Shares of SSP Group PLC (LSE: SSPG), the operator of food and beverage outlets in travel locations like airports and railway stations, surged by approximately 15% following the release of its latest full-year results and a forward-looking strategic review. This major movement signals renewed investor confidence in the travel food giant’s ability to unlock significant value and accelerate future growth.

Key Reasons & Drivers for the Stock Surge

The significant stock jump was driven by two major announcements within the annual results, which signals management's decisive action to unlock future value and improve overall profitability:

- Wide-Ranging Review of Continental European Rail Business: SSP announced a "wide-ranging review" of its struggling Continental European rail division, which has been an underperformer since the pandemic. This decisive action signals a strong intent to address and potentially divest or significantly restructure a key area of weakness, removing a major drag on group earnings. This move is seen as critical for margin recovery.

- Exploring Options to Realize Value in Indian Investee (TFS): The company is actively mulling options to "realise value" in its recently listed Indian investee, Travel Food Services Ltd (TFS). Given the burgeoning growth potential in the Indian aviation market, this move, potentially through a partial sale or IPO proceeds, is expected to unlock substantial shareholder value quickly.

Source: Kalkine Group

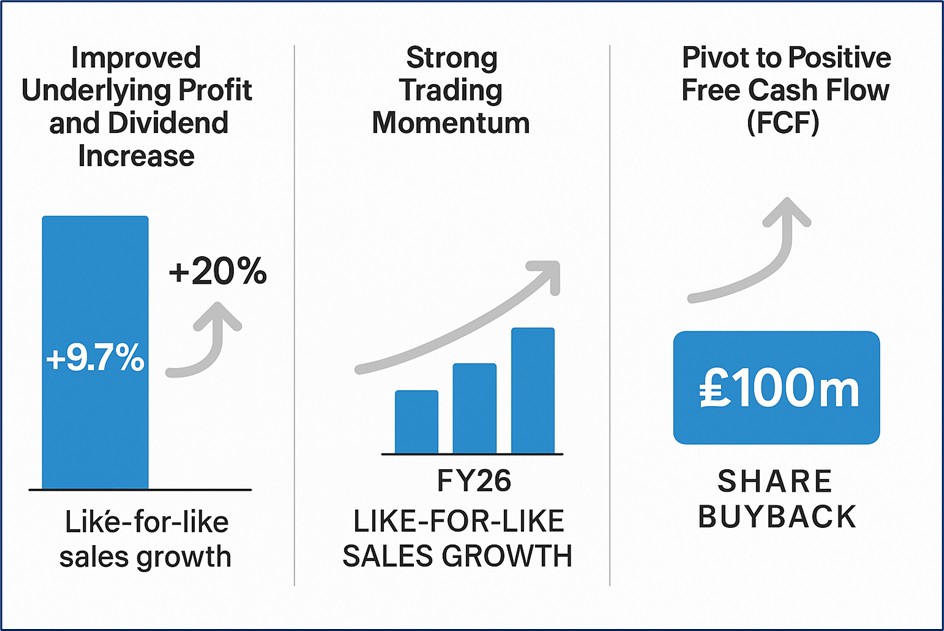

The positive investor sentiment was further supported by a resilient financial performance in other key regions and strong operational momentum:

- Improved Underlying Profit and Dividend Increase: Underlying pretax profit grew by 9.7%, and the total dividend was raised by a robust 20%, demonstrating management’s confidence in the company's financial health, cash generation, and commitment to capital return.

- Strong Trading Momentum: The company reported an encouraging start to the new financial year (FY26) with like-for-like sales growth positive across all regions, underpinning the optimistic outlook.

- Pivot to Positive Free Cash Flow (FCF): A crucial shift to positive FCF, enabling the initiation of a new £100 million share buyback program, marked a significant financial turning point.

Source: Company Data, Kalkine Group

SSP Group's Business Model: The Travel Concessionaire

SSP Group operates as a food and beverage concessionaire in high-traffic travel locations across 38 countries, fundamentally operating as a monopoly provider in many secured sites.

- Concession-Based Approach: The core model involves securing long-term contracts (typically 5 to 10 years) through competitive tenders to operate F&B outlets in premium airports and railway stations.

- Captive Audience: It capitalizes on the captive audience of travelers, who often have limited dining options and higher willingness to spend due to time constraints and necessity, providing structural pricing power.

- Diverse Portfolio: The company manages a diverse mix of proprietary brands (like Upper Crust, Ritazza, Soul + Grain) and popular international/national franchised brands (like Starbucks, Burger King, M&S Simply Food), allowing it to cater comprehensively to varied passenger demographics.

- Revenue Structure: Revenue is primarily derived from direct F&B sales, structured through concession agreements that involve a minimum fixed rent plus a percentage of sales, ensuring both baseline income and upside potential tied to passenger volume.

Financial and Operational Latest Data (FY25 Highlights)

Figures are for the year ended September 30, 2025 (FY25), based on the latest company reports:

- Revenue: £3.64 billion (+6.0% year-on-year), supported strongly by performance in North America and the UK.

- Underlying Pretax Profit: £172.3 million (+9.7% year-on-year), showcasing underlying operational and margin improvement.

- Reported Pretax Loss: A reported loss of -£10.4 million, which resulted primarily from high non-underlying costs, including a substantial £50.7 million impairment charge, as well as significant IT and restructuring expenses.

- Total Dividend: A sharp increase to GBX 4.2 per share (+20% year-on-year), signalling conviction in sustained cash flow.

- Free Cash Flow (FCF): The crucial pivot to Positive FCF of approximately £80 million, providing the foundation for the new share buyback program.

- Continental Europe Underperformance: Sales in this specific region were flat or slightly down (-0.2%), highlighting why this area is the focus of the current strategic review to reset the operating model and balance sheet allocation.

Conclusion and Strategy for Investors

Conclusion

SSP Group has delivered a resilient full-year performance, marked by strong underlying profit growth and a significant shift to positive free cash flow. The massive stock surge reflects investor optimism about the management's proactive, decisive steps to tackle the chronic underperformance in Continental Europe and unlock material value from the high-growth Indian market (TFS). While one-off non-underlying costs impacted reported profit, the narrative has shifted to operational momentum and strategic clarity.

Investor Strategy

- Long-Term Growth Focus: The core investment thesis is tied to the continued global recovery of passenger traffic (air and rail) and the successful execution of the new strategy. Investors should look beyond the statutory loss and concentrate on the trajectory of Underlying Operating Profit and, crucially, Free Cash Flow.

- Monitor Execution: Closely watch the updates on the Continental European review (expected by May next year) and the strategy for TFS value realization. Successful execution in these two distinct areas is the primary driver for sustained share price appreciation.

- Capital Return Signal: The initiation of a £100 million share buyback program and the raised dividend are powerful signals of management's confidence and commitment to enhancing shareholder returns, providing a strong floor for the share price.

- Risk Management: While improving, Continental Europe remains a key risk until the review is complete and tangible operational improvements are visible. Broader risks include renewed geopolitical volatility impacting global travel and inflation eroding operating margins.

Source: Trading View, 4 December 2025, 11:20 AM GMT

Please wait processing your request...

Please wait processing your request...