SSE is a leader in offshore wind, including the massive Dogger Bank project. Its model focuses on developing, owning, and operating assets, then "rotating" (selling) minority stakes to fund future projects.

- SSE Thermal (Flexibility): The "stabilizer." Using gas-fired plants with carbon capture (CCS) and battery storage to provide power when the wind doesn't blow.

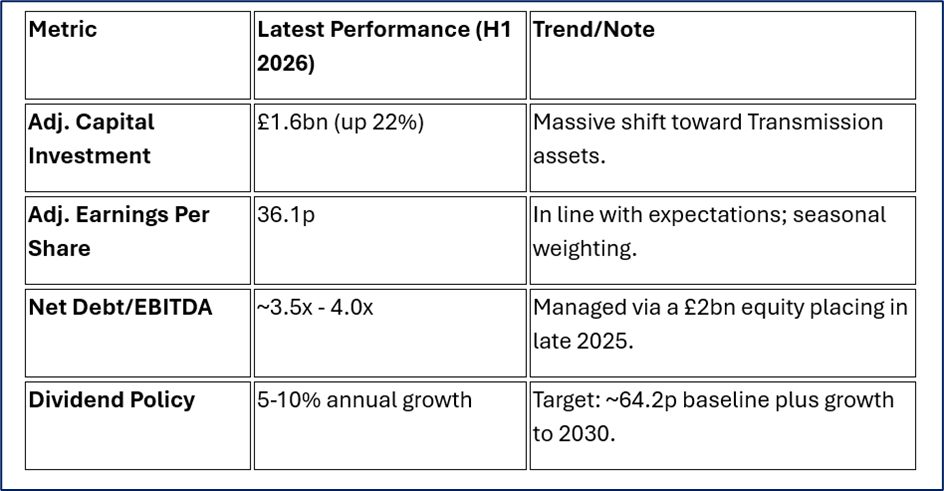

Financial & Operational Update: By the Numbers

According to the latest interim data (H1 2025/26), SSE is mid-way through a £33bn five-year investment plan:

Source: Company Data

Operational Milestone: The Viking Wind Farm (Shetland) is now fully operational, and turbine installation at Dogger Bank Phase A is nearing completion, significantly boosting renewable output for the 2026 fiscal year.

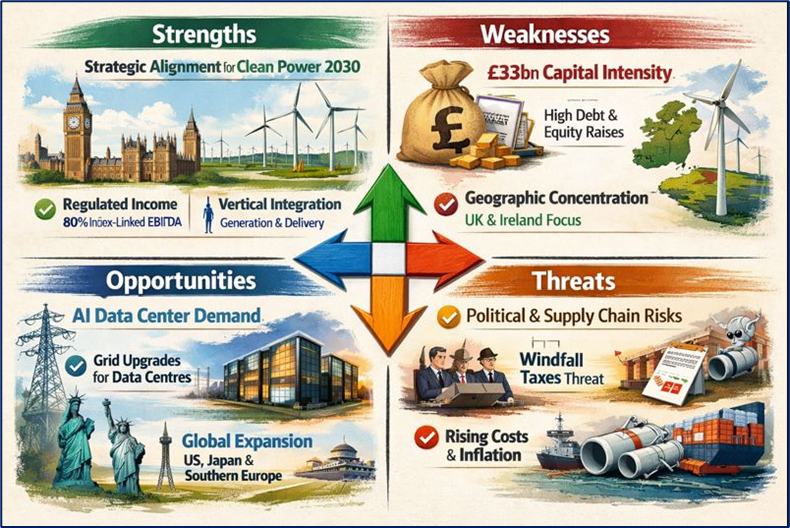

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Strategic Alignment: Perfectly positioned for the UK Government’s "Clean Power 2030" goal.

- Regulated Income: ~80% of future EBITDA is expected to be index-linked or regulated, providing a hedge against inflation.

- Vertical Integration: Owns the generation (wind) and the delivery (wires).

Weaknesses

- Capital Intensity: The £33bn plan requires constant debt management and occasional equity raises (dilution).

- Geographic Concentration: Over-reliance on the UK and Irish regulatory environments.

Opportunities

- AI Data Center Demand: The surge in UK data centers requires massive grid upgrades, directly benefiting SSEN Transmission.

- International Expansion: Early-stage entries into the US, Japan, and Southern Europe renewable markets.

Threats

- Political Risk: Potential for "windfall taxes" if energy prices spike again.

- Supply Chain Inflation: Rising costs for turbine components or specialized installation vessels could squeeze margins.

Key Risks to Watch

While the January 2nd jump is positive, three risks remain central for 2026:

- The "CEO Transition": With Alistair Phillips-Davies set to retire, the market will be hyper-sensitive to the new CEO's ability to execute the £33bn plan without "execution slippage."

- Weather Dependency: Low wind speeds in Q3/Q4 can lead to earnings volatility, despite the stability of the grid business.

- Interest Rates: As a capital-intensive utility, higher-for-longer interest rates increase the cost of servicing the ~£11.4bn debt pile.

Conclusion

SSE's 2.3% climb on the first day of 2026 reflects a market that finally values "boring" infrastructure when it’s paired with "exciting" green growth. The company has successfully navigated its £2bn capital raise and secured the backing of the National Wealth Fund, leaving it with a fortress-like balance sheet to tackle the year ahead. As the UK accelerates its electrification, SSE isn't just a utility—it's the primary landlord of the British energy transition.

Please wait processing your request...

Please wait processing your request...